Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

After my recent conversation on Morningstar’s The Long View podcast, a financial advisor reached out with a message that stayed with me.

She said widows are a community she is especially interested in serving — and that our conversation clarified how intentional advisors need to be before loss occurs. That response pointed to a larger planning issue: Widowhood is not a niche concern. It is one of the most consequential transitions many clients will face in later life.

Yet many retirement plans are built for couples without being fully tested for the person who may one day be left to carry the plan alone.

A couple’s retirement plan may look sound on paper. The assets are adequate. The withdrawal rate is reasonable. The estate documents are signed. But widowhood does not happen on paper.

It happens in the middle of grief, changing income, tax questions, family expectations, housing decisions, administrative demands, and a profound shift in identity. The math may still work, but the human operating system has changed. And that is why advisors need to stress test — not only for portfolio survival, but for survivor usability.

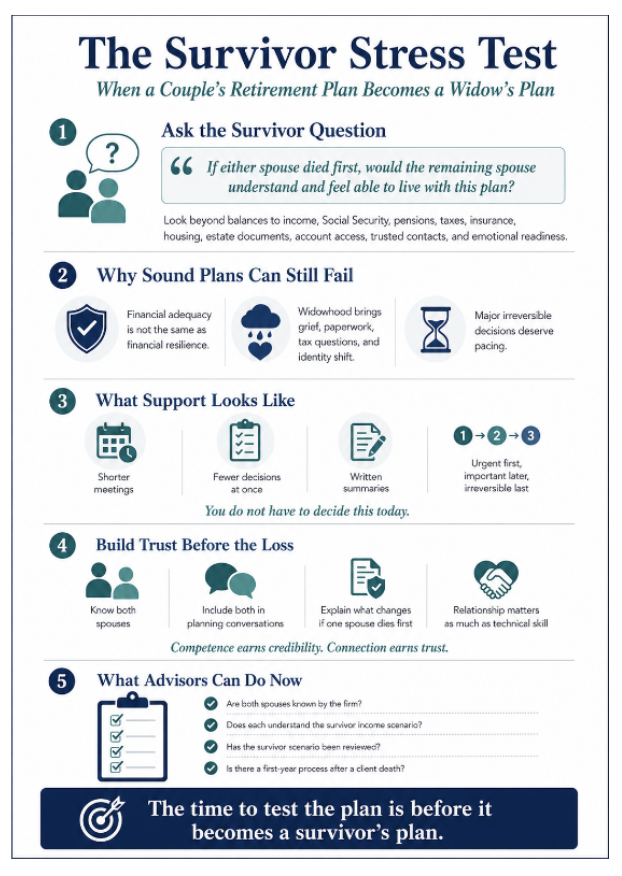

Ask the Survivor Question

A meaningful survivor stress test begins with this question: If either spouse died first, would the remaining spouse understand and feel able to live with this plan?

That question goes beyond account balances. It includes income, Social Security, pension elections, taxes, insurance, housing, estate documents, account access, trusted contacts, and emotional readiness.

Widowhood as a status doesn’t mean that such individuals are less capable, intelligent, or resilient than any other person. However, in the early months after loss, they often describe themselves as being in a fog. Concentration may be impaired. Memory may feel unreliable. Decision-making can feel exhausting. That is not weakness, but a normal response to profound disruption.

Advisors who understand this adjust their process. They shorten meetings, reduce the number of decisions, provide written summaries, and distinguish what is urgent from what can wait. They say clearly, “You do not have to decide this today.”

That sentence may be one of the most valuable forms of advice an advisor can give.

Why Sound Plans Can Still Fail

Many retirement plans are judged successful if the numbers work. But financial adequacy is not the same as financial resilience.

A widow may have enough money and still feel overwhelmed, isolated, unsure whom to trust, or afraid of making a mistake. She may be pressured by family, real estate decisions, tax deadlines, or well-meaning professionals who move too quickly.

The advisor’s role is not to freeze all action. Bills need to be paid. Cash flow must be stabilized. Claims may need to be filed. Benefits need to be reviewed.

But major, irreversible decisions deserve pacing. Some of the highest-risk decisions in the first year are also among the most emotionally charged: selling a home, relocating, changing advisors, making large family gifts, altering investments, or revising estate documents.

One useful framework is: urgent first, important later, irreversible last. That sequence can protect a widowed client from double grief — the emotional grief of losing a spouse, compounded by the financial grief of a decision made too quickly or under pressure.

Build Trust Before the Loss

When widowed clients change advisors, the reason is often not investment performance. It is relationship.

If the advisor’s primary relationship was with the spouse who died, the survivor may feel like a secondary client when they need to feel known, respected, and supported. They may not understand the plan because they were never fully included in building it. They may not know whether the advisor truly sees them as the client now.

Advisors can reduce that risk before a death. Invite both spouses into planning conversations. Ask each person questions directly. Make sure both understand where income would come from if one spouse died first. Explain what would change with Social Security, pensions, taxes, insurance, housing, and family roles.

This is not merely inclusive client service. It is risk management.

With widowed clients, behavioral coaching becomes deeply personal. Call it a form of emotional alpha: the value advisors create by helping clients feel safe, steady, and understood during vulnerable transitions. It may sound like this: “You do not have to remember all of this today. I will write it down.”

Technical competence remains essential. Widows do not need sympathy without skill. They need advisors who can explain the financial details in understandable, respectful language.

Competence earns credibility. Connection earns trust.

What Advisors Can Do Now

Advisory firms can begin by asking a few practical questions:

- Are both spouses known by the firm, or has one partner become the “default client”?

- Does each spouse understand where income would come from if the other died first?

- Has the survivor scenario been reviewed for Social Security, pensions, taxes, insurance, housing, account access, and estate documents?

- Does the firm have a first-year process after a client death?

- Are early meetings shorter, written summaries standard, and urgent tasks clearly separated from decisions that can wait?

A strong financial plan is not just about whether the numbers work. It is about whether life still works when circumstances change. The best plans protect more than assets. They protect confidence, dignity, choice, and peace of mind.

For advisors, the survivor scenario belongs at the center of retirement planning — not after the loss, not in the fog, and not when one spouse is sitting alone asking, “What do I do now?”

The time to test the plan is before it becomes a survivor’s plan.

Kathleen M. Rehl, PhD, CFP®, CeFT® (Emeritus), is an author, educator, and speaker who empowers widows financially and trains advisors in grief-aware client communication. After experiencing widowhood herself, she authored "Moving Forward on Your Own: A Financial Guidebook for Widows". Kathleen continues to teach and write about widows and money, legacy planning, and purposeful aging. Her website is https://www.kathleenrehl.com.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Read more articles by Kathleen M. Rehl

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.