Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Key Takeaways

- Managed accounts classified as qualified default investment alternatives (QDIAs) are not truly managed because there is no participant engagement.

- Personalized Target Date Accounts (PTDAs) combine managed accounts and target date funds, offering multiple glidepaths for self-directed participants to manage their own risk.

- For defaulted participants, customization — not personalization — is recommended, with plan sponsors designing a model glidepath tailored to plan demographics.

- Personalization works for non-defaulted, engaged participants, but pretending to personalize for defaulted accounts misleads and fails to address true risk tolerance.

When Is a Managed Account Not Managed? When It’s a QDIA

Although managed accounts (MAs) are the second most popular qualified default investment alternative (QDIA), with $450 billion in invested assets, they are far behind the $4 trillion invested in the most popular vehicle, target date funds (TDFs). However, a new hybrid product, Personalized Target Date Accounts (PTDA), combines the two approaches.

There are two distinct types of managed accounts. Both are called “managed accounts,” but one is not actually managed.

- Truly managed accounts require decisions from participants who typically take advice from live investment consultants. These accounts are not QDIAs because these participants do not default.

- By contrast, people relying on the default option do not engage, so managed accounts for them are not actually managed, despite the fact that they are labeled as such.

This article details personalization with a strong caution against trying to personalize what cannot be personalized because It’s Not Nice to Fool Mother Nature with a “managed” account that is not actually managed.

QDIAs Are Best Constructed as Custom Model PTDAs

Defaulted participants will not talk to investment managers, so we can’t know their risk preference/tolerance. That said, most MA and PTDA providers pretend to know by using recordkeeper data as a proxy — they use age and wealth without ever talking to the participant. This data reveals risk capacity, which is the ability to take risk, but the correct input is risk tolerance, which is the willingness to take risk.

Wealthy people with high risk capacity want to stay wealthy, so they actually have low risk tolerance. Similarly, poor people with low risk capacity want to stop being poor, so they tend to have high risk tolerance. Simply put, personalization for defaulted people does not work, and — even worse — it could do them real harm by confusing an investor’s risk ability with their risk tolerance.

MAs and PTDAs simply do not work for defaulted people. And calling them QDIAs does not change the fact that pretend personalization does not work. The better approach for all defaulted people is to customize rather than personalize. The plan sponsor, along with its advisors, tailors a model glidepath to serve all defaulted people, using the funds that are on the plan platform.

Yes, it’s still one-size-fits-all, but can be designed in a way that follows DOL guidance by aligning the QDIA with plan demographics. The one demographic trait that all defaulted people have in common is financial naiveté — and for that reason, they need protection.

Non-QDIAs Are Personalized

Non-defaulted participants do want to engage. They want to tell investment managers their risk tolerance. MAs and PTDAs work for self-directed people. About a third of the assets in TDFs is from self-directed individuals, confirming that many non-defaulted people like the construct of a lifetime glidepath. These investors can manage their own unique glidepath through time, changing risk level and target date at will.

Personalized Lifepath Management Using PTDAs

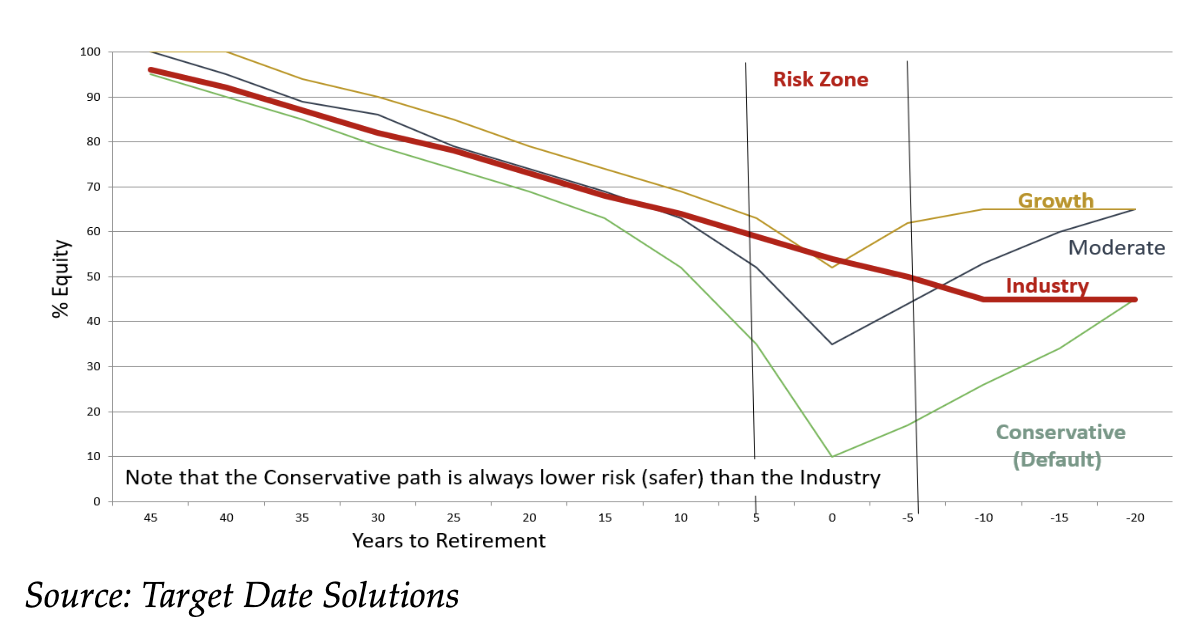

Unlike most target date funds with a single glidepath, PTDAs come with an array of glidepaths with varying risks, such as the examples shown in the following graphic.

Participants in PTDAs can move from path to path at any time, and they can blend paths. They also change their target date at any time. They manage their own unique lifetime paths over the long term, adjusting to life events as they occur.

The “Industry” shown in the graph above is an aggregate of the S&P Target Date Fund Indexes, covering all TDFs. It is 85% in risky assets at the target date with 50% in equities and 35% in long-term bonds. By contrast, the “Conservative” glidepath is 20% risky at the target date. It is like the glidepath followed by the Federal Thrift Savings (TSP) TDF, and others.

Conclusion: Baby Boomers and Fiduciaries Take Heed

Baby boomers are spending this decade in the “Retirement Risk Zone,” during which investment losses can ruin their remaining years. Accordingly, baby boomers need to take a close look at their investments to make sure that they are safe. Those who have not made an investment election in their retirement savings (i.e., defaulted) need to find out how they are invested, rectify their previous inaction, and move to safety.

Fiduciaries need to take heed too. The description “managed account” is not correct when applied to the accounts of defaulted participants, because you cannot manage assets for people you don’t know and who will not talk to you. However, that is what is happening. Truly managed accounts are being viewed as the same as unmanaged accounts, and that’s a mistake.

This matters because there is a push in retirement savings plans toward personalization, since investing is inherently personal. The idea behind this movement is solid, but current implementations are not. Personalization can help self-directed participants manage their own unique lifepaths, and it can be used to customize a single glidepath for all defaulted people as a QDIA. That said, it can’t manage defaulted accounts.

Ron Surz is president of Target Date Solutions, developer of the patented Safe Landing Glide Path and Soteria personalized target date accounts. He is also co-host of the Baby Boomer Investing Show. Surz’s passion is helping his fellow baby boomers at this critical time in their lives when they are relying on their lifetime savings to support a retirement with dignity, so he wrote a book, “Baby Boomer Investing in the Perilous 2020s,” and he provides a financial educational curriculum.

For anyone who relies on TDFs — or advises those who do — Surz’s new book is a must-read guide to understanding the risks, solutions, and future of a secure retirement.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

More Fiduciary Rules Topics >

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.