Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Barbara, invested in a bond ladder, wanted to confirm when her next check would be issued. Jason, who owns a bond fund, wanted to sell his shares before lunch.

Different clients may prefer different ways to invest in bonds. This article isn’t about identifying which fixed income vehicle offers the highest yield or lowest fee. It’s about matching strategies to real-world investor behavior. Because if fixed income ideally adds a measure of calm to a portfolio, the position should be built to withstand human nature.

Bonds may not be as exciting as the latest internet meme or tech darling. However, if you’re a financial professional attempting to guide a client through a period of volatility, you know the importance of peace of mind. This article is for you. This is for the advisor reading this between back-to-back calls, wondering if there’s a better way to explain the trade-offs. You’re not alone.

Let’s meet three fictional clients, each with different goals, personalities, and preferences. We will explore how bond ladders, funds, and separately managed accounts (SMAs) meet their varying needs.

Meet the Clients

-

Barbara wants checks in the mailbox, not surprises in her portfolio.

-

Jason is juggling kids and deadlines, and has zero bandwidth for yield curves.

-

Rita desires custom solutions and hires a professional to build the blueprint.

Client #1: Barbara, the Planner → Bond Ladder

Barbara is 68 and recently retired, and wants a predictable monthly income.

Her advisor builds a bond ladder — a portfolio of individual bonds maturing at regular intervals. Barbara wants to know when her money will come back. It’s like rent checks from the world’s least exciting tenant.

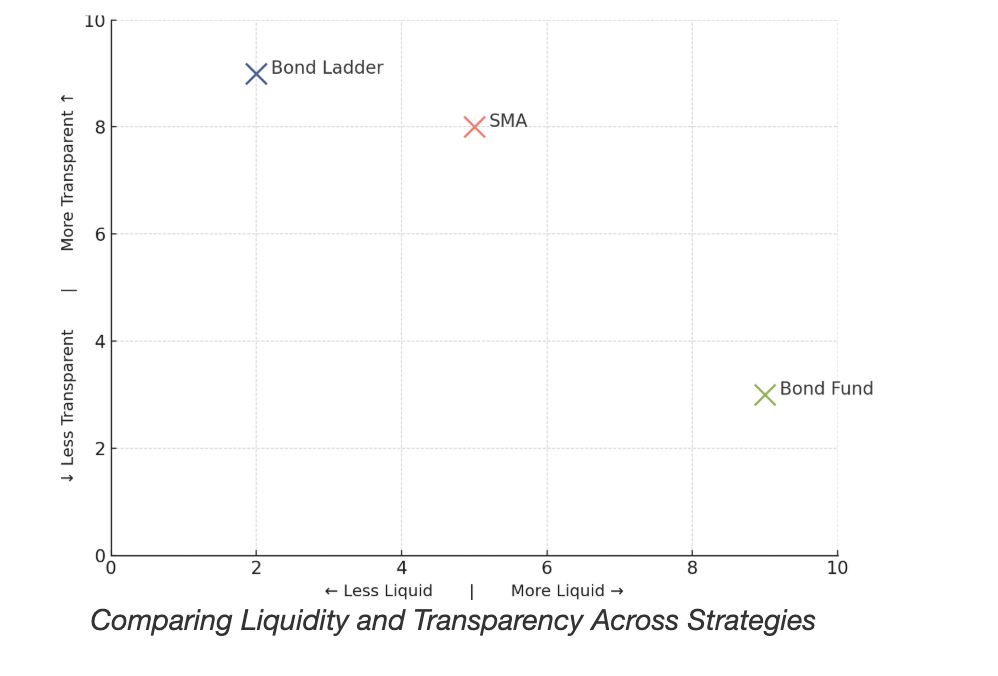

Why it works: Predictable income, full return of principal if held to maturity, transparency, and control.

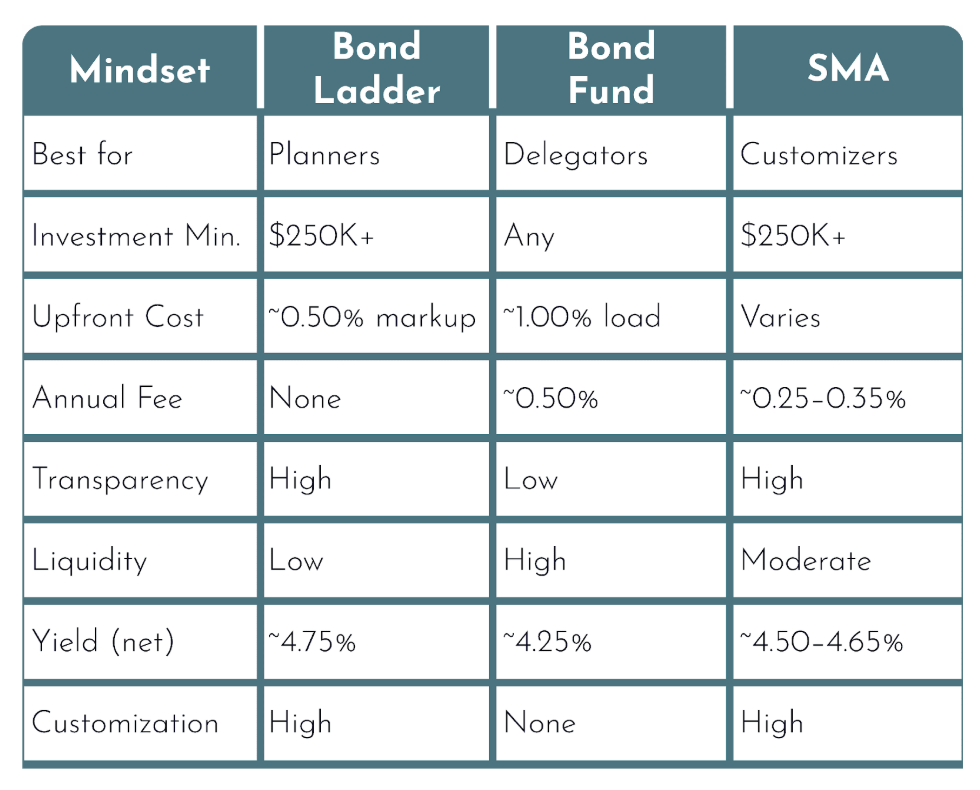

Costs: ~0.50% markup at execution (our assumed cost), no ongoing fee, low liquidity, and minimal customization.

Ideal for: Clients who prefer that their money works quietly in the background without surprises or drama.

It’s like a vegetable garden. You plant, you water, and you wait.

Client #2: Jason, the Delegator → Bond Fund

Jason is 45, busy with career and kids, and allergic to spreadsheets. He wants bond exposure without thinking about it.

His advisor recommends a bond fund or ETF. It’s easy to implement, instantly diversified, and rebalanced automatically.

Why it works: Simple and scalable, offers daily liquidity, and requires low effort.

Costs: ~Ongoing expense ratio (~0.50%). NAV fluctuates with market conditions.

Ideal for: Clients who consider fixed income as a background player, for diversification, not income.

Bond funds are the slow cookers of investing: set it, forget it … and maybe check the recipe once in a while.

Client #3: Rita, the Customizer → Fixed Income SMA

Rita is 60, has substantial assets, and wants things tailored to her tax situation and goals — but doesn’t want to manage the details herself.

Her advisor sets her up with an SMA, a professionally managed and customized bond portfolio. Rita obtains visibility into each bond, along with professional oversight.

Why it works: Combines transparency and customization with professional execution. It can optimize for tax, duration, and credit quality. Yield typically falls between ladders and funds.

Costs: ~Annual fee (~0.25-0.35%), lower execution costs than retail, and higher minimums (~$250K+)

Ideal for: Clients who want a tailored strategy without the DIY workload.

Sometimes you build the car. Sometimes you let a manager drive. An SMA gives you both — if you can afford the garage.

A Word About SMAs vs. Funds

We’re noticing a growing interest in SMAs — and for good reason. Advisors are realizing that if a client owns bonds inside a fund, that doesn’t necessarily mean they understand the holdings.

With an SMA, clients can see the bonds’ maturity dates, coupon payments, and yield to maturity. That clarity often translates into calm.

When rates jumped, my ladder and SMA clients stayed calm. The fund-only clients? Not so much.

How to Trade Bonds Like a Pro

-

Know your market. Inventory varies — don’t assume everything’s listed like a stock.

-

Shop around. Ask multiple dealers for pricing. Execution can differ.

-

Don’t chase yield. If it looks too good, it might just be too … callable.

FIR’s Philosophy: What Are You Really Solving For?

- Bond ladders and SMAs are designed for predictable income and capital preservation.

- Bond funds are for diversification and negative correlation to equities.

Trying to evaluate these structures exclusively on the basis of return misses the point. Each fits a distinct role in the portfolio — and a distinct kind of client mindset.

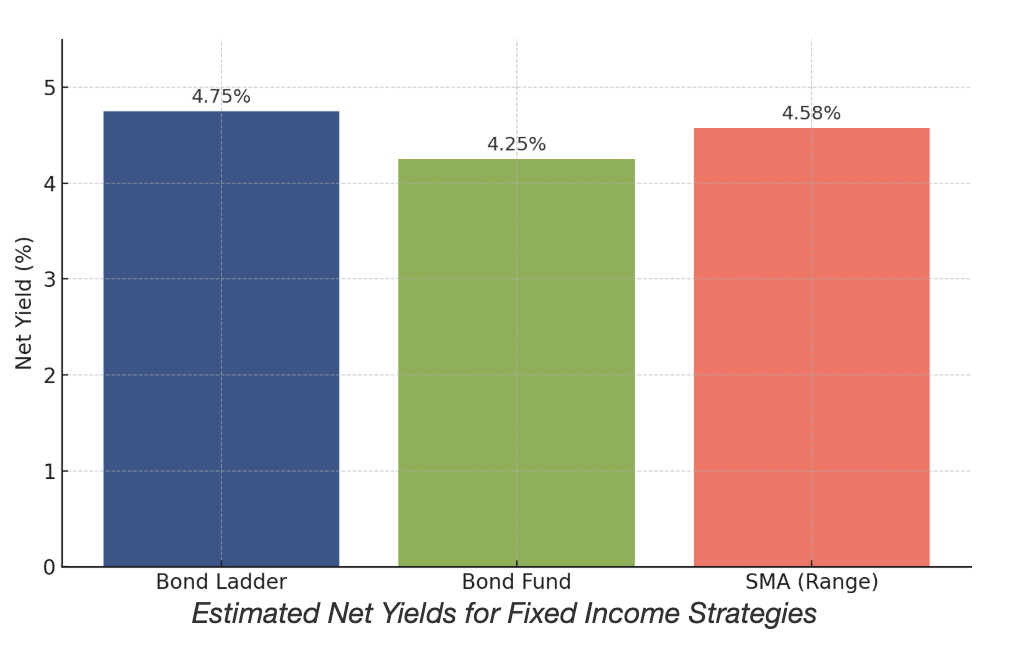

How We Calculated the Yields

To keep things apples-to-apples, we assumed the following when estimating net yields:

Bond ladder: Gross yield of 5.25% with ~0.50% in execution costs (markup at purchase), netting ~4.75%.

Bond fund: Gross yield of 4.75% with a 0.50% annual expense ratio.

SMA: Institutional pricing leads to lower execution costs (~0.15%), plus an annual fee of 0.25-0.35%, netting ~4.50%-4.65%.

Of course, actual results vary, but these are representative of current market conditions and typical fees. More importantly, yield alone isn’t the whole story.

Match the Strategy to the Mindset

Final Thought: It’s About Fit, Not Flash

Sometimes the answer is a ladder, sometimes it’s a fund, and sometimes it’s handing the keys to a seasoned manager. Just remember to inform your client about who’s driving — and what kind of ride to expect.

Charles Urquhart is the founder of Fixed Income Resources.

Prepare your bond portfolio for changing market conditions. Register today for the Fixed Income Symposium on Sept. 18, 2025, 11AM ET / 8AM PT.

Read more articles by Charles Urquhart

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.