At this time of the year we typically get warm and generous wishes for the New Year and, of course, numerous questions about what our crystal ball has in store for 2013. While many economists publish their perspectives prior to January 1, we opted to wait in the hope of having a clear fiscal picture for the United States. A lot of good that did us…

We have pooled our thoughts with that of our colleagues from the Country Risk Group for a whirlwind economic tour around the world. First, though, here are some broad themes that bear watching across jurisdictions:

-

Fiscal Reform. It’s hard for governments to budget when times are less than perfect. And when you combine economic stress with calls for structural reform, the process becomes downright intractable. Coalitions weaken, as one side tries to place blame for austerity on the other.The balance between promoting growth and limiting national debt is delicate. Many countries are facing rising costs for medical and retirement programs, partly because of demographics. With the number of beneficiaries rising, the will to make meaningful change may be difficult to muster.

-

Generating Jobs. Unemployment remains high in the world’s major economies, frighteningly so in some nations. Better growth would certainly help to prompt more hiring, but there are structural impediments of various degrees that need to be surmounted.

-

The Limits of Central Banks. The Federal Reserve, the Bank of Japan, the ECB, and the Bank of England have all implemented unconventional policies since 2008. They have all been effective to varying degrees, but results may diminish over time. In the process, monetary authorities have been accused of overstepping their bounds and serving as enablers for wanton banks and legislatures. How long will money remain so easy?

- Balance Sheet Repair. Whether American consumers, certain banks, or governments are doing it, bringing assets and liabilities into better alignment is a work in process. As this progresses, spending and credit may continue to be muted.

Following are specific thoughts on how major markets are expected to fare.

United States – Another Year of Underperformance

The US economic summary of 2012 would highlight moderate growth, a slightly lower unemployment rate, contained inflation, and a comeback for the housing sector. What is in store for 2013?

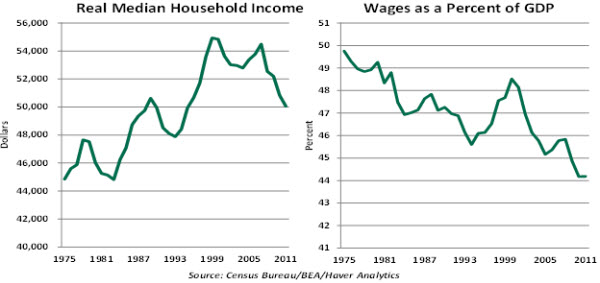

Consumer spending, the mainstay of the economy, is projected to show only a modest increase this year, reflecting the combined pressure from tepid income gains, elevated debt, and an increase in taxes. The pace of hiring in recent quarters has hovered around 150,000 per month, producing very modest wage gains. Projections of payroll employment and income for 2013 are lackluster and fundamentals of household finances are soft. Although the economic recovery is in its fourth year, real median household income is still in decline after the recent peak in 2007. Also, on a historical basis, the share of labor income in the nation’s economic pie has shrunken rapidly.

In addition to a lack of strong support from income, households are focused on cleaning up their balance sheets. The reduction of household debt has come a long way from the highs seen in 2008, but the process is still ongoing and will continue to hold back discretionary consumer spending. The expiration of the 2.0% payroll tax cut, higher income taxes for high income households, and additional taxes to fund provisions of the Affordable Care Act will each account for trimming overall consumer spending.

The housing sector should continue to improve, but the lack of credit availability and tepid gains in income are both important factors preventing a stronger recovery of home sales. The home price picture shows a significant positive trend partly due to the reduction of distressed properties in the marketplace. The gradual increase in home prices has translated into fewer home mortgages that are underwater. Both of these positive developments are expected to continue in 2013. Residential investment expenditures should record the second consecutive annual contribution to real GDP following a string of annual declines since 2006.

Although businesses are well positioned with strong balance sheets and ample liquidity, recent survey data are not optimistic about capital spending plans. Exports played a big role in lifting the growth of GDP during the onset of the recovery but this has changed in large part due to headwinds from Europe and more muted gains in GDP growth among other trading partners. The upshot is that exports could turn out to make the smallest contribution to GDP since the recovery commenced, at best.

The unresolved spending plans of the US Federal government and the debt ceiling impasse have complicated the fiscal outlook for 2013. Irrespective of how these issues are resolved, the bottom line is that a fiscal drag in 2013 is nearly certain. Our most-likely scenario does not include the sudden spending cuts now scheduled for March 1 or a shutdown of government created by the failure to increase the US debt ceiling.

State and local government outlays have declined for several years in a row. Fiscal consolidation in most states should result in small spending and employment gains in 2013. However, financial conditions of most local governments remain on shaky ground.

Overall, the US economy is predicted to move along at a nearly 2.0% pace in 2013, marking the third consecutive year of only moderate economic growth. This should result in only a small reduction in the unemployment rate (7.3% by year-end) during the next twelve months. Expectations of contained demand are consistent with a favorable outlook for inflation that is within the Fed’s short-term tolerance mark (2.5%). This combination should support central bank asset purchases throughout 2013, barring an upside surprise of a “substantial improvement” in the labor market.

Lurking in the recesses of the baseline economic story are a few risks that could throw the economy off its track. The inability of Congress to put the fiscal house in order, an unraveling of the eurozone banking and economic situation, and a conflict in the Middle East are each potential sources of economic turmoil that will require monitoring in 2013.

Europe – Focus Shifts to Political Calendar, But Macroeconomic Imbalances Remain

Euro-zone headlines are no longer as focused on market stresses and sovereign liquidity woes. The ECB’s vows in Q4 2012 to support the euro “no matter what” appear to have appeased most investors, even though the primary method by which the Bank would support a stressed sovereign – namely, its new Open Market Transactions (OMT) program – has yet to be invoked by any government.

In addition, the decision of the “Troika” (IMF, EU, and ECB) to resume aid disbursements to Greece has removed near-term fears of a Greek debt default and some form of forced exit from the Euro-zone. However, none of the region’s underlying economic or structural woes have really been resolved. Although reforms are ongoing in places like Italy and Spain, the competitiveness gap between such economies and Germany remains significant. And other countries, like France, seem to be in denial about their competitiveness gaps.

Unemployment continues to rise across most of Europe, particularly in those countries undergoing the deepest economic upheaval. While there are tentative signs that the Euro-zone economy as a whole may have bottomed out in Q4 2012, there are still significant headwinds – the social and economic impacts of fiscal austerity programs, very tight credit conditions as banks continue to repair their balance sheets, and the high and rising unemployment rate. Spain in particular still faces serious problems, not least its 25% jobless rate. All of this suggests that real GDP in the Euro-zone will contract by perhaps 0.5% this year, with risks still to the downside.

Meanwhile, the European headlines will focus on things political in the coming months. Italy’s general election in late February could be a game changer for that country if it ushers in a center-left coalition with a pro-reform mandate. Germany’s general election, slated for September/October, is also crucial given the country’s pivotal role as both the largest and healthiest economy in the Euro-zone, and its primary paymaster. Chancellor Merkel is still very popular, but her center-right party is unlikely to win a majority of the seats in parliament, and its traditional coalition partner looks set to be trounced in the polls. Thus, the make-up of the German government could change in Q4, with pundits looking for either a Grand Coalition of the center-left and center-right, or a new union of the center-right and Greens. Any extended uncertainty over the parameters of the new coalition would rattle the markets and undermine the euro.

There are perennial concerns about Greek political stability as the country’s economic depression exacerbates social strains and reduces the credibility of the coalition government. At the time of this writing the government’s majority has fallen to 163 of the 300 parliamentary seats, down from 179 at the time of the June 2012 election, and likely to fall further as the crisis grinds on. New political and/or economic problems in any of these Euro-zone countries could trigger a new round of market stress and a revisit of sovereign debt woes in 2013.

Political news also dominates in the UK, where supporters of the two coalition parties are increasingly disgruntled about the government’s fiscal austerity and reform policies. The coalition is likely to remain intact until the election scheduled in 2015 but Conservative PM Cameron and his Liberal Democrat Deputy Clegg will walk an increasingly fraught tightrope – mollifying the markets that fiscal reform will continue while carving out their own respective priorities ahead of the next election.

The UK marked the 40-year anniversary of its membership in the then-European Economic Community by revisiting the question of its relationship with the EU. PM Cameron faces increasing pressure from the small but vocal Euro-skeptic wing of his own party along with increasingly-vocal supporters of the UK Independence Party. While it is highly unlikely that the government will actually attempt to “renegotiate” the terms of the UK’s membership, the issue will continue to get play in the headlines. This is a distraction for a government entering the final stretch of its term in office, and if it continues to percolate could have a negative impact on market sentiment.

Like its Euro-zone neighbors, the British economy is constrained by the effects of ongoing fiscal austerity and reform, and still-tight credit conditions. Unlike many of those neighbors, the UK’s exports are relatively competitive thanks to reforms in earlier decades, and its markets are relatively diversified. Real GDP will likely be flat for 2013 as a whole, recovering more firmly in the latter half of the year and resuming trend rates of growth by 2015.

China – New Leadership Emphasizes Social Stability, But Financial Sector Woes Will be a Challenge

Sorting through the economic indicators to determine China’s future – always an interesting exercise – is particularly nettlesome this year. First and foremost, expectations for the incoming President, Xi Jinping, and his Premier, Li Keqiang are not promising. The recently nominated head of state does not carry the reformist credentials some had hoped for, yet it is becoming apparent that China can only carry on for so long under the export-economy model. Even with its glut of available labor, high and rising wages are eroding labor competitiveness, causing jobs to drift toward southern Asia.

China’s high-end export production can still carry the economy in the near-term, but this is not as labor intensive as many other manufacturing sectors, so its job-creation potential will not satisfy the expanding population. Furthermore, the weaknesses of an export-reliant economy have been apparent over the last four years, as a synchronized slowdown in China’s trading partners has forced the country to generate its own growth – often less efficiently than by foreign investment. The expectations placed on Xi and Li are for carrying the country forward while maintaining social stability and national security, which should not be a major problem. Moving the country toward a more consumption-driven economy, however, will likely not make significant advances and could work against China’s progress.

The other concern is the ambiguity surrounding the financial sector. The Big Four banks have solid financials and low non-performing loan ratios, but information gaps raise questions (i.e. special-mention loans to stressed companies, refinancing loans). The shadow banking system is also becoming an issue with credit generation, as these non-financial sector lenders are not as well regulated and their exposures not as easily determined, even though they may carry significant lending on their books.

State-directed development over the past five years has been impressive but not always profitable or productive, and there are signs that the loans supporting these developments are turning sour at a rate higher than what the government expected. As 2013 progresses, we believe that headlines coming from the Chinese financial sector will raise concerns and could diminish confidence in the larger institutions. Beijing will most certainly provide support to the Big Four banks, but the size of such a bailout could be dramatic.

Middle East – Slow and Ongoing Political Change Means Continued Uncertainty Across the Region

As the Middle East recognizes the two-year anniversary of the Arab Spring and the fall of several strongmen throughout the region, the pivotal question will be whether countries and governments have changed for the better or worse. A number of dictators were either thrown out or killed, but all the monarchies retained power despite episodes of unrest. New leaderships and constitutions have been installed, but the countries are now experiencing the pains that come with the birth of a new regime.

Economic uncertainties and no guarantee of a better tomorrow make the region very unpredictable. Egypt, the most populous Arab nation, has a popularly elected leader and a publicly approved constitution, yet will be facing its greatest economic challenge since the 1973 Yom Kippur War. Other countries across the region are experiencing throes of transition, meaning 2013 will be a trying year.

The biggest unknown is Syria, where civil war has taken tens of thousands of lives and is not showing signs of an immediate conclusion. We believe this conflict will remain within the country’s borders and eventually President Assad will be unseated, but this will create a power vacuum as the victors all wrangle for power. The key word for the Middle East is uncertainty, with the risks open-ended and heavily weighted toward the downside.

Japan – Can the LDP Jump Start the Economy?

Unfortunately, in what has become fairly common, Japan is in technical recession. Yet there is some hope that a number of factors will converge to put the nation back on the road to recovery.

First, the newly-elected Liberal Democratic Party has already announced stimulus measures amounting to 2% of GDP. Second, appointments to the top three seats at the Bank of Japan offer the promise of a more aggressive monetary stance, which may include the move to a 2% inflation target. Markets have reacted to the first factors by driving the Nikkei higher, while pushing the yen lower—both of which are welcomed by Japanese business interests.

Next, the informal boycott of Japanese goods in China should ease as the dispute over the Senkaku/Daioyu islands cools. Finally, domestic growth will be supported by continued reconstruction spending in the Tohoku region (which was ravaged by the 2011 tsunami) and an expected run-up in purchasing ahead of increased consumption taxes which take effect in 2014. Prime Minister Shinzo Abe has six months until elections in the upper house of parliament to prove that his government can put the economy on a firm footing. If not the “twisted Diet” which has stifled political progress could return.

Emerging Asia – Domestic Demand Must Drive Growth

Emerging Asian economies will continue to be saddled with sub-trend growth as the global slowdown weighs on the predominately export-led countries. An expected increase in the IT and electronics cycle will provide a boost, but demand will still fall short of expectations. Domestic consumption and inward-looking industries will be forced to pick up the slack as Asian economies wait out the global slowdown and hope for solid growth in China. Protests could return to Thailand as momentum builds for an amnesty bid for former Prime Minister Thaksin Shinawatra. In South Korea, the President-elect Park Geun-Hye will be tasked with stimulating the economy and reengaging with North Korea.

Australia – Two-Track Economy Refuses to Converge

Australia is expected to continue its 20-plus year run of positive GDP growth in 2013. However, major concerns loom over the economy. Of primary importance is the question of whether the mining boom has come to an end. Expansion in 2012 was led by capital expenditures by mining interests, but projects are now being delayed or scrapped as soft demand from China hits commodity prices. There is optimism that proposed infrastructure spending and stronger growth in its largest trading partner will prop-up commodity prices; however, the Reserve Bank of Australia (RBA) acknowledges that the boom is likely winding down.

In response, the RBA has aggressively lowered rates in hopes of stimulating a lagging domestic economy. Yet, consumers will likely remain gloomy and the strong Aussie dollar will weigh on non-mining sectors of the economy. The government’s decision to abandon plans for a fiscal surplus in 2013 will boost the economy and take some pressure off of the RBA. While elections in the latter part of the year could see PM Julia Gillard and her Labor Party booted from power, what was once considered a foregone conclusion has become murky.

Sub-Saharan Africa – Onward and Upward, But Political Headwinds Loom

The majority of Sub-Saharan African countries will continue impressive growth runs. The region has benefited from its relative insulation from the crisis in the Euro-zone due to its underdeveloped financial sector and commodity driven export industry. The exception is South Africa, which suffered from the Euro-zone crisis, as well as from labor unrest and political uncertainty on the domestic front. With party elections complete, the ruling African National Congress will likely abandon populist pandering and seek to shore up business confidence. Inflation in SSA—a perennial issue—was largely contained in the second half of 2012, but another spike in food or fuel prices could trigger protests. Unlike the successful transition of power in Ghana, elections and leadership transitions in Kenya and Ethiopia trigger some anxiety as the potential for violence looms large.

Latin America – Growth, But Not Without Growing Pains in Key Markets

Across the region, the outlook for 2013 will be affected by swings in commodity prices and inflation, as well as the outlook in China and Europe. With Chávez’s health in dire straits, Venezuela will likely see a new president in the first quarter of the year. A messy transition would feed a climb in oil prices. Headlines will follow the situation to see who fills the power vacuum left by the nation’s controversial and charismatic leader.

Meanwhile, new President Enrique Peña Nieto has promised major reforms to spur growth in Mexico. Headlines will follow the extent and success of these changes, particularly regarding security and the state-owned oil company, Pemex.

After a disappointing 2012, Brazilian policymakers face the challenge of navigating a slowing economy, rising inflation and a volatile real. Attempts to jumpstart the economy will dominate the news rather than much needed structural reforms. Look for GDP growth to rebound to 3.3% with a greater downside risk.

As one reads these accounts, the linkages between regions stand out. The success of the major economies in dealing with cyclical and structural challenges will have a significant influence on global outcomes.

Let’s hope that good solutions to difficult problems arise, and become available for export to other needy countries. That kind of trade creates no deficits. We’ll look forward to keeping you apprised on all of these fronts throughout the year.

© Northern Trust