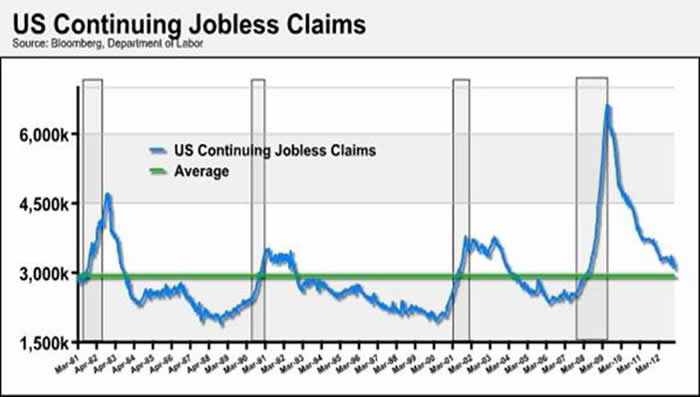

The continuing jobless claims relative to past measurements has been a chart we like to detail to show the more psychological impact of where we stand and the sentiment about the employment situation. As we have shown, the current level is just below the high points of past recessions (recessions denoted by gray rectangles). Although we are approaching the long-term average, currently 6.7% above the 30-year average, the negative sentiment is understandable.

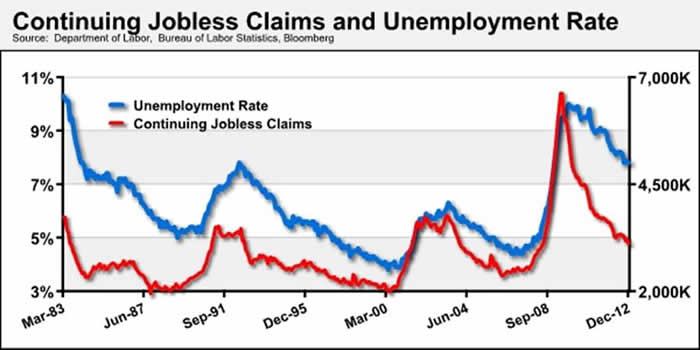

To take another aspect, consider the continuing claims and the unemployment rate. The interesting component is the sharpness in the rise and fall of the U.S. continuing claims relative to the unemployment rate.

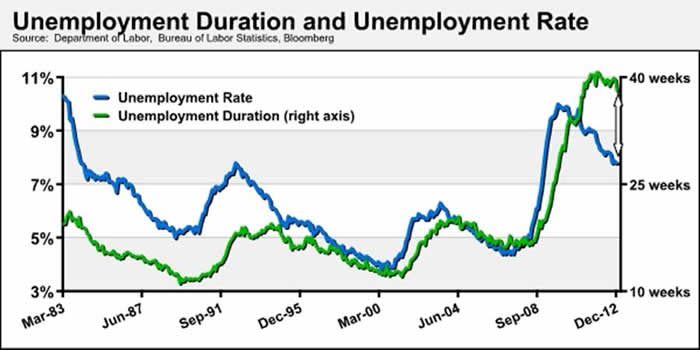

Lastly, the most intriguing argument that we might be on the precipice of a sharp decline in the unemployment rate is the potential rolling over of the amount of weeks for the unemployed. This gap between the unemployment rate and duration helps feed the anxiety over the employment situation much like the continuing claims chart above has shown.

You also continue to see a steady increase in jobs created in the private sector as well as the average hours worked weekly at 34.5 hours, which is above the 34.3 hours averaged over the last seven years. These continue to point to an employee who is asked to work more hours as companies attempt to meet demand but maintain flexibility should revenue begin to decline.

Although we are continuing to run into more headwinds and “boogey men,” both real and imagined, there are trends in place that could well catch most investors and prognosticators by surprise in how quickly the jobs market may come back. It is still pragmatic to predict an improving job market; however, when we find so many people leaning in one direction, more often the opposite is realized.

© Advisors Asset Management