Riding the Wheel of Fortune: A Practical Guide to Lifetime Investing and Spending

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Overview

We steer our financial course through life, choosing how much to spend and how to invest what’s left, periodically updating our choices as circumstances evolve. This is the essence of financial planning: specifying in advance a desired spending and investment policy conditional on relevant aspects of our life, varying investment opportunities, and our preferences for the benefits derived from our wealth.

It’s a pretty simple problem to put into words, but finding an optimal solution has occupied some very bright minds since Harry Markowitz got the ball rolling 60 years ago. Since then, researchers have made tremendous progress in both specifying and solving increasingly realistic and relevant formulations of this problem. In fact, academic research in this area has been so rich that it’s given birth to an entire academic discipline with dedicated university courses and textbooks.

And yet, even though the study of this problem has delivered novel and valuable insights, we haven’t seen meaningful adoption by the financial planning or wealth management industries. The issue may in part involve the “expected utility” formulation so common in academia. Utility is a measure of the benefit we derive from using our wealth, and researchers generally presume that an investor knows their own “utility function,” which is to say the relationship between their wealth and utility.

Unfortunately, sparingly little has been written about how an individual should calibrate their personal utility function.1 Financial planners may also worry that these relatively stylized academic models of utility don’t adequately represent investor preferences in the real world and fear their clients will be confused by a process grounded in an unfamiliar and abstract formalism.

As a result, practitioners have mostly focused on ad-hoc solutions that are often neither satisfying in their methodology nor especially helpful to their users. Catchphrases like “goal-based investing” have proliferated, but if the ideas behind the catchphrases are taken seriously, they typically lead to obviously suboptimal or nonsensical policies. [MB, pp.141 – 145] Sometimes these approaches can use complex simulations and model complicated financial situations with impressive detail — but without a grounding in a principled framework, the computational sophistication is often wasted.

In contrast, we’ve found the framework suggested by decades of academic research to also be eminently usable in practice. Our experience is that, with a little guidance and explanation, most of our clients can reasonably calibrate their own utility function, which does quite a good job of representing their risk preferences — at least as far as material financial matters are concerned.2 And similarly, most of our clients can both appreciate and benefit from a sound framework that provides advice for translating preferences into consistent investing and spending policies.

In this note, we’re primarily focused on the questions of how much you should spend and how much of your wealth you should commit to risky investments. These are two of the most basic and impactful financial questions to answer, the building blocks of any sensible personal financial policy. We’re not going to drill down into subsidiary questions like “what should I spend money on?” and “what risky investments should I choose?” We feel the former mostly lies outside the realm of mainstream finance. Oceans of ink have been spilled on the latter, but at Elm, we feel that broad, global equity markets — typically held through liquid, low-cost index funds — will serve most investors best.

The framework we use and discuss below is almost entirely grounded in the academic consensus for how to answer these big-picture questions — so we’re standing on the shoulders of the giants of financial economics,3 and doing our best to take the concepts they developed and turn them into practically useful tools accessible to an audience of primarily wealthy, sophisticated investors. For a deeper dive into the history and philosophy behind what we’re doing here, we (naturally!) recommend our book The Missing Billionaires, in particular Chapters 9 through 11. Throughout, as we discuss various concepts we’ll reference where in the book more information can be found — for example [MB, Ch. 9 – 11]. We also have a significantly more technical whitepaper which can be found here.

What’s the Goal?

Before we can find the ideal set of investing and spending policies, we need to know what our objective is. We think the clear choice is to maximize the “Lifetime Discounted Expected Utility of Spending” [MB, Ch.9] — which, going forward, we’ll just called Expected Lifetime Utility. There’s a lot of terms there, so we’ll try to unpack them one by one:

- Lifetime: We’re not focusing on a fixed horizon, such as the next ten years, but looking at spending and investing over one’s entire lifespan starting now.

- Expected Utility:4 Utility refers to the benefit we get from spending, and it’s not a straight-line relationship: having to cut spending by half hurts much more than doubling spending feels good. The magnitude of this asymmetry is a personal preference and varies between people, and we’ll call it your coefficient of risk aversion.5 Using Expected Utility of Spending rather than simply Expected Spending makes sure we capture your risk aversion and take both spending amount and spending risk into account. [MB, Ch. 6]

- Discounted: We’re potentially adding up the utility of spending from periods that could be 50 years apart, so there are two things we need to adjust for to make these utilities comparable. The first is time preference, which basically encodes your preference for how to trade off an equal amount of utility today vs. next year. The second is longevity: we can’t know how long anyone’s life will last, and this risk — what we’ll call longevity risk — needs to be incorporated into our decision framework. If you’re 50 right now, you’re much more likely to be alive at 60 than at 100, so we need to adjust the utility of spending by these probabilities.6

- Spending: We’re using spending pretty generally here, to encompass at least three different uses of wealth:

-

- Spending on yourself: Normal spending like paying the bills, dining, vacations, etc.

- Living philanthropy: We treat philanthropic giving during your life as just another kind of spending, without making any distinction between it and spending on yourself.

- Bequests: This is what happens to the wealth you leave behind, whether it goes to your heirs, philanthropies, or some combination of the two.

The type of spending we care about is what economists call real spending, meaning we’re deriving utility not from the absolute number of dollars we’re spending but from how much it can buy. If we’re spending twice as much in a world where everything’s twice as expensive, that’s no benefit to us! So as spending changes over time, we need to keep track of how much of that is a change in real spending vs. just a change in nominal spending from inflation. In the framework, we actually keep track of two inflation metrics: inflation in the consumer-price index (CPI), and inflation in cost-of-living, which is typically higher than CPI. We use the cost-of-living inflation to translate nominal spending (and wealth) into real spending and wealth.

One thing that isn’t spending is paying taxes — a regrettable necessity, but not one that brings (most of) us utility. When we model your wealth dynamics, we’ll have to include taxes, of course — on income, dividends, and capital gains — and take them out of wealth, but it won’t be counted as spending.

How to Achieve the Goal

If you live forever and pay no taxes,7 we know exactly what to do! Robert Merton showed that there’s a simple set of policies which, in this case, maximize your Expected Lifetime Utility:

- Invest a constant fraction of your wealth in risky assets, equal to the “Merton Share”. [MB, Ch. 4]

- Set your spending to a constant fraction of your wealth — the level itself will depend on your risk aversion and time preference, but it will be a bit less than the risk-adjusted return on your portfolio.

Sadly, living forever and paying no taxes is not a good assumption for most of us. But we can take inspiration from the Merton problem setup and solution, with a few extra wrinkles we need to introduce.

- We’ll assume that the optimal amount to invest in risky assets — what we’ll call the investment policy, isn’t just constant, but can change as a function of wealth. Implicitly, the optimal investment policy will also change with age and time, because wealth is changing with age and time.

- We’ll assume that the optimal spending policy is proportional to wealth, but that the optimal spending rate can change over time.

Then, we just need to find the investment policy and spending policy which jointly maximize your Expected Lifetime Utility.8 In this more realistic case, there isn’t a formula for Expected Lifetime Utility given a specific set of policies, so we have to use some computer power to calculate it numerically.

Nuts & Bolts

We start off by making assumptions about:

- Safe asset returns.

- The expected risk and return of your risky portfolio — typically global equities, but this can be customized to your specific circumstances as well.

-

- We can also include an annuity component in your portfolio and evaluate the effect of the annuity on your lifetime spending metrics.

- Your longevity statistics, either just for you or jointly with your spouse.

- Tax rates and rules.

- And with input from you:

-

- Your net worth, and its distribution across your taxable, traditional IRA, Roth IRA, and personal real-estate buckets.

- Your future earned income, including how much uncertainty there is around it, and your social security income.

- Your level of risk aversion, which we help you calibrate.

- The weight you place on utility arising from personal spending vs. from legacy bequests.

- Your “subsistence spending”, a level of spending which you would very, very strongly prefer not to fall below.

We’ll assume that every year, you have two choices to make:

- What fraction of your investable wealth to invest in the risky portfolio?

- What fraction of your wealth to spend on consumption.9

And we’ll assume that these policies can’t just be anything from year to year, but they have to vary pretty smoothly and follow some basic functional forms.

We’ll computationally model your portfolio and spending dynamics, then start with an educated “guess” at a good set of policies and calculate your Expected Lifetime Utility based on these policies and the modeled dynamics. We then use an optimizer to find better and better policies, until we can’t increase Expected Lifetime Utility any further by varying the policy details, at which point we’ll have found your optimal investing and spending policies.

Output

The output of the process can be summarized through four main charts, which we’ll discuss below.

These are just illustrative examples, not generic recommendations — actual output will, of course, be different for each individual case.

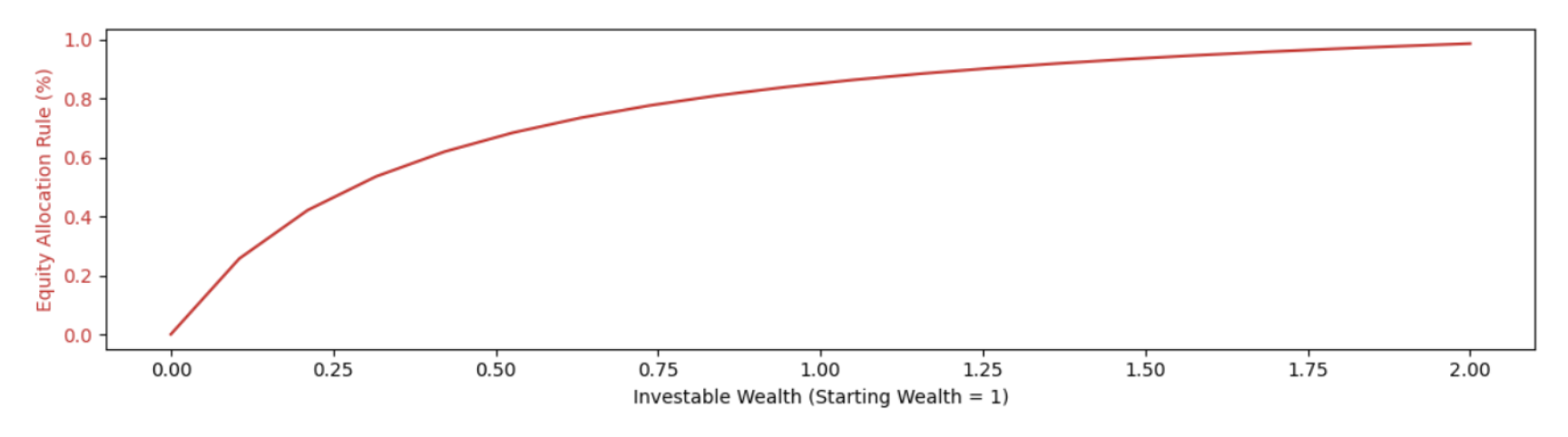

The first chart displays the investing rule: the optimal fraction of wealth to allocate to the risky portfolio, which is a function of wealth level:

This is saying that, for our example investor around their current wealth level, it’s optimal to commit about 80% to the risky portfolio. This rises to 100% as wealth rises, and the spending this investor’s wealth can support increases relative to subsistence. Conversely, it falls to 0% as wealth approaches zero.

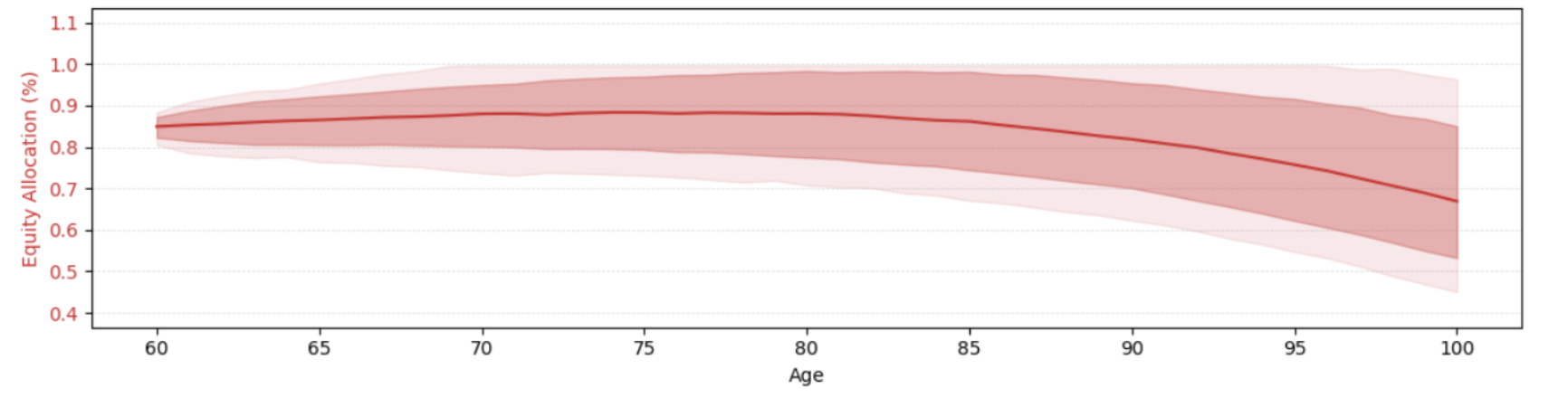

The second chart displays statistical properties of the investing rule:

The solid line shows the median value over time. The darker “cloud” around it shows the 1 standard-deviation range around the median, and the lighter cloud the 2 standard-deviation range. There’s about a 16% chance of being below the lower 1 standard-deviation boundary, and about a 2% chance of being below the 2 standard-deviation boundary.

In this case, the range of optimal equity allocations is quite tight near the beginning (because there hasn’t been time for wealth to vary much), then widens out significantly into very old age.

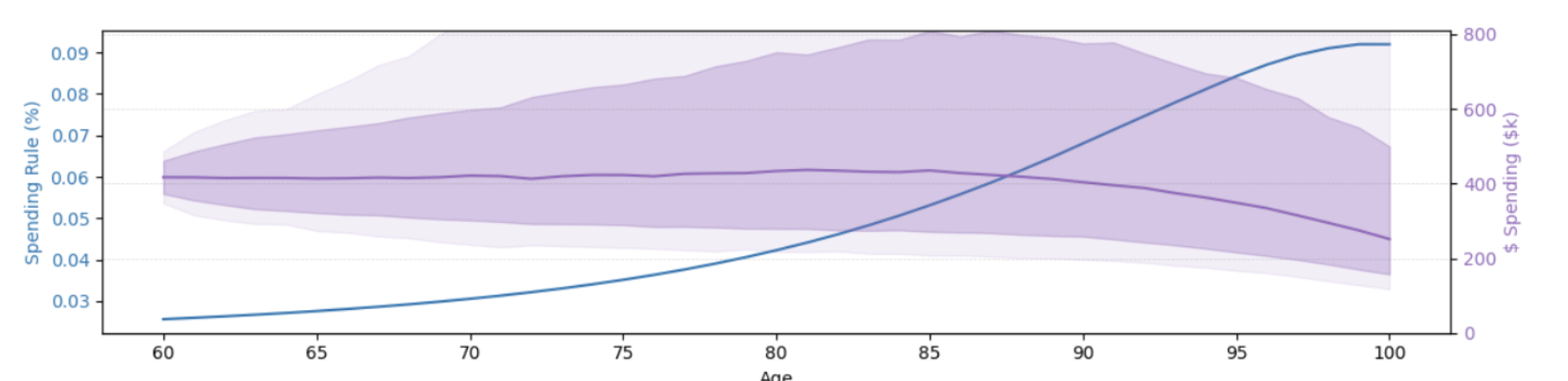

The third chart displays the spending rule:

The blue line shows the optimal proportion of wealth to spend every year — in this case, starting around 2% and rising to about 10% in very old age.

The solid purple line shows the resulting median spending from following the optimal investing and spending rules. It’s in real dollars, adjusted for both inflation and cost-of-living increases. As above, the clouds show the 1-standard-deviation and 2-standard-deviation ranges.

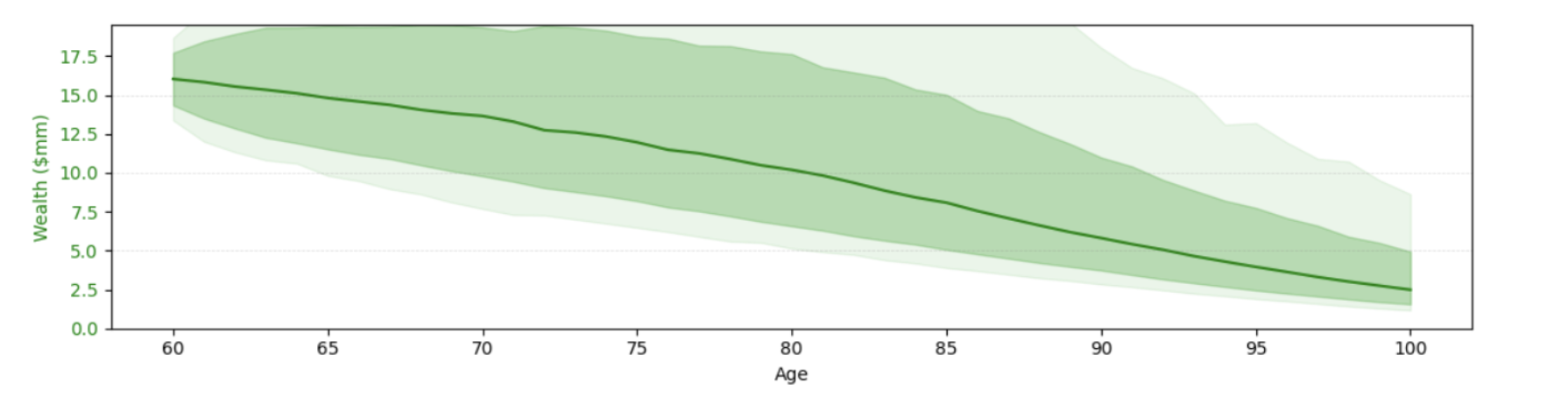

The final chart shows the evolution of real wealth,10 again assuming following the optimal investing and spending rules:

As above, the solid green line is the median, and the clouds are the 1 and 2 standard deviation ranges.

Elm Lifetime Investing & Spending Analysis (ELISA)

We have a prescriptive process we can go through with clients, with this framework and the associated internally developed models at its center. The focus of the process is to help you figure out, at a high level, your optimal investing and spending policies — in particular, how much investment risk to take, and what proportional spending policy to follow. Related questions we can address through the process include:

- Is current spending sensible?

- How much expected spending and bequest your wealth can support, and what the distribution of outcomes looks like

- Are your savings sufficient for retirement given your spending and bequest preferences?

- What is the impact of different income scenarios on long-term spending and bequest?

This is not a typical financial planning process, which ordinarily focuses on helping families track and budget spending in a detailed way. Our focus instead is not on the fine-grained details of your portfolio or spending, but on the big-picture investing and spending policies you should be following. There are cases where more detailed modeling can be useful too, but we think focusing on these policies is the best and most impactful place to start for most families.

Endnotes

1 Ourselves being the exception that proves the rule!

2 We’re really only concerned with significant financial decisions, not with reflecting risk preferences across the full spectrum of life decisions.

3 Especially Robert Merton, framer of the “Merton Portfolio Problem” which forms the kernel of our framework, but many others as well who contributed to the field of financial decision-making under uncertainty.

4 You probably thought we’d do Discounted next, but you have to wait for it!

5 We assume Constant Relative Risk Aversion (CRRA) utility throughout.

6 We use standard actuarial tables to make these longevity calculations.

7 Amongst some other simplifying assumptions, for example: no subsistence spending, CRRA utility, normally distributed returns, etc.

8 We actually assume both policies are parametric and optimize over the parameters.

9 i.e. not including taxes and other forms of “forced” spending and not including investments.

10 Adjusted using the cost-of-living index.

This is not an offer or solicitation to invest, nor are we tax experts and nothing herein should be construed as tax advice. Past returns are not indicative of future performance.

Victor Haghani is founder & CIO of Elm Wealth, a Philadelphia-based asset manager. James White is Elm Wealth’s CEO.

Learn more at www.elmwealth.com.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All