How Wealth Firms Can Productize Their Services in 2026

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

The author used artificial intelligence to assist in the organization and editing of this article.

“Productization” has quickly become one of the most widely used terms in wealth management. It appears in strategy decks, conference discussions, and vendor messaging. Yet, despite its popularity, the concept remains poorly understood in practice.

There is a clear disconnect across the industry: Many firms talk about productization, but very few implement it at an operational level.

This gap exists because productization is often interpreted as a branding or packaging exercise, something tied to how services are presented externally. In reality, it is something far more fundamental.

Productization is the process of transforming your service into a standardized offering with defined variables, pricing, action items and outcomes that can be marketed to a wide range of customers.

Not to be confused with marketing services differently, the concept of productization is about restructuring how advisory capabilities are delivered.

The urgency behind this shift is driven by several structural pressures:

- Rising client expectations for consistency, transparency, and responsiveness;

- Fee compression that demands greater operational efficiency; and

- Increasing complexity from multi-account, multi-custodian environments.

As these pressures intensify, the traditional model of highly customized, manually delivered services becomes harder to sustain. The firms adapting successfully translate their expertise into repeatable, scalable service models, without compromising the quality of advice.

The Misconception: Why Productization Feels Abstract to Most Firms

One of the biggest barriers to productization is conceptual. Wealth management has long been built on a relationship-driven model, where customization is viewed as a core value driver. Advisors pride themselves on tailoring solutions to individual client needs, and for good reason.

However, this has led to a persistent misconception that productization means removing personalization. That’s not the case at all. Rather, productization is about structuring how value is delivered.

In many firms, the delivery of services is highly inconsistent. Two clients with similar needs may have entirely different experiences depending on the advisor, the tools used, or the operational processes behind the scenes.

Common symptoms of non-productized firms include:

- Fragmented workflows across teams and systems;

- Heavy reliance on manual processes and spreadsheets;

- Inconsistent reporting and client communication; and

- Difficulty scaling without adding headcount.

These issues are not always visible externally, but they create internal friction that limits growth and efficiency.

Productization begins with a simple but critical shift: redefining what the firm actually delivers on a recurring basis. Instead of viewing each client engagement as unique, firms identify the underlying services that are repeated across their entire client base.

Turning Advisory Expertise Into Repeatable Services

There are two keys to the process of productizing.

Identify core capabilities. Every wealth management firm, regardless of its size or specialization, delivers a common set of core capabilities, including portfolio construction and asset allocation; risk monitoring and exposure analysis; and performance measurement and reporting, as well as client communication and insights.

The important realization is that these capabilities are consistently delivered across firms. However, firms can differentiate themselves with how they execute those capabilities.

Convert capabilities into service frameworks. Productization requires transforming core capabilities into structured service frameworks. This means introducing consistency across three key dimensions: inputs, processes, and outputs.

Inputs involve standardizing data sources, benchmarks, and models, while processes focus on defining clear workflows for how services are executed. Outputs, in turn, ensure consistency in deliverables such as reports, alerts, and insights.

For example, instead of generating fully customized performance reports for each client, firms can implement standardized reporting templates, apply consistent calculation methodologies, and establish automated delivery schedules. This approach not only improves efficiency, but also enhances reliability and scalability.

Similarly, risk monitoring can be formalized through predefined thresholds and triggers, systematic portfolio reviews, and automated alerts for deviations. By structuring these elements, firms can ensure more proactive and consistent risk oversight.

Importantly, these frameworks do not eliminate customization. Rather, they create a stable and repeatable foundation, enabling firms to deliver tailored advice more effectively and at scale.

Why Repeatability Matters

Repeatability is the mechanism that enables scale. When services are delivered through structured frameworks, variability across clients is significantly reduced, ensuring a more uniform standard of service. At the same time, dependence on individual advisors decreases, as processes become less reliant on personal execution and more driven by defined systems.

As a result, operational processes become more predictable and easier to manage. This predictability allows firms to grow without proportionally increasing operational complexity or staffing levels. It also ensures that every client receives a consistent experience, regardless of which advisor manages their account.

In modern wealth management, scalability is not achieved by simply working harder. Instead, working systematically supports scalability.

Building Modular Service Layers Instead of One-Off Solutions

Traditional service models in wealth management are often monolithic. Each client engagement is treated as a unique combination of services, built from the ground up.

Productized firms take a different approach by adopting modular service architectures. This means breaking services into independent but connected components that can be reused and recombined.

What Modular Service Layers Look Like in Practice

In a modular model, services are delivered through distinct, well-defined layers, each designed to perform a specific function. These may include portfolio rebalancing tools, performance reporting modules, portfolio analytics engines, risk diagnostic tools, and client engagement and insight platforms. Each layer operates independently while contributing to the overall service structure.

Despite their independence, these modules are built to integrate seamlessly with one another. This interconnected approach allows firms to deliver a cohesive and unified service experience without the need to create custom-built workflows for every individual client.

As a result, firms can maintain both efficiency and flexibility, leveraging standardized components while still supporting a high level of service quality and responsiveness.

Modularity Enables Both Scale and Flexibility

The primary advantage of modularity is that it enables firms to balance scale with flexibility. By structuring services into modular components, firms can configure offerings differently for various client segments without rebuilding processes from scratch. This approach allows for greater adaptability while maintaining operational efficiency.

In addition, modular systems make it easier to introduce new capabilities without redesigning the entire infrastructure. Firms can also respond more quickly to regulatory or market changes, as adjustments can be made within specific modules rather than across the entire system.

This leads to a critical insight: Productization does not eliminate flexibility; it redefines it. Instead of repeatedly customizing processes, firms configure pre-built components to meet client needs. This approach is not only more efficient but also far more scalable, enabling consistent delivery alongside tailored outcomes.

Operational Efficiency Through Standardization

Without standardization, wealth management firms often face a range of operational inefficiencies that hinder performance and scalability. These include duplicate processes across teams, manual data reconciliation between disconnected systems, and advisor-dependent workflows that lack consistency. As a result, operations become fragmented, time-consuming, and difficult to manage effectively.

These inefficiencies translate into tangible business challenges. Firms experience a higher cost-to-serve per client, slower onboarding and service delivery timelines, and increased exposure to operational and compliance risks. Over time, these challenges compound, ultimately limiting the firm’s ability to grow in a sustainable and profitable manner.

How Standardization Changes the Operating Model

Standardization introduces structure and consistency into operations, creating a more disciplined and reliable service environment. It involves defining uniform workflows across the organization, establishing clear and repeatable service delivery processes, and implementing automation wherever possible to reduce manual intervention.

The impact of this approach is significant. Firms can reduce their reliance on manual execution, improve consistency in how services are delivered, and make more efficient use of resources across teams. As processes become more streamlined, operations become easier to manage and scale.

Ultimately, standardization transforms operations from being reactive and fragmented into a more proactive and controlled system, enabling firms to deliver higher-quality outcomes with greater efficiency and predictability.

Refocusing Human Capital on High-Value Work

One of the most important benefits of standardization is its impact on how teams allocate their time. When processes are structured and automated, less effort is required for routine execution, allowing both advisors and operations teams to operate more efficiently.

As a result, teams can shift their focus toward higher-value activities such as building deeper client relationships, providing strategic financial guidance, and interpreting data and insights in a more meaningful way. This transition elevates the role of the advisor from executor to strategist.

Ultimately, this shift not only enhances the client experience but also strengthens the firm’s overall value proposition, positioning it as more insightful, responsive, and client-centric. In this way, productization can actually result in greater customization.

The Role of Data Infrastructure in Productization

At its core, productization depends on consistency, and consistency depends on data.

Productized services require:

- Reliable inputs;

- Accurate calculations; and

- Consistent outputs.

However, many wealth firms operate with fragmented data environments spread across custodians, platforms, and internal systems. This makes it difficult to standardize processes or deliver consistent insights.

A robust data infrastructure provides the foundation for productization. This includes:

- Aggregating data from multiple sources;

- Standardizing data into a unified format; and

- Ensuring data accuracy and governance.

With a “single source of truth,” firms can deliver services consistently across their entire client base. Once data is structured and accessible, it becomes possible to automate insight generation.

Examples include:

- Automated performance calculations across all portfolios;

- Real-time risk monitoring and alerts; and

- Consistent reporting outputs delivered at scale.

Technology’s Role in Enabling Productized Services

Technology is often viewed as a supporting layer in wealth management. In reality, it plays a central role in shaping how services are delivered.

Modern platforms do more than automate tasks: They define workflows, integrate data, and enable scalability.

To support productization, technology must provide seamless integration across custodians, systems, and data sources, along with automation of repetitive workflows. It should also enable scalable analytics and reporting to maintain efficiency as firms grow.

As a result, firms are moving away from disconnected tools toward integrated ecosystems that support end-to-end service delivery with greater consistency and scalability.

When implemented effectively, technology becomes a true strategic advantage. It enables firms to deliver insights consistently across all clients, scale operations without adding complexity, and reduce friction across workflows and teams.

Firms leveraging advanced platforms, such as those provided by SoftPak Financial Systems, can operationalize complex capabilities like portfolio analytics and rebalancing. This allows them to deliver services that are both standardized and configurable at scale.

In this context, technology doesn’t just supporting productization, it makes it possible.

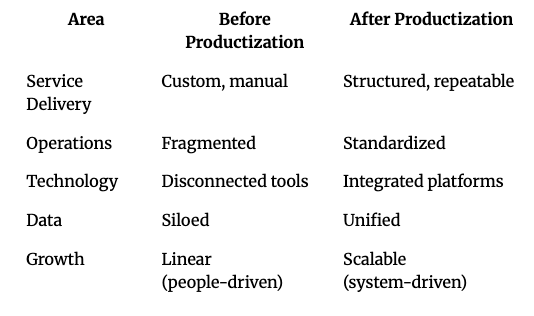

What Productization Actually Changes for Wealth Firms

Productization fundamentally reshapes how wealth firms operate across multiple dimensions:

Conclusion: Productization as the Foundation for Scalable Advice

Productization is often discussed as a strategic initiative, but its real impact is operational. It is the mechanism through which wealth firms translate their expertise into scalable, repeatable services.

Importantly, it does not reduce the quality or personalization of advice. Instead, it ensures that high-quality service can be delivered consistently across all clients.

The firms that will succeed in the coming years are not those with the most bespoke offerings, but those that can systematically deliver insight, consistency, and outcomes at scale.

In an increasingly complex and competitive environment, productization is no longer a differentiator. It is becoming the foundation for how modern wealth management firms operate.

Naaz Scheik is the founder of SoftPak Financial Systems and keynote speaker at RIA Edge LA.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All