Fed Policy Update: Waiting for Clearer Criteria for Open-Ended Asset Purchases

• The FOMC’s shift from dates to economic conditions as the basis for policy rate guidance clarified the criteria for beginning rate hikes.

• The criteria for ceasing open-ended asset purchases are not clear, and may reflect not only the evolution of the labor market recovery but also concerns about financial stability and the size of the Fed’s balance sheet. We expect the Fed to try to clarify these criteria in the months ahead.

• Asset purchases will end a “considerable time” before policy rate hikes commence, and rate hikes will commence before asset sales (as per the Fed’s “Exit Strategy Principles,” reproduced in an Appendix).

Increased clarity regarding the criteria for commencing policy rate increases

From August 2011 through November 2012, the FOMC guided expectations for how long it would maintain the current 0%-0.25% target fed funds rate with reference to a future date, leaving market participants to infer the threshold economic conditions from the Committee’s Summary of Economic Projections. The Committee shifted to explicitly state-dependent rate guidance at its December 11-12, 2012 meeting: “the Committee…currently anticipates that this exceptionally low range for the federal funds rate [0%-¼%] will be appropriate at least as long as the unemployment rate remains above 6½ percent, inflation between one and two years ahead is projected to be no more than a half percentage point above the Committee’s 2 percent longer-run goal, and longer-term inflation expectations continue to be well anchored. The Committee views these thresholds as consistent with its earlier date-based guidance.”1 From this mid-2015 starting point, market participants can adjust expectations of the timing of the first rate hike based on changes in their economic outlooks.

Criteria for ceasing asset purchases are not clear

The stated justification on September 13, 2012 for initiating open-ended asset purchases (OEAP) was a concern that, “without sufficient policy accommodation, economic growth might not be strong enough to generate sustained improvement in labor market conditions.”2 The implied condition for ceasing asset purchases is a substantial improvement in the labor market outlook.3

These general formulations raised several questions: What is meant by “sustained improvement in labor market conditions”? What constitutes a “substantial” improvement in the labor market outlook? What is the baseline against which such improvement should be measured? Is the threshold an improvement in current conditions (as implied by the first formulation), or in expected future conditions (i.e., the outlook)?

Our interpretation has been that policy makers wanted to see (1) monthly payroll employment growth of at least 150,000 – consistent over time with a 12-month decline in the unemployment rate of 0.3-0.5 percentage points – for several (6-9) months; (2) concurrent real GDP growth at a pace sufficient to sustain that pace of labor demand (2¼%-2½%); and (3) evidence that the economy was gaining momentum sufficient to support a modest further pickup in the pace of job growth, to something in excess of 175,000 per month (sufficient to reduce the unemployment rate by 0.5-0.7 percentage points every 12 months). Based on these thresholds and our economic outlook, we have expected the current $85 billion/month pace of asset purchases to persist through the first half of this year, with the program phase-out to take place over the second half.

The Fed’s labor market threshold: so far, “We’ll know it when we see it.” To this point, the FOMC has been less precise in laying out the criteria for winding down the current asset purchase program. Available evidence suggests that the threshold rate of job growth may be similar to, or slightly less than what we specified above, and that concerns about financial stability and the size of the Fed’s balance sheet will also be significant considerations.

Chairman Bernanke’s elaboration of the rationale for initiating asset purchases in September exemplifies the current shortfall of clarity in regard to the labor market threshold for ending them:

Question: Can you define and describe more specifically what “improve substantially” means?

Bernanke: [W]e’re looking for ongoing, sustained improvement in the labor market. There’s not a specific number we have in mind, but what we’ve seen the last six months isn’t it. We’re looking for something…that involves unemployment coming down in a sustained way, not necessarily a rapid way, because I don’t know if our tools are that strong, but we’d like to see an economy which is strong enough that it will support improving labor market conditions and unemployment that’s declining gradually over time”4 (italics added for emphasis).

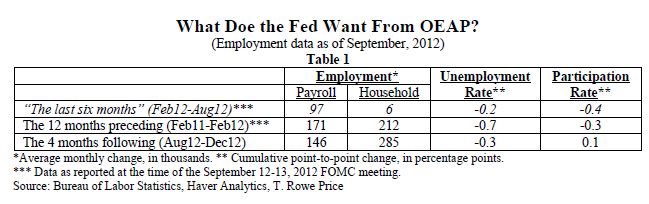

The labor market data over the six months through last August, viewed in isolation, were a legitimate basis for concern about the economy’s ability to generate a sustained decline in the unemployment rate (Table 1). Employment in the household survey barely grew, and monthly gains in the less volatile payroll survey were slightly below the 100,000-105,000 threshold required to keep the unemployment rate from rising, and well below the pace that would generate a gradual decline in the unemployment rate over time.

But how much of an improvement is the Fed expecting? Labor market data reported since the inception of OEAP have been a clear improvement on that six-month soft patch, broadly resembling the 12-month period that preceded it. Over the last four months, payroll employment growth has averaged nearly 150,000 per month (the household survey has been much stronger) and the unemployment rate has declined by 0.3 percentage points even as the labor force participation rate ticked higher. Recognizing the limited power of the Fed’s tools, might a steady trend of monthly payroll employment growth near the current pace (even absent signs of acceleration), sustained into the spring, be sufficient to justify an end to current asset purchase programs?5

Weighing modest expected benefits against mounting potential costs. The December 11-12, 2012 FOMC minutes indicate that most of the Committee’s 12 voting members thought that it would be appropriate to end asset purchases at the end of 2013, but with the largest contingent (“several”) citing “concerns about financial stability or the size of the balance sheet,” while only “a few” based their view on the “outlook for the labor market and the broader economy.”6 Assumptions of appropriate monetary policy among the 19 meeting participants sorted into similar blocs.7

Among the possible costs and risks of additional asset purchases:

• They could complicate efforts to eventually withdraw monetary policy accommodation, for example, by causing inflation expectations to rise or by impairing the future implementation of monetary policy. On the latter point, we have previously observed that the larger the Fed’s balance sheet becomes, the greater will be the quantity of excess reserves that the Fed has to drain from the banking system – by issuing term deposits (TD) and reverse repurchase agreements (RRP) – in order to control the effective fed funds rate adequately as rate hikes commence. And the greater the quantity of these alternative liabilities, the higher are likely to be the rates that the Fed has to pay to place them.

• Further enlargement of the balance sheet could complicate the process of reducing accommodation (via policy rate increases). Suppose that policy accommodation has to be removed more quickly than currently anticipated, requiring rapid asset sales. “The bigger our balance sheet, the more difficult it will be to exit in a way that meets our inflation objective without creating instability in the real economy,”8 through the sale of assets.

• Depending on the path for the balance sheet and interest rates, the Federal Reserve’s net income and its remittances to the Treasury could be significantly affected during the period of policy normalization, and could create institutional pressures to slow the pace of policy tightening or, conversely, to accelerate the course of rate hikes as a substitute for delayed asset sales.9

• Large-scale asset purchases could have adverse effects on market functioning and financial stability.

Looking ahead, we hope to see the FOMC take steps to clarify the criteria for winding down or ending its open-ended asset purchase programs. The most highly anticipated steps may pertain to characterizing the labor market conditions that would satisfy policy makers that asset purchases are no longer warranted. Less appreciated but equally important, however, will be further definition of the way that potential risks and costs are factored into decisions about the course of asset purchases. If the economy and labor market remain weaker than the FOMC would like, the Committee will have a difficult choice to make: conclude that its asset purchases to that point have been insufficient, and opt to continue or perhaps increase the pace of purchases; or conclude that its asset purchases to that point have been ineffective, and opt to discontinue a program whose costs are clearly outweighing its benefits. We would favor the latter conclusion, and think that, around mid-year, the FOMC will as well, bringing open-ended asset purchases to a conclusion whether or not the desired result has been achieved.

Exit strategy principles

Bernanke gave a strong indication at his September 13 press conference of the likely timing of completing asset purchases relative to beginning to raise interest rates: “[w]e’re not going to be able to sustain purchases until we’re all the way back to full employment; that’s not the objective.”10 The substantial interval between the end of asset purchases and the onset of rate hikes was formalized in the December 12, 2012 policy statement: “the Committee expects that a highly accommodative stance of monetary policy will remain appropriate for a considerable time after the asset purchase program ends and the economic recovery strengthens.”11 This expectation reflects the discrete purpose of the asset purchase program: “to increase the near-term momentum of the economy”12 toward the 6.5% unemployment rate threshold for raising rates, not to see the unemployment rate to that level. It is also fully consistent with the Exit Strategy Principles enunciated in the minutes of the June 21-22, 2011 FOMC meeting.13

1 “FOMC Policy Statement,” December 12, 2012. The Committee left itself flexibility to consider other factors in determining the timing of the first rate hike: “In determining how long to maintain a highly accommodative stance of monetary policy, the Committee will also consider other information, including additional measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial developments.”

2 “FOMC Policy Statement,” September 13, 2012 (as well as the statements released on October 24, 2012 and December 12, 2012).

3 We infer this second criterion from the statement that, “[I]f the outlook for the labor market does not improve substantially, the Committee will continue its purchases of…securities, undertake additional asset purchases, and employ its other policy tools as appropriate until such improvement is achieved in a context of price stability.” (“FOMC Policy Statement,” September 13, 2012, as well as the statements released on October 24, 2012 and December 12, 2012.

4 Ben S., Bernanke, “Press Conference,” September 13, 2012. Transcript provided by Roll Call Inc., via Bloomberg.

5 Put differently, might the OEAP have been initiated as a contingency against the possibility that the March-August labor market soft patch might continue (due in part to uncertainty regarding the resolution of the year-end “fiscal cliff”), as well as against the possibility of an adverse cliff outcome? In this case – might a relatively constructive resolution of remaining cliff-related issues – say, a smoothing of sequester-replacing spending cuts into later periods, and a two-year increase in the debt limit – eliminate the need for this monetary policy insurance?

6 “FOMC Policy Statement,” December 12, 2012.

7 Appendix I at the end of this document excerpts in full the passages from the December 11-12, 2012 FOMC minutes and Summary of Economic Projections relating to participants’ views on the appropriate course of asset purchases.

8 Charles I. Plosser, President and Chief Executive Officer, Federal Reserve Bank of Philadelphia, “Good Intentions in the Short Term with Risky Consequences for the Long Term,” November 15, 2012.

9 “[t]he Fed’s balance sheet is not only quite large, but it now contains mostly long-term securities. As interest rates rise, if the Fed finds it must sell assets at a rapid pace to restrain inflation, it would very likely incur substantial losses. If so, the Fed may not be able to make any remittances to the Treasury for some years. While this is of little macroeconomic significance, it will not go unnoticed, particularly in an era when the government will be struggling to reduce deficits. This could place considerable short-term pressure on the Fed to prevent those losses by tightening policy more slowly than might otherwise be appropriate. If, instead of asset sales, the Fed tries to restrain credit growth by increasing the interest rate paid on excess reserves, this too would reduce our remittances to the Treasury as more of the Fed’s income would be paid out to the banks holding the reserves.” (Plosser). It might also weaken the economy more than would the preferred path of policy rates preferred in the absence of constraints imposed by the enlarged balance sheet.

10 Ben S., Bernanke, “Press Conference,” September 13, 2012. Transcript provided by Roll Call Inc., via Bloomberg.

11 “FOMC Policy Statement,” December 12, 2012.

12 Ben S., Bernanke, “Press Conference,” December 12, 2012. Transcript provided by Roll Call Inc., via Bloomberg.

13 The Fed was not purchasing assets at that time, but was reinvesting all payments of principal on its holdings. Thus, the principles indicated that, as the first step in the process of policy normalization, the FOMC would “likely first cease reinvesting some or all payments of principal on the securities holdings in the SOMA.” In our view, it is reasonable to assume that the cessation of asset purchases (active balance sheet expansion) would precede the cessation of principal reinvestment (passive balance sheet contraction). The “Exit Strategy Principals” section of the June 21-22, 2012 FOMC minutes appears in its entirety as an appendix to this document.

Appendix I – FOMC Meeting Participants’ Views of the Appropriate Course of Asset Purchases

(December 11-12, 2012)

Views of the 12 voting members of the FOMC (excerpted from “Minutes of the Federal Open Market Committee,” December 11-12, 2012)

In considering the outlook for the labor market and the broader economy, a few members expressed the view that ongoing asset purchases would likely be warranted until about the end of 2013, while a few others emphasized the need for considerable policy accommodation but did not state a specific time frame or total for purchases. Several others thought that it would probably be appropriate to slow or to stop purchases well before the end of 2013, citing concerns about financial stability or the size of the balance sheet. One member viewed any additional purchases as unwarranted.

Views of the 19 FOMC meeting participants, including the 12 voting members (excerpted from “Summary of Economic Projections of the Meeting of December 11-12, 2012”)

Most participants thought it was appropriate for the committee to continue purchasing MBS and longer-term Treasury securities after completing the maturity extension program at the end of this year. In their projections, taking into account the likely benefits and costs of purchases as well as the expected evolution of the outlook, these participants were approximately evenly divided between those who judged that it would likely be appropriate for the Committee to complete its asset purchases sometime around the middle of 2013 and those who judged that it would likely be appropriate for the asset purchases to continue beyond that date. In contrast, several participants believed the Committee would best foster its dual objectives by ending its purchases of Treasury securities or all of its asset purchases at the end of this year when was completed.

Appendix II – FOMC Exit Strategy

(Excerpted from “Minutes of the Federal Open Market Committee,” June 21-22, 2011)

Exit Strategy Principles

The Committee discussed strategies for normalizing the stance and conduct of monetary policy, following up on its discussion of this topic at the April meeting. Participants stressed that the Committee's discussions of this topic were undertaken as part of prudent planning and did not imply that a move toward such normalization would necessarily begin sometime soon. For concreteness, the Committee considered a set of specific principles that would guide its strategy of normalizing the stance and conduct of monetary policy. Participants discussed several specific elements of the principles, including how they should characterize the monetary policy framework that the Committee would adopt after the conduct of policy returned to normal and whether the principles should encompass the possible timing between the normalization steps. At the conclusion of the discussion, all but one of the participants agreed on the following key elements of the strategy that they expect to follow when it becomes appropriate to begin normalizing the stance and conduct of monetary policy:

• The Committee will determine the timing and pace of policy normalization to promote its statutory mandate of maximum employment and price stability.

• To begin the process of policy normalization, the Committee will likely first cease reinvesting some or all payments of principal on the securities holdings in the SOMA.

• At the same time or sometime thereafter, the Committee will modify its forward guidance on the path of the federal funds rate and will initiate temporary reserve-draining operations aimed at supporting the implementation of increases in the federal funds rate when appropriate.

• When economic conditions warrant, the Committee's next step in the process of policy normalization will be to begin raising its target for the federal funds rate, and from that point on, changing the level or range of the federal funds rate target will be the primary means of adjusting the stance of monetary policy. During the normalization process, adjustments to the interest rate on excess reserves and to the level of reserves in the banking system will be used to bring the funds rate toward its target.

• Sales of agency securities from the SOMA will likely commence sometime after the first increase in the target for the federal funds rate. The timing and pace of sales will be communicated to the public in advance; that pace is anticipated to be relatively gradual and steady, but it could be adjusted up or down in response to material changes in the economic outlook or financial conditions.

• Once sales begin, the pace of sales is expected to be aimed at eliminating the SOMA’s holdings of agency securities over a period of three to five years, thereby minimizing the extent to which the SOMA portfolio might affect the allocation of credit across sectors of the economy. Sales at this pace would be expected to normalize the size of the SOMA securities portfolio over a period of two to three years. In particular, the size of the securities portfolio and the associated quantity of bank reserves are expected to be reduced to the smallest levels that would be consistent with the efficient implementation of monetary policy.

• The Committee is prepared to make adjustments to its exit strategy if necessary in light of economic and financial developments.

This material is provided for informational purposes only and is not intended to be a solicitation for any T. Rowe Price products or services. Recipients are advised that T. Rowe Price shall not offer any products or services without an appropriate license or exemption from such license in the relevant jurisdictions. This material may not be redistributed without prior written consent from T. Rowe Price. The contents of this material have not been reviewed by any regulatory authority in any jurisdiction where this presentation is being made or by any other regulatory authority. This material does not constitute investment advice and should not be exclusively relied upon. Investors will need to consider their own circumstances before making an investment decision.

T. Rowe Price, Invest With Confidence and the Bighorn Sheep logo is a registered trademark of T. Rowe Price Group, Inc. in the United States, European Union, Australia, Canada, Japan, and other countries. This material was produced in the United Kingdom.

The views contained herein are as of January 11, 2013, and may have changed since that time.

Copyright © 2013 by T. Rowe Price Associates, Inc.

All rights reserved.