Seduced by Private Markets: Why Democratization May Not Be Best for Investors

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

The push to “democratize” private markets is not about giving retail investors better opportunities; it is a corporate strategy by asset managers to bypass the race to zero in public markets and recover profit margins. This is a fundamental mismatch, attempting to force illiquid, opaque, and hard-to-value assets into a public fund structure built for liquidity and transparency, ultimately shifting new and significant risks onto the individual investor.

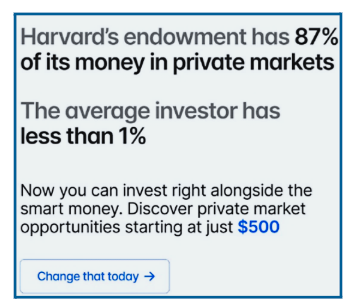

Harvard’s endowment has 87% of its money in private markets … says the advertisement (for private markets).

Not quite. At the end of 2024 it was 79% — a combination of hedge funds, real estate, real assets, and private equity.

You get the point: Private good, public bad. Just click here.

Those smart college-types can’t be wrong, can they?

Well, Moody’s says they’re wrong.

Wrapping private markets for retail clients will introduce new risks to private-asset managers, including “reputation loss, heightened regulatory scrutiny and higher costs,” according to the ratings agency. Plus, there could be additional risks to investors, from the same MSN.com article noting, “[d]uring economic downturns, individuals typically sell their investments and stockpile cash to make ends meet. That will be harder to do if those investors hold stakes in private funds that limit withdrawals.”

Not so, says the world’s largest asset manager.

BlackRock announced plans to weave private equity into its target date funds. It estimates private equity and venture capital will grow by more than two-thirds by 2029, to $23 trillion. Besides, says BlackRock, defined benefit plans “have invested in privates for years.”

BlackRock continues, “In fact, we believe it’s possible to design an investment solution … that could deliver an estimated incremental 50bp in average annual returns over an employee’s working lifetime. Compounded over 40 years, this could generate about 15% more money in a participant’s 401(k) account.” Later, in an 8-point font footnote, it discloses: 1) its estimate comes from “capital market assumptions”; 2) are not actual returns; 3) “nor do they consider the impact of trading decisions, liquidity constraints, fees, taxes and other factors on future returns.”

Is this a serious argument for private markets? Is lack of access to private markets holding back retail investors?

I am a retail advisor and an investment writer, and I have built and managed public funds. Therefore, I see this from multiple angles. But the only angle that matters is that of the retail investor.

Let’s evaluate private markets based on liquidity, returns, transparency, and measurement standards.

Liquidity: Why Illiquid Assets Stay Illiquid in Public Wrappers

I don’t know who needs to hear this, besides the DOL, BlackRock, and the president (upon his Executive Order signed August 7), but putting an illiquid asset in a liquid fund structure such as a mutual fund or ETF does not make it liquid.

The founder of Advisor Perspectives (predecessor to VettaFi Advisor Perspectives) Robert Huebscher reported on a webcast earlier this year that featured Jeffrey Gundlach. ”While private credit has performed admirably over certain periods in the past five years, it is no longer demonstrating outperformance. It is an illiquid asset class put into a daily NAV fund, and there is a mismatch in liquidity,” Huebscher noted.

“That is something to always avoid,” Gundlach said during the webcast.

Additionally, Gundlach recently said, “Private credit today is analogous to the CDO market in the mid-part of the ’00s, where there’s just tremendous issuance, there’s tremendous acceptance … There is a lot of overinvestments in private credit and the liquidity is not very good.”

My experience with illiquid assets is visceral. I managed a variable annuity subaccount for over 10 years on three large insurance platforms. I never liked following the interval fund manager, who was in the same trust at annual board meetings. Their meetings took forever, always due to pushback on valuations. “Where’d this price come from?; how’d you value that?; who’d you say the appraiser was? You? You can’t do that!” Finally, the fund was shuttered because of pricing complications.

Meanwhile, my fund offered real-time liquidity, held tier-one securities, came with one-day settlement, and was independently verified by exchanges and major data feeds. I never needed to provide values. Our meetings lasted five minutes. That is the beauty of the public securities markets.

Is the industry willfully ignoring this difference between public and private?

Returns: The Private versus Public Reality Gap

Does private outperform public?

Institutional portfolio manager Cambridge Associates says yes: “Returns for the US private equity (PE) index exceeded those of the S&P 500 for periods longer than three years as of December 31, 2024, and outpaced the small-cap index, the Russell 2000®, in all but two time periods analyzed. The US venture capital (VC) benchmark’s performance relative to public indexes has been less consistent, particularly against the tech-heavy Nasdaq.” (Source: US PE/ VC BENCHMARK COMMENTARY, Calendar 2024)

However, these returns were not achieved inside a public-funds structure available to retail investors, such as ETFs, mutual funds, closed-end funds, variable annuity subaccounts, UITs, etc. In this regard, no actual comparison has been made. Once you make public funds of private markets, you dramatically change their structure.

There are few private market ETFs — by my count less than a dozen. The four funds that appear on my Morningstar database that have a track record of over three years underperformed their respective index categories. (Data is available on request.) I may get pushback because I picked the peer — not the fund manager. That’s fair, but remember I am driven on behalf of investors, not the industry.

I am not saying these funds should not be built. I can build a case for making available investment categories that are not easily purchased or custodied. I am saying issuers should quit trying to build the raw performance case. That is not how to win skeptics.

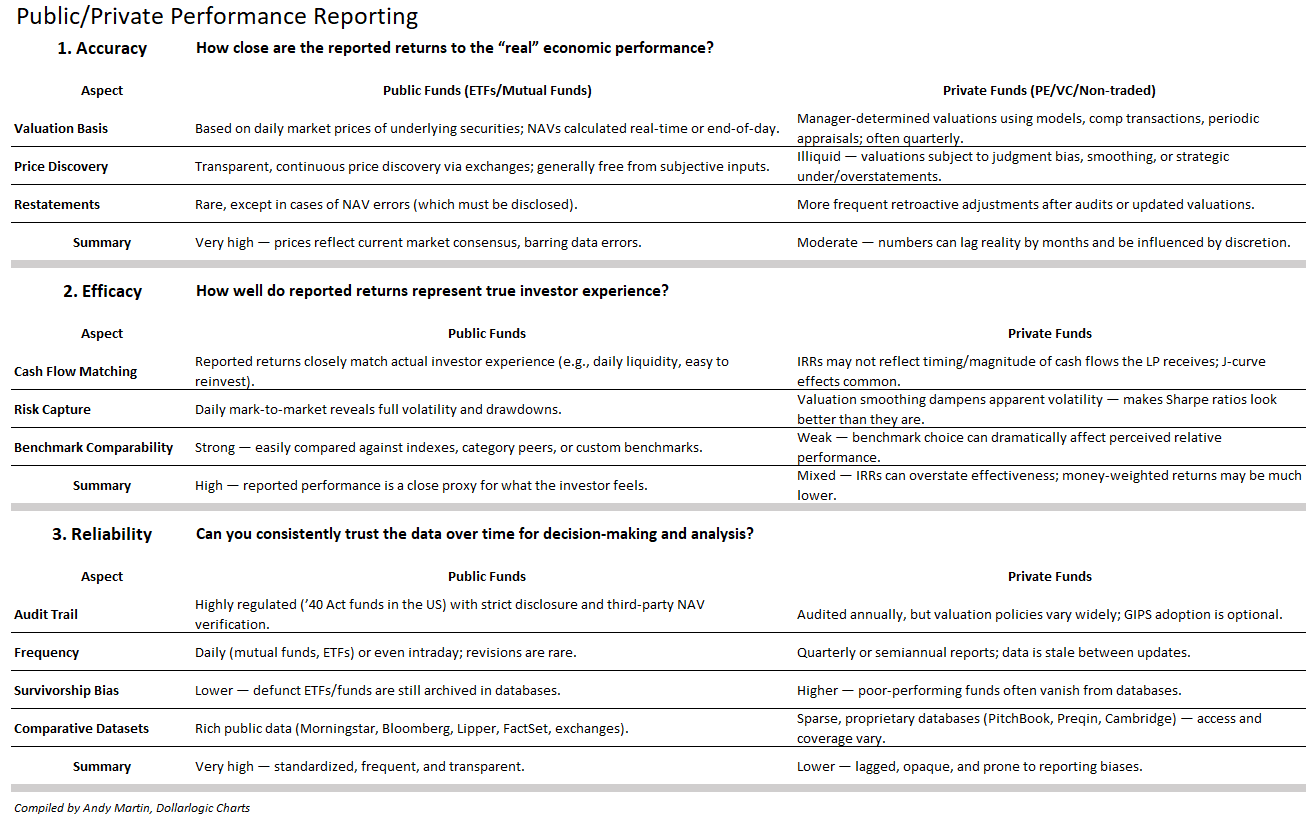

Transparency: Trust & Verification in Public versus Private Markets

Is it easier to verify the returns of publicly traded securities or private nontraded instruments? You know the answer. However, to attempt a detailed response using accuracy, efficacy, and reliability criteria as guides, consider the following comparison chart.

The Public/Private Performance Reporting table breaks down how public and private fund performance reporting compares on three dimensions — accuracy, efficacy, and reliability — giving you a clearer view of where each excels or falls short.

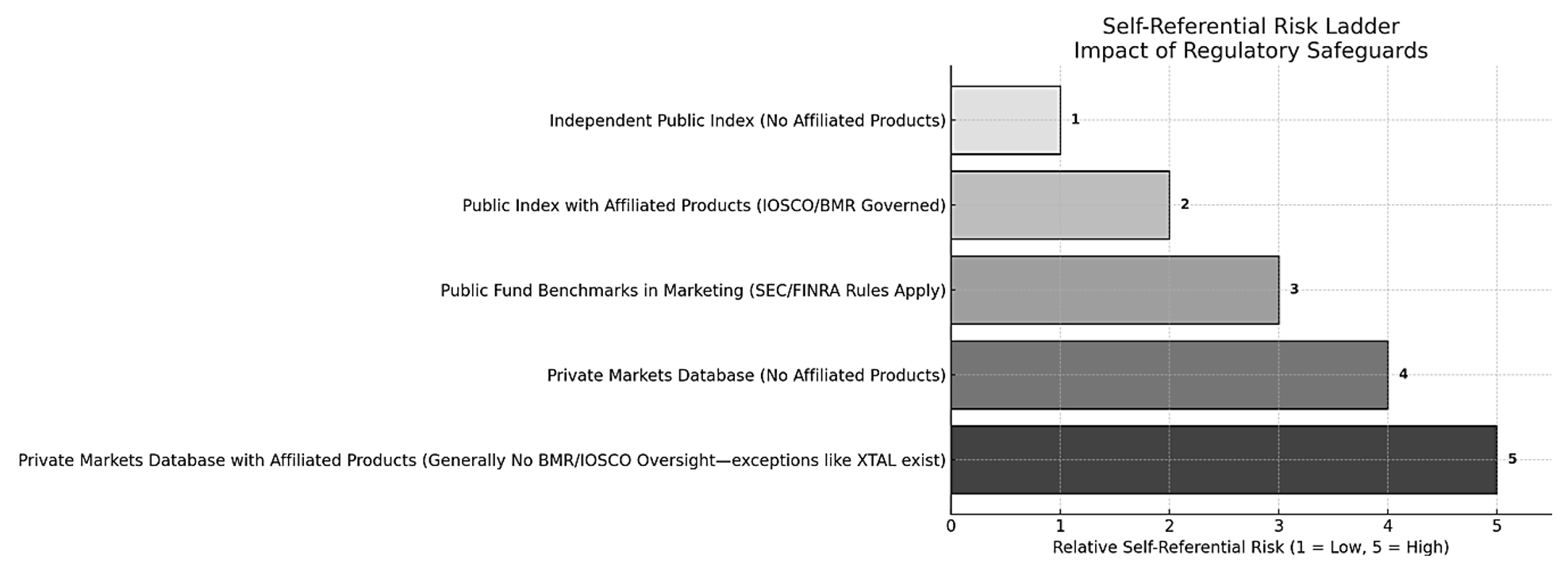

The Big 3 private markets performance data providers are BlackRock-owned Preqin, Cambridge, and Morningstar-owned Pitchbook (Morningstar has advisory products but less direct general partner roles than Cambridge and BlackRock). All three have inherent conflicts of interest in reporting performance — called self-referential reporting — where the same entity (or its affiliate) is both producing the performance standard or dataset and participating in the market being measured, so that its own products, services, and track record are judged against a benchmark or dataset it controls.

Is this best practice?

To compare, the Self-Referential Risk Ladder, a generalized 1–5 scale, highlights the relative conflict-risk of various index and data provider structures. As you move from public, independent benchmarks to private, affiliated data sources, the need for strong governance safeguards increases.

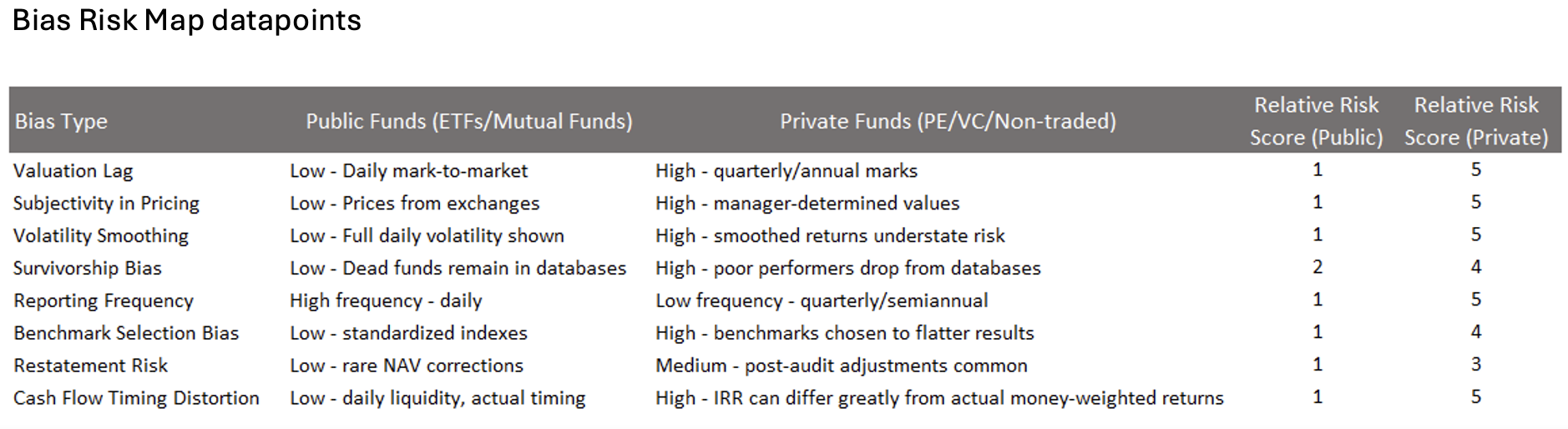

Measurement Standards: When Methodology Shapes the Story

Jason Millard, CFA, CIPM, managing member, Assurance Accounting Group LLC in San Diego told me that measuring long/short hedge funds (as a private markets example) provides relatively accurate data. But private equity?

“Not so much, particularly with valuation and timing, where the methodology is inconsistent. There can be a lot of reporting drag — one fund may be valued end-of-year, the other end-of-quarter. Also, the value and frequency of fees? How are fees accessed — as paid [or] accruing? Cash or accrual will make the returns look very different. This can create distortions.”

This is an embedded problem, the nature of private investments. It’s not wrong, it’s not illegal. However, it also does not meet the standard of public fund reporting. There is a material gap between public and private fund performance reporting.

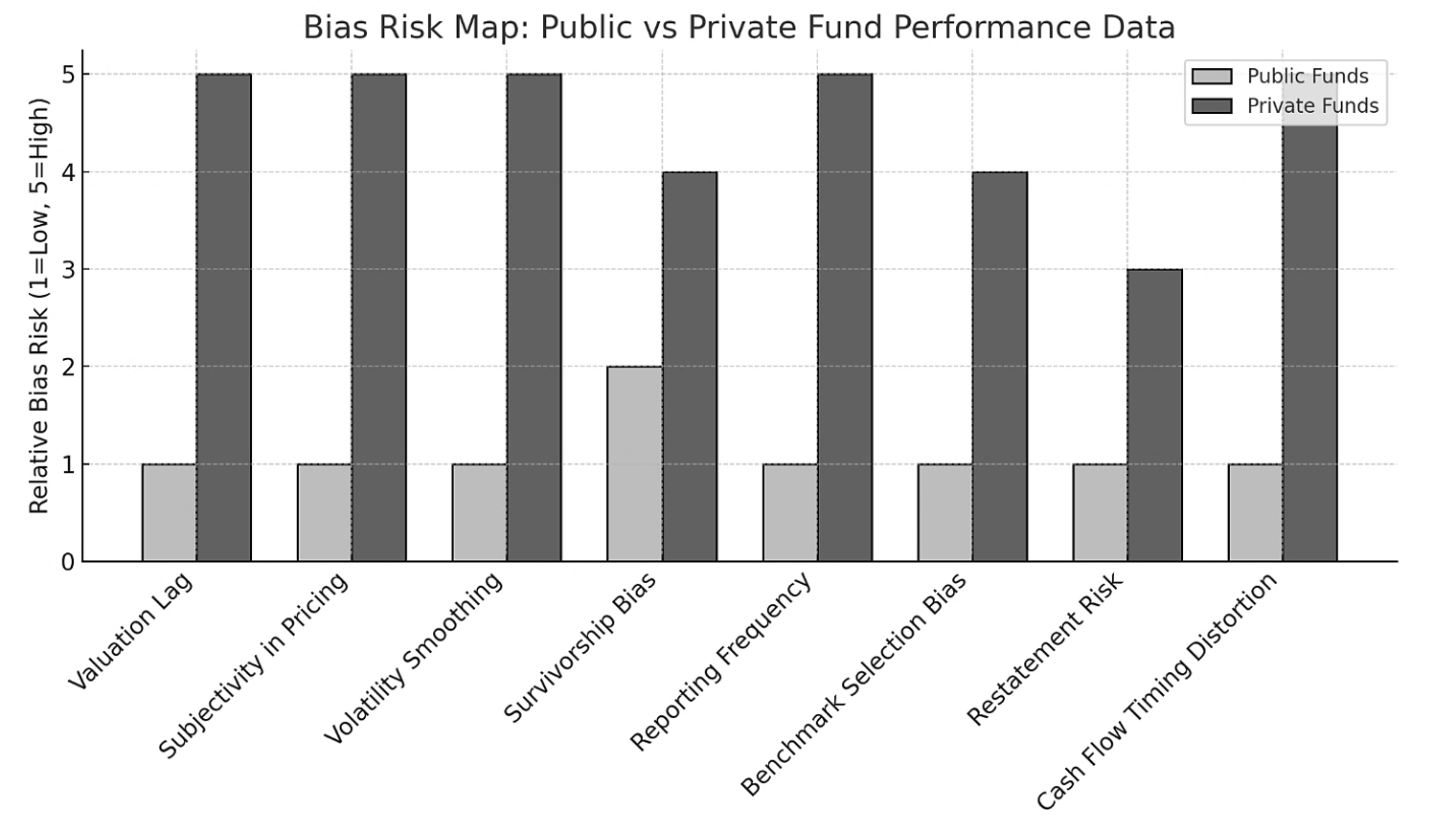

A straightforward way to illustrate this is The Bias Risk Map below, which contrasts eight key areas where public and private fund performance data can differ in accuracy and reliability. Each is on a 1–5 scale, where higher values indicate greater potential for bias or uncertainty.

Cynical Me

BlackRock won the game, accumulating more assets than their competitors. They pushed expense ratios down to zero, turned around and saw vast work products, employees, fixed costs, and real estate living on three bps. Now they need their margins back. This seems to be a way to vivify balance sheets.

Am I wrong?

BlackRock makes $25 million more top-line revenue on the iShares Bitcoin Trust ETF (IBIT), (issued just last year) than on their biggest ETF, the iShares Core S&P 500 ETF (IVV) (that launched 25 years ago). Higher ER funds must be the future for a company that has exhausted itself by “democratizing” investing.

Democratizing has taken on a new meaning for BlackRock: Reimbursement.

How? By seeking that reimbursement from expanded offerings into active management, digital assets, and — most recently — with private markets.

It’s hard to blame BlackRock. IBIT is up 120% (as of 9/5/25*) since launch. I am sure their shareholders are thankful and feel the 25 bps is well worth it. I do not begrudge their success.

However, it is important to understand the complications.

Can This Work?

I am a fan of private markets. Surprised? The best investment I’ve made was private market: an office building, which resulted in a 3x cash-on-cash return in six years. But it was expensive, illiquid, price volatile, hard to maintain, complex, deeded, and taxed everywhere. That’s the tradeoff that accompanies investing in private market assets.

However, it must be done correctly on both the fund and the investor levels.

Fund level: BondBloxx and Virtus have issued new private credit CLO ETFs. Private credit bonds have relationship-based structures and are loan-like, less liquid, and more complex than typical traded or even non-traded bonds. In exchange, they may offer higher returns and may be collateralized.

It is nearly impossible for the average investor to buy even one of these, and they often need to be an accredited investor. However, in a fund, they are traded, valued, accessible and liquid (on the fund level, if not on the constituent level.)

Thinking like BondBloxx or Virtus is how bitcoin made it into ETFs. You would have to be a bigger scold than me to lament the availability of digital assets in publicly traded funds.

After all my criticism of private markets in funds, BlackRock’s idea, mentioned above, to add this asset type to target date funds may not be unreasonable. Target date funds have long hold periods, are hyper-managed, and are probably the most practical fund type to accept illiquid assets into — they have pension funds’ style of liability time matching.

Investor level. This is where it gets tricky. If you divide investors into Emerging, Mass Affluent, and High Net Worth, it becomes clearer where private markets belong, and where they do not:

High Net Worth? Yes

Mass Affluent? Maybe

Emerging? No

And this is how the story ends. When you take private markets and house them in self-directed accounts, it’s over. There is no way to keep the 22-year-old exterminator from putting 100% of his Terminix 401k plan into the new Quantum Computing V/C ETF.

You cannot say no to emerging investors. You cannot run suitability on mass affluents, and your HNWs are insulted that any shmoe off the street can have what they have.

As an advisor, that kind of hurts.

Chart sources:

Public vs Private Performance Reporting: Kaplan & Schoar (2005); Getmansky, Lo & Makarov (2004); CFA Institute (2020); SEC Investment Company Act of 1940 & ICI Guidelines (2020).

Self-Referential Risk Ladder: IOSCO (2013); EU Benchmarks Regulation (2016+); FINRA Rule 2210; SEC Marketing Rule (2020); Preqin, PitchBook, Cambridge Associates company disclosures.

Bias Risk Map: Gompers, Kaplan & Mukharlyamov (2016); Brown et al. (1992); Phalippou & Gottschalg (2009); Preqin (2023); Kaplan & Schoar (2005).

Source disclaimer: Elements of the analysis and visualization in this article were developed with the assistance of OpenAI’s ChatGPT (GPT-5). Source references, provided by AI are cited as originally generated.

*Past performance no guarantee of future returns.

Andy Martin is an advisor, writer, researcher, and index builder. He can be found at Dollarlogic.com and EWIndexes.com. None of this should be construed as investment advice.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits