2013 Forecast: Good Economy, Challenged Markets

Introduction

We enter 2013 bombarded by conflicting signals. While fundamentals have been mixed of late, longer-term themes — our “tectonic shifts” like the energy revolution — are gaining momentum and promising to make positive contributions sooner rather than later. And while salutary measures taken by policymakers have eased global risks and lessened fears of Armageddon, there is considerable work yet to be done.

You wouldn’t know it to look at fund flows, but markets have been unequivocal in their support of the post-Great Recession environment. In fact, the three-year-plus run since early 2009 can best be described as a “stealth bull market” — though asset classes of all stripes delivered outsized returns, the record amount of cash on the sidelines suggests few investors took notice. Opportunity abounded for investors with an even moderate exposure to risk, as a broad cross section of global asset classes — both equity and fixed income — experienced double-digit rallies. The past three years will go down as a time when, due to unwarranted pessimism on the global risk front, investors overlooked or even ignored improving fundamentals, choosing instead to stay largely out of the market in a classic example of the folly of gaming diversification.

No doubt 2013 will present many challenges and opportunities in markets that given a more stable global macroeconomic environment should once again be driven primarily by fundamentals. Since it is imperative to have a clear and unequivocal understanding of today’s fundamentals, let’s begin our 2013 forecast there.

2013: Good Economy, Challenged Markets

The global economy is in reasonably good shape if you look only at the level of economic progress. Based on several key metrics — including gross domestic product, S&P 500 corporate profits, retail sales and exports, all of which have reached record highs — the U.S. economy made it through recovery and moved into expansion since the trough of the Great Recession. The crisis that has consumed Europe in recent years has abated thanks to strong policy action by the European Central Bank (ECB), remedial measures designed to promote a fiscal and banking union, and progress toward political integration. Emerging markets largely avoided the debt crisis, becoming a bright spot for world growth and trade. Unfortunately, markets do not buy levels — they buy growth. And growth from here looks to be a challenge.

Given a plethora of mitigating factors, we have been only moderately concerned by the global risks over the past few years. The lack of growth in the euro zone as a whole was offset by the outsized impact of a strong, export-driven Germany. Japan teetered on the precipice of recession, as it has on-and-off for the past 20 years or so. China has slowed, but most indicators suggest it sidestepped a hard landing. We have faced significant obstacles since coming out of the recession, and the global economy has repeatedly demonstrated its resilience with an awe-inspiring, fundamentally supported comeback.

But the wind is not in the sails of the fundamentals this time. For example, quarterly year-over-year earnings growth of the S&P 500 — our primary fundamental market indicator and typically a reliable predictor of future earnings growth — went negative in the third quarter. Consensus expectations for fourth quarter growth have dropped precipitously, falling from over 9% at the end of September to 2.4% currently, and we think even this may be too high. The S&P 500 derives more than half its revenue from overseas, and there is no question that a global economy under duress is pressuring corporate profits.

Of course, the overall fundamental picture is broader than just corporate profits, and there is positive news to be found. Collectively, fundamentals are so basic to successful investing that we categorize them as the “ABCDs” that drive the markets. They are:

A: Advancing corporate profits

B: Broadening manufacturing

C: Consumer as the game changer

D: Developing economies

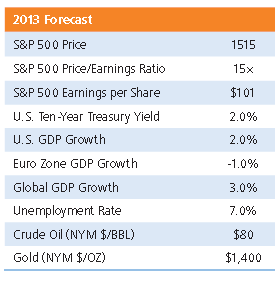

Advancing corporate profits. The third quarter saw corporate profits experience negative year-over-year growth for the first time in three years. In an example of the “cockroach theory” — which states that the emergence of one piece of bad news suggests more is looming — a negative quarter of earnings tends to be predictive of additional negative quarters. Of the ABCDs of fundamentals, the direction of corporate profits is the canary in the coal mine, signaling that conditions are worse than the other indicators would suggest. In fact, it is our signature factor in determining when to be defensive or fully invested. Our forecast for S&P 500 2013 earnings is $101 per share, less than the $105 per share we forecasted for 2012. Combined with a price-to-earnings multiple of 15 — we expect multiple expansion from current levels given the extraordinary monetary easing by central banks around the world — this gives us a year-end 2013 price target of 1515 for the S&P 500.

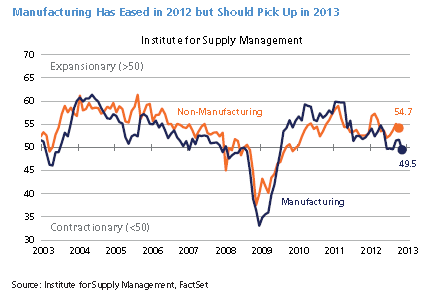

Broadening manufacturing. The uncertainty in Europe, the slowdown in China and the fear of falling off the fiscal cliff contributed to a manufacturing slowdown in 2012. However, we anticipate manufacturing will strengthen as these uncertainties abate, and it will accelerate based on an energy revolution fueled by inexpensive natural gas, as well as China’s waning ability to maintain a producer price advantage (labor costs have increased by more than 15% per year). Meanwhile, industrial production in the U.S., as measured by the Industrial Production Index, is increasing faster than in all other developed markets, including Germany and China.

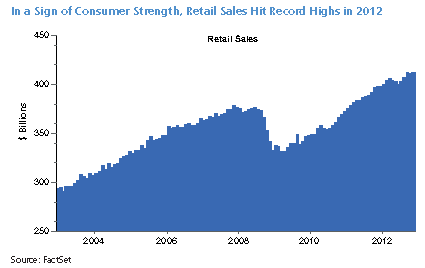

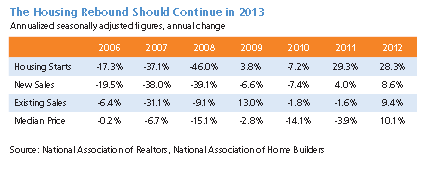

Consumer as the game changer. The resilience of the U.S. consumer — responsible for 70% of GDP growth — has been underestimated and is a true fundamental game changer. Retail sales reached all-time highs in 2012, surpassing $412 billion per month, as consumers continued to buoy the economy with their spending. While this is partly due to slow but steady improvements in the employment picture — as we forecast at this time last year, unemployment has fallen below the 8% mark — the housing market is the key to consumer resilience and renewed confidence.

Housing numbers across the board have signaled a turnaround, and we expect the trend to continue. Housing has a profound multiplier effect across the economy, and we believe the Federal Reserve targeted its latest quantitative easing efforts at housing in order to spur consumer confidence. This accommodation may have unintended consequences, though; pent-up housing demand combined with the best affordability levels in a decade may drive cash on the sidelines into housing speculation rather than securities markets, a potential negative for stocks.

Developing economies. Emerging markets are a key catalyst for global growth and helped the U.S. avoid a recession in 2012. We expect that U.S. corporations will continue to be the number-one beneficiary of emerging market growth; this is especially true in the technology sector, where almost 57% of total sales come from outside the U.S. (based on 2011 data).

Global Risks Have Eased but Continue to Challenge Fundamentals

Though policymakers the world over have taken steps to avoid the worst-case scenarios, their work is far from over.

European debt crisis. Europe has made considerable progress in addressing its issues. Finance ministers recently established a “single supervisory mechanism” under the auspices of the European Central Bank to oversee the region’s largest banks beginning in March 2014, another step forward after massive ECB stimulus programs successfully stemmed the risk of debt contagion earlier in the year. However, the European crisis will not truly be over until the euro zone recession ends and the region is able to transition away from a bifurcated union marked by a successful Germany and a mediocre collection of other economies. The Germans can’t do it alone, and we are now seeing signs in the all-important industrial production figures that its economy is beginning to wilt. We expect continued turmoil out of Europe in 2013; however, the market’s main focus will likely shift away from Spain and toward Italy and — surprise! — France.

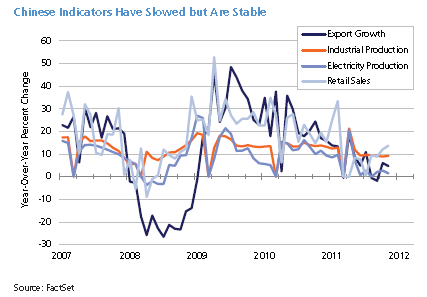

Chinese hard landing. China needs to transition from an export-driven economy to a consumer-driven one. China’s “state capitalism” — in which profits are secondary to growth and power — is slow and ineffective but still critical to global growth. Excesses are becoming apparent, exemplified by the oversupply of commodities, unclear debt levels and flat-lined exports. Nevertheless, the recent transition in leadership heightens the chance that growth will be sustained, though it may be more precarious going forward.

U.S. debt and growth crisis.U.S. debt is 100% of GDP, a level not seen since World War II. In 2011, Standard & Poor’s downgraded the country’s credit rating despite the passage of the Budget Control Act of 2011 only days prior. Since dubbed the “fiscal cliff” by Ben Bernanke, the act — scheduled to take place at the start of 2013 to address America’s unsustainable debt path — contains a series of draconian tax increases and spending cuts likely to derail economic growth into recession.

But a recession on positive debt reduction is better than continuing to risk an additional downgrade from the ratings agencies. The fiscal cliff would also lower the future trajectory of debt and thus the expectation of future taxes. We prefer to take the pain now and go over the fiscal cliff with only minor modifications to make it more palatable to the electorate. But to kick the can down the road on debt would be the worst course of action for the economy and markets in the long run.

Meanwhile, there are other laws and pending federal actions whose effects are only beginning to be fully understood:

- The Affordable Care Act (aka Obamacare) is scheduled to immediately raise Medicare taxes and meaningfully impact the dynamics of the health care industry, which is one-sixth of the U.S. economy.

- The Dodd-Frank Wall Street Reform and Consumer Protection Act is the most significant change in financial regulation since the Great Depression.

- Quantitative easing by the Fed has indisputably helped heal the economy and provide some clarity in uncertain times. But the Fed has continued to tinker in recent months, committing to:

- QE3: $40 billion per month of mortgage-backed security purchases

- QE4: $45 billion per month of long-term Treasury purchases without a corresponding sale of short-term notes, thus expanding the Fed balance sheet (in effect, printing money)

- Meeting explicit targets for employment and inflation before it will consider raising its key policy rate

The U.S. is still the global reserve currency, but its credit rating is in jeopardy of another downgrade if lawmakers are unable to devise a credible solution to the fiscal cliff. Nevertheless, the question remains whether these policies will be beneficial to economic growth and, if not, where growth will come from.

The risk of global deflation. Those who have spent the past three years preparing for inflation are likely to again be disappointed in 2013. In fact, we would welcome a certain amount of inflation, as reflation of price levels back up to more reasonable levels — say, ten-year Treasury yields above 3% — would suggest a healthy economy. In fact, at this point we think deflation is equally as likely to occur. Though this opinion deviates from the consensus, we believe it’s prudent to consider given how unmanageable and contagious deflation tends to be. Meanwhile, the Federal Reserve’s aggressive policy actions suggest that the central bank considers deflation more than a trivial concern.

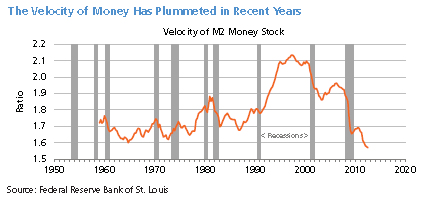

From a monetarist perspective, deflation can happen because of 1) a drop in the money supply due to a lack of credit and/or 2) a drop in the pace at which money is changing hands (i.e., the velocity of money). Most of the money the Fed is currently pumping into the system is ending up in bank reserves rather than being lent, meaning velocity is down (as you can see in the accompanying chart from the St. Louis Fed). The central bank continues to expand its asset-purchase programs and quantitative easing efforts, and has now established explicit employment and inflation targets in its dual-mandate role. These actions also could be viewed as thinly veiled salvos against deflation, though they impact only the monetary side of the equation and not the more important velocity of money component. While deflation is less evident in the U.S. than it is in Europe and Japan, we remain concerned.

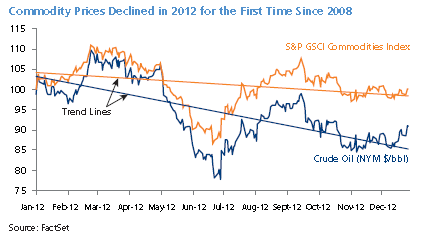

If changes in commodity prices are assumed to roughly reflect inflation, the potential for deflation becomes even more evident. Despite drought-related price surges in some agricultural commodities, the S&P GSCI — a tradable index produced by Standard & Poor’s that tracks 24 commodities across sectors — declined this year for the first time since 2008 as weak global demand suppressed prices across the board. Moreover, supply has increased due to either technological advancements or commodity producers hoping to cash in on the all-time-high price levels achieved over the last few years. The Fed’s quantitative easing has spurred widespread expectations of commodities inflation, which has not materialized. We anticipate Nymex crude oil will moderate further from its current $90/barrel price, as proposed pipelines move oil from the Midwest to Gulf Coast refineries.

Tectonic Shifts in the Global Economy

Traditional short-term market forecasts typically ignore trends that are slow moving, hard to measure and/or veiled in their influence on the global economy. Disregarding these sub-surface themes is a critical gap in forecasting methodology because, like continents colliding, their explosive intensity may have the power to change the face of the earth. We call these trends “tectonic shifts” and regard them as a meaningful part of the surprises in advancing corporate earnings, broadening manufacturing, unanticipated consumer strength and global market resilience in the face of the Armageddon scenarios favored by the financial press.

Any 2013 forecast is short term relative to these secular trends; while we see the influences build year by year, it is difficult to know when the impacts will be felt in earnest. The best we can say is that these trends will support — or potentially lead — to positive surprises in the markets. Note, however, that politicians in their infinite wisdom often try to control these forces through new laws and regulations, sometimes dampening their full potential.

Energy. Tectonic shifts in energy — led by new technologies to tap into natural gas stores deep under the surface of the earth — are expected to lead the U.S. to energy independence by 2020. We expect the themes below to play out over the next several years.

- Exports in natural gas and coal make an enormous positive contribution to U.S. economic growth while imports plummet due to the self-sustaining energy boom in North America.

- The U.S. trade deficit ultimately will become a trade surplus for the first time since 1975, and the dollar will strengthen relative to other developed nations.

- Natural gas gives manufacturers an 80% cost advantage over foreign competitors, unleashing an investment wave in such U.S. industries as petrochemicals, fertilizer, natural gas export and steel production.

- Natural gas at $3 replaces oil at $90 as feedstock for diesel fuel. As a result, transportation costs plummet, to the benefit of both businesses and consumers.

Technology. Technological advances are not only manifesting themselves in the energy arena.

- In developed nations such as the U.S., the main thrust of technology is moving from “cost containment and productivity improvement of current processes” to “revenue enhancement and business transformation”. This is “Big Data”, and the firms that embrace it will be on the forefront of the revolution. Big Data leverages the massive amounts of information generated by mobile commerce, social media, and consumer and business profiling and tracking, and it has the potential to transform all sectors of the economy, including the consumer discretionary, health care, industrials, financials and energy industries. Omni-channel retailing (through which retailers seek to meet the needs of consumers through all available shopping channels — mobile devices, bricks and mortar stores, catalogs, etc.) is one example of a Big Data application that may transform the customer and supplier experience.

- In developing nations, the benefits are not as easily measured but are still impressive. Ten years ago, less than 1% of the African population had access to landline telephones; now 70% of the population has mobile phones. Coincidently, Africa’s GDP has increased 5% on average each year for the last ten years.

- Technology is not just entertainment and convenience, it is empowerment. And it will drive change.

New emerging and frontier economies. With the slowdown in China felt around the world, the question is who will pick up the slack. The answer is the newly emerging markets — aka, the frontier markets. Frontier countries have younger populations, better government financial ratios and higher growth trajectories than developed nations. In Columbia, 40% of the population is below age 20, and 80% is below age 50.

- Poland was the only European country to avoid recession during the post-Lehman 2008 financial crisis.

- The rising African consumer class has higher household consumption than Russia or India.

- Based on labor rates, logistics and currency fluctuations, Mexico has become the cheapest place in the world to manufacture goods intended for sale in the U.S. And Mexico’s growth trajectory will push its economy into the world’s top ten by 2020.

- The ASEAN (Association of Southeast Asia Nations) consortium represents a population of more than 3 billion and GDP of $17 trillion. It is estimated that within ten years, Southeast Asia will trump China as the home of low-cost manufacturing.

- Indonesia is the fourth most populous country in the world, has a debt-to-GDP ratio of only 25% and its sovereign bonds were upgraded to investment grade in 2012.

- While the term “BRIC” has been synonymous with emerging growth over the last 20 years, it may be time to suggest a new acronym. We offer “PIVOT” (Peru, Indonesia, Vietnam, Oman and Turkey) as frontier markets move to the front of the global economy.

Global trade. Trade is the wrapper that facilitates new energy exploration, technological advancements and the emerging economies clamoring for infrastructure, goods and services.

- A significant global rebalancing is underway. Net importing countries — like the U.S. — are now exporting more; U.S. exports rose to 13.5% of GDP in 2011, the highest level ever, and the trade deficit remained under 4% of GDP. Meanwhile, net exporters — like China — have seen their trade surpluses sink; China’s trade surplus fell to 2.5% of GDP in 2011, down from more than 10% five years ago.

- But global trade is not all about the U.S. In fact, trading among emerging markets — often referred to as “south/south” trade routes — makes up one-fifth of the world’s total trade and is expected to surpass trade flows between developed and developing economies by 2030.

- Traditionally, the intra-emerging market trade was concentrated in Asia, but market opportunities in Asia and Latin America as well as within sub-Saharan Africa abound. Exports from sub-Saharan Africa to Asia alone are expected to increase by 14% in the next decade.

Portfolio Positioning: Defensive in 2013

“Stay the course” was typically considered sage investment advice until this last decade. With two bear markets over the past ten years, however, this phrase has lost its resonance. Instead, we advocate having a plan that employs rare but unequivocal signals about when to become defensive to avoid market dislocations. Our guideline in these circumstances is to ratchet risk levels down, not by an order of magnitude but certainly from (in military parlance) DEFCON 3 to DEFCON 4.

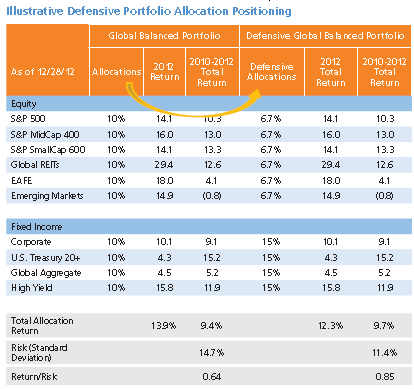

The fundamentals we explained in this forecast have led us to a defensive stance as of the first business day of January 2013. While we remain broadly and globally diversified, we have tilted our bias away from equity and toward fixed income. The figure below illustrates the impact such a defensive posture would have had on a hypothetical portfolio over the past three years; as you can see, returns would have been similar despite a significant reduction in risk over the three-year period.

As we’ve said time and time again, gaming diversification is folly; however, adjusting risk exposure in the face of formidable evidence is prudent portfolio management. And note that while the repositioning is designed to provide downside protection, the past three years did not show a symmetrical impact on return; that is, the allocation would have limited losses without an equivalent reduction of upside potential. Though the past three years can hardly be regarded as typical in the context of very long time frames, the experience suitably exemplifies the conditions we see today.

In general we advocate a broadly diversified portfolio in order to avoid gaming diversification. However, we acknowledge that some asset classes may have a stronger investment outlook than others at this juncture.

- Mid-cap stocks have the financial wherewithal of a large company but the growth prospects of a small one, making them the sweet spot of the U.S. domestic market. Despite its issues, the U.S. continues to have the best prospects in the global economy based on the tectonic shifts we discussed earlier.

- Global bonds issued by lower-debt nations not only offer attractive yield opportunities, they help increase portfolio diversification via the many currencies in which they are available. While the U.S. dollar remains the global reserve currency, investors tend to be overexposed to it and any reduction helps.

- Consumer discretionary stocks are our favorite sector; the continued largesse of the Fed should keep interest rates low indefinitely, to the benefit of the housing market and, by extension, consumer spending.

Conclusion

A good economy is not necessarily a good market. A good market depends on growth in fundamentals; with U.S. corporate earnings going negative in the third quarter, it’s clear that serious problems are afoot in the global economy and that future growth may be hard to come by.

There are numerous catalysts that will have a positive long-term effect on the global economy and market fundamentals, and they may even find a way to positively impact the 2013 environment. In the meantime, however, we advocate a defensive stance until the markets “show me the money” in terms of fundamental growth.

Index Definitions

Barclays Capital U.S. Corporate Bond Index is a component of the Barclays Capital U.S. Aggregate Index.

Barclays Capital U.S. Treasury Bond Index is a component of the Barclays Capital U.S. Aggregate Index.

Barclays Capital Global Aggregate Bond Index measures a wide spectrum of global government, government-related, agencies, corporate and securitized fixed-income investments, all with maturities greater than one year.

Barclays Capital U.S. Corporate High-Yield Bond Index tracks the performance of non-investment grade U.S. dollar-denominated, fixed rate, taxable corporate bonds including those for which the middle rating of Moody’s, Fitch, and S&P is Ba1/BB+/BB+ or below, and excluding Emerging Markets debt.

FTSE EPRA/NAREIT Global Real Estate Index is designed to represent general trends in eligible real estate equities worldwide.

MSCI EAFE Index is a free float-adjusted market capitalization weighted index designed to measure the developed markets’ equity performance, excluding the U.S. & Canada, for 21 countries.

MSCI Emerging Markets Index is a free float-adjusted market capitalization index that measures emerging market equity performance of 22 countries.

S&P Mid-Cap 400 Index is a benchmark for mid-sized companies, which covers over 7% of the U.S. equity market and reflects the risk and return characteristics of the broad mid-cap universe.

S&P Small-Cap 600 Index covers approximately 3% of the domestic equities market and is designed to represent a portfolio of small companies that are investable and financially viable.

S&P 500 Index is a gauge of the U.S. stock market which includes 500 leading companies in major industries of the U.S. economy.

This review has been prepared by ING U.S. Investment Management for informational purposes. Nothing contained herein should be construed as (i) an offer to sell or solicitation of an offer to buy any security or (ii) a recommendation as to the advisability of investing in, purchasing or selling any security. The material presented is compiled from sources thought to be reliable, but accuracy and completeness cannot be guaranteed. Any opinions expressed herein reflect our judgment and are subject to change. Certain of the statements contained herein are statements of future expectations and other forward-looking statements that are based on management’s current views and assumptions and involve known and unknown risks and uncertainties that could cause actual results, performance or events to differ materially from those expressed or implied in such statements. Actual results, performance or events may differ materially from those in such statements due to, without limitation, (1) general economic conditions, (2) performance of financial markets, (3) interest rate levels, (4) increasing levels of loan defaults, (5) changes in laws and regulations, and (6) changes in the policies of governments and/or regulatory authorities.

Past performance is not a guarantee of future results. The index returns are shown for illustrative purposes only and do not represent the returns of any particular investment product. The index figures do not reflect any fees, expenses or taxes. Investors cannot invest directly in an index.

© 2013 ING Investments Distributor, LLC • 230 Park Avenue, New York, NY 10169