The US Congress kicked the fiscal cliff down the road

January 4, 2013

- The US Congress kicked the fiscal cliff down the road

- Holiday sales in the US were tepid

- December’s job report will not impress the Fed

They say that motivated men and women can move mountains. At the end of 2012, American legislators did just that, but not in a good way. The more I reflect on the deal that averted the fiscal cliff, the less I like it.

What began eighteen months ago as an effort to regain long-term fiscal sustainability devolved so completely that a last-minute accord was required to head off a very unfortunate economic outcome. The clock on this process had been ticking since August 2011, when Congress formed a budgetary “super committee.” This group of six members from each side was given three months to recommend $1.5 trillion in deficit reductions over ten years.

The failure of this august group (which seemed destined from the start) triggered the automatic changes which were to take place this week. Yet the steps creating the fiscal cliff were never intended to go into place as written; the indiscriminate reversion of tax rates and cuts to spending programs were supposed to be so unappealing that legislators would be moved to find more intelligent and lasting solutions.

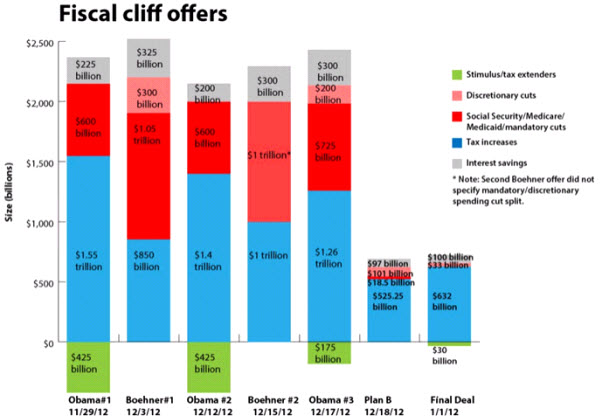

The chart below from the Washington Post provides an interesting illustration of the year end negotiations.

The blue bars show that the two sides were getting very close on tax policy. The red bars show that differences on spending were also narrowing. A “grand bargain” seemed possible. Then, a week before Christmas, something changed and all momentum seemed to be lost.

The American Taxpayer Relief Act of 2012 (ATRA) raises far less revenue than either side would have wanted, and only about a third of what would have been raised had we gone over the cliff. To be sure, some of the tax changes that were scheduled to take hold this week were seen by many as extreme. Approximately half of the relief granted by ATRA will go to the roughly 25 million families who would have been newly ensnared by the alternative minimum tax (AMT). Fixing this feature seemed proper to both sides and significantly reduced the potential drag on consumer spending.

But the status quo was also preserved for a long list of tax preferences. This analysis from the Joint Committee on Taxation inventories the 52 personal, business, and energy tax “extenders,” which afford special treatment for (among other things) electric motorcycle purchases, Caribbean rum production, and motorsports racing track facilities. Publicly, members of Congress rail against deficits, but they privately work to preserve special handling for their favorite constituents. This certainly does not bode well for the type of broad-based reform that many think the US tax code desperately needs.

Those who had become weary of the coverage surrounding the fiscal cliff (which included a countdown clock on CNBC) can expect only a brief holiday. Automatic spending cuts were deferred for only two months, and as we mentioned in our January 2 update, the end of this window coincides with the exhaustion of borrowing room under the Federal debt ceiling. Discussions are not expected to get too serious until the President delivers a draft budget toward the end of this month. That does not leave legislators much time.

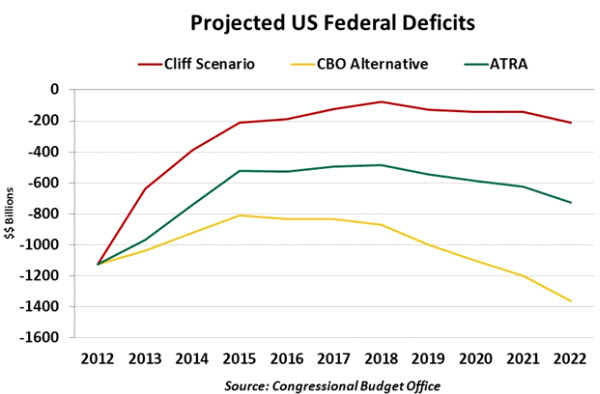

There is much work to be done. Absent further changes, federal deficits will remain sizeable under ATRA.

Many who voted against ATRA would have preferred a comprehensive package of tax increases and spending cuts. Those individuals will certainly place a lot of emphasis on attacking the cost side in the next round, and might view the debt ceiling as a lever to be used to gain concessions. If Congress and the Administration are unable to return to the positive negotiating tone they shared in early December, last-minute brinksmanship is likely, and a second run at debt default cannot be ruled out.

Meanwhile, the economy is left with a modest drag on consumer spending, as the payroll tax reverts to its normal level and higher marginal rates take effect for high income taxpayers. And economic actors are left with just as much uncertainty, if not more, over the outlook for 2013. It appears that the best we can hope for is a patch that averts the now-repositioned cliff. Broad reform of either the tax code or entitlements seems impossibly far off.

When Wile E. Coyote went over cliffs, he often remained suspended blissfully in mid-air for a few moments. It was only when he looked down that the inevitable descent began. Here’s hoping that Congress keeps its eyes on the horizon, and finds a way to return us to terra firma.

2012 Holiday Spending Tally Points To Soft Gains

The uncertainty over the fiscal cliff may have contributed to a holiday sales season that was not the bright spot retailers had been hoping for. The MasterCard Pulse tally for retail sales from Black Friday through Christmas Eve reported only a 0.7% increase from a year ago versus a 2.0% gain recorded in 2011. Estimates of online retail sales also indicate an outcome that is noticeably less impressive than last year’s. There were a few temporary factors that played a role in trimming spending in the fourth quarter and there are some broader issues that will continue to hinder consumers going forward.

Hurricane Sandy dampened retail sales in the Northeast by diverting purchases to rebuilding of damaged homes and away from discretionary items. Nationally, consumer sentiment measures fell in December, partly reflecting the impact of many tax-related unknowns that were bound up in the fiscal cliff negotiations. These influences should fade as the recovery from Sandy progresses and as understanding of the new tax regime takes hold.

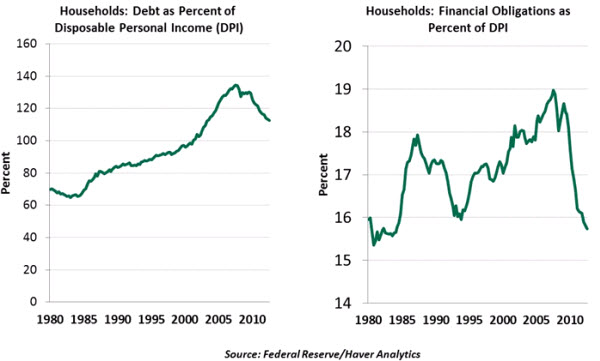

A more lasting influence on household spending is the deleveraging of household debt that has been underway for several quarters. Household debt levels have declined since the peak seen prior to the onset of the financial crisis. Although debt service obligations have dropped to levels last reported in 1984 (thanks to very low interest rates), the elevated debt burden is a significant headwind that continues to hold back consumer spending.

A 16.1% annualized increase in auto sales in the fourth quarter softened the blow to overall consumer spending in the final three months of 2012. Going forward, though, we expect frugality to remain. And that could mean stress on the other side of the cash register, as retailers struggle to sustain sales and profits.

Employment Gains: Steady Is Not Good Enough

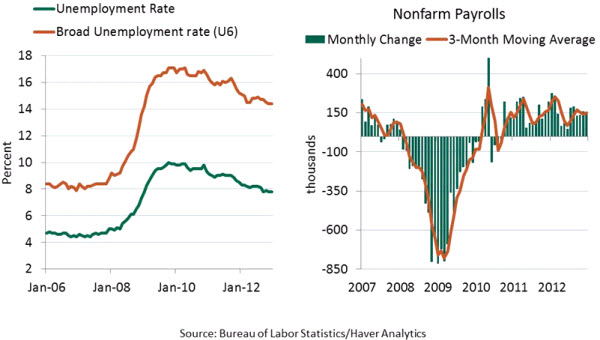

The unemployment rate was unchanged at 7.8% in December and 155,000 new jobs were created. These headline numbers typified the current status of the labor market – not too hot, not too cold. But at the top of the economic wish list for 2013 is a more robust pace of hiring to bring down the jobless rate a bit more rapidly.

Delving in to the details, annual revisions of the household survey numbers led to small changes in previously estimated rates of unemployment. The jobless rate in December (7.8%) matches the November unemployment rate, which was revised up one notch from the earlier estimate of 7.7%. The participation rate edged down to 63.6% in December, down from 63.8% in the prior month. The broad measure of unemployment in December (14.4%) has registered a gradual decline from 15.2% a year ago.

Measures of the duration of unemployment also point to modest improvement during the year, with the median duration of unemployment now at 18 weeks, down from 20.8 weeks at the close of 2011. Pulling these numbers together, the conclusion is that the past year recorded a number of positive developments on the labor front.

From the establishment survey data, private-sector firms created 168,000 new positions in December, while government payrolls fell 13,000. The net gain of 155,000 new jobs in December is close to recent trends (151,000 and 160,000 for 3-month and 6-month averages) and the average for the entire recovery in payroll employment (141,000) which commenced in March 2010. As noted earlier, the bottom line is that data from both the household and establishment surveys are modest improvements, at best.

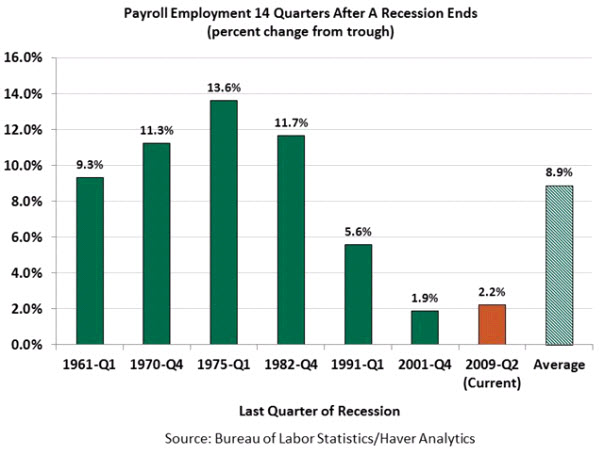

The Fed has set the labor market as the key sector that will guide its monetary policy decisions. The December policy statement and associated rhetoric identified numerical thresholds for when it would raise the federal funds rate and a qualitative threshold of “substantial improvement” in the labor market for termination of quantitative easing. The December employment news by no means meets the latter requirement and the chart above drives home the point that hiring in the current recovery lags its predecessors by a large measure and gives an upper hand for the doves on the FOMC, for now.

© Northern Trust