TrumpBessenomics: The First-Semester Report Card

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Reintroducing “TrumpBessenomics”

Now that we are six months into the second Trump administration, it is worth revisiting the economic philosophy that I refer to as “TrumpBessenomics.” The term captures the fusion of Donald Trump’s populist, growth-oriented agenda with the strategic and data-driven approach of Treasury Secretary Scott Bessent.

At the heart of TrumpBessenomics is the 3-3-3 Plan, a simple but ambitious economic vision:

- Achieve 3% annual GDP growth through deregulation, increased industrial activity, and sustained low interest rates.

- Reduce the federal budget deficit to 3% of GDP, compared to roughly 6% under the previous administration.

- Expand domestic oil production by 3 million barrels per day, with the aim of lowering energy costs and inflation.

While it is too early to evaluate the effectiveness of this plan, what follows is a targeted assessment of actual policy execution and economic outcomes so far, focused on four key areas: growth and markets, fiscal policy, trade strategy, and institutional integrity.

Economic growth & financial markets

Grade so far: A- | Future implications: B

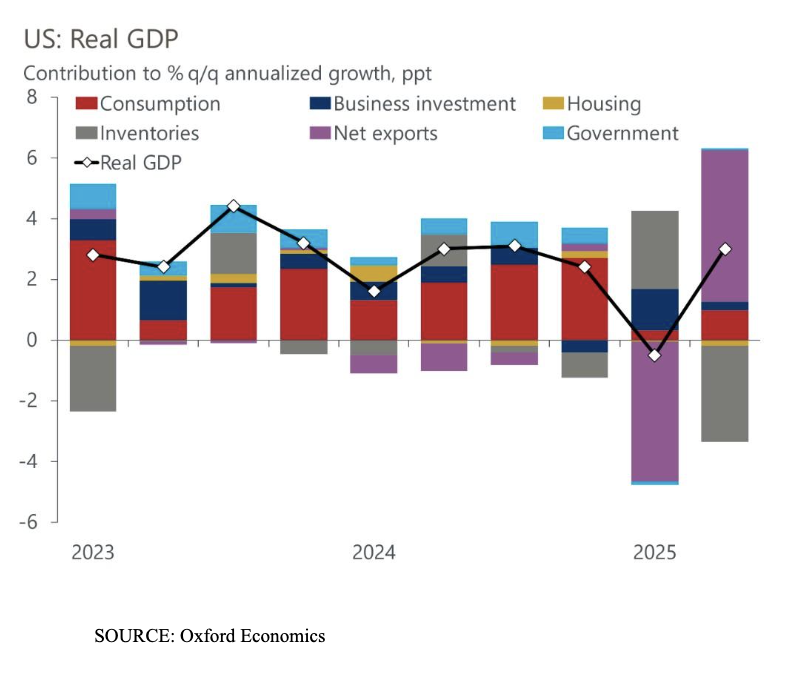

The early economic returns of the Trump administration’s second term have been broadly positive, albeit with complications. GDP growth has remained steady, bolstered by resilient consumer spending, increased government investment in defense and technology, and early effects of deregulatory momentum. While the administration’s aggressive energy posture has not yet hit its full stride, the market has forced oil prices downward in anticipation of greater supply.

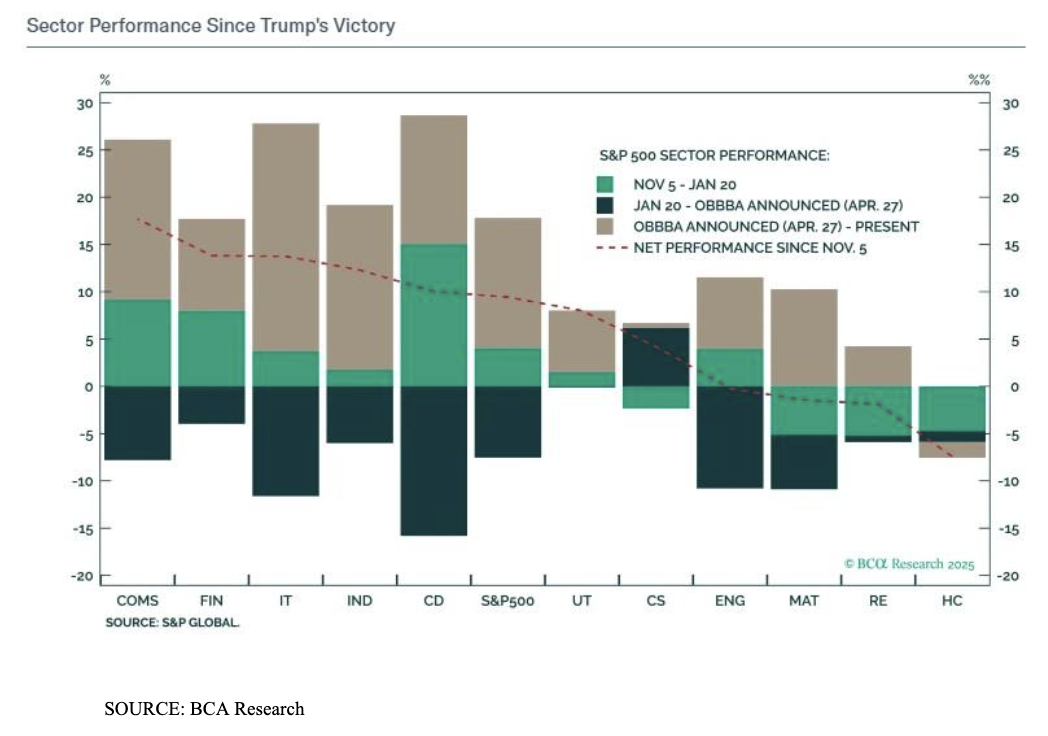

Financial markets, meanwhile, have shown strong performance in the first half of 2025. Equity indexes are up, investor confidence is rebounding, and corporate earnings are exceeding expectations. The chart below illustrates how industries such as IT, financials, and industrials have led the S&P 500 index. Much of this reflects anticipated future tax cuts, expanded defense contracts, and further regulatory easing. The administration has leaned hard into messaging around economic nationalism and domestic revitalization, and markets, at least for now, are playing along.

With this growth, there is an underlying concern about inflation. The administration’s aggressive immigration policy has exacerbated an already-tight labor market. With birth rates low and retirements accelerating, this labor supply shortage may create a bottleneck for growth. It remains to be seen if the evolution (and successful application) of artificial intelligence will offset the inflationary pressures stemming from productivity loss and a smaller labor pool.

The economic momentum is real, and 2026 could be very strong, but the growth story is not yet self-sustaining. The conditions created by these policies enhance the risk of stagflation, which entails stubbornly high inflation and only moderate economic growth.

Fiscal policy & government spending

Grade so far: C- | Future Implications: D

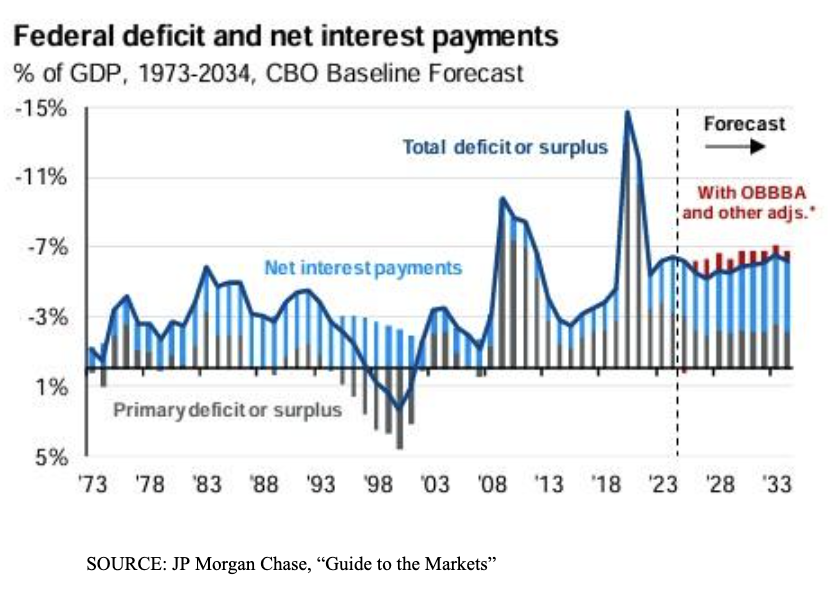

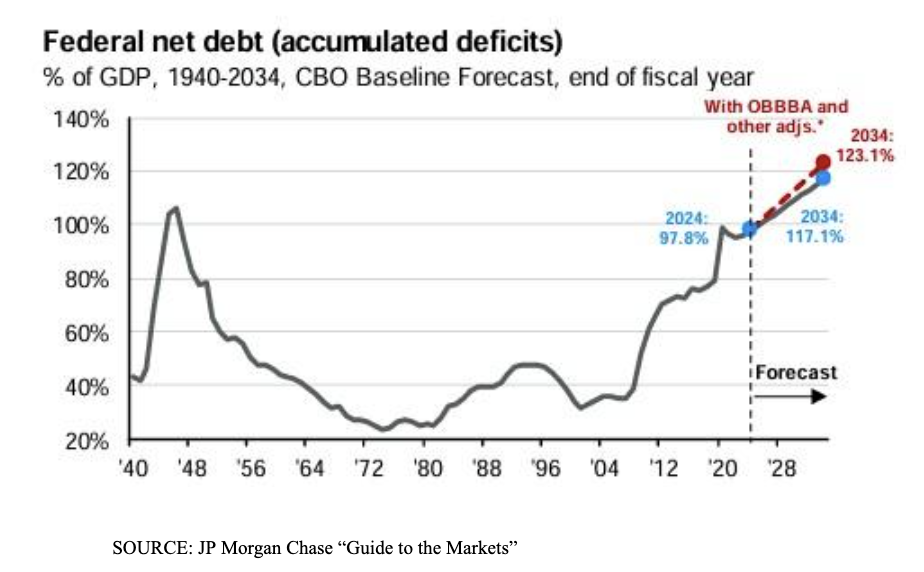

Despite aggressive rhetoric about budget tightening, the deficit has widened significantly, driven by a combination of tax favoritism, uneven spending cuts, and mounting interest obligations.

The most high-profile cost-cutting initiative, led by the Department of Government Efficiency (DOGE), claimed to have saved $175 billion by the end of May through sweeping layoffs and program eliminations as it worked toward its goal of saving $2 trillion. In practice, those cuts were executed in a dangerously haphazard manner.

Thousands of federal jobs were slashed in a matter of months, triggering administrative turmoil and legal challenges, as well as rehirings. While the savings appear legitimate, the operational fallout raises serious questions about sustainability and competence.

On the revenue side, the administration’s tax policy has leaned heavily in favor of the affluent and large corporations. The extension of the Tax Cuts and Jobs Act (TCJA) will likely deepen income inequality while adding to the already-ballooning deficit. Investors may cheer the lower capital gains taxes and higher after-tax profits provided by the bill, but from a macroeconomic standpoint, this approach risks eroding consumer demand over time and widening the already-yawning wealth gap.

One particular bright spot is the administration’s clear prioritization of defense and technology funding. Strategic investments in AI, semiconductor manufacturing, and national security infrastructure have accelerated under Trump 2.0. but even these gains come at a cost. Clean energy initiatives, climate resilience projects, and housing programs have been either gutted or deprioritized to fund these initiatives.

Trade, tariffs & global strategy

Grade so far: B+ | Future implications: C

Of all the economic levers the Trump administration has pulled in its first six months, trade policy has unquestionably had the most immediate and visible impact. The administration has fairly touted these moves as correcting long-term structural trade imbalances.

For example, the administration recently negotiated a deal with the European Union that includes a 15% flat tariff on most EU imports. While it adds a degree of friction to transatlantic commerce, the agreement stabilized what was rapidly becoming an escalating standoff. Thus far, the broader market has absorbed these tariffs with only minimal impact.

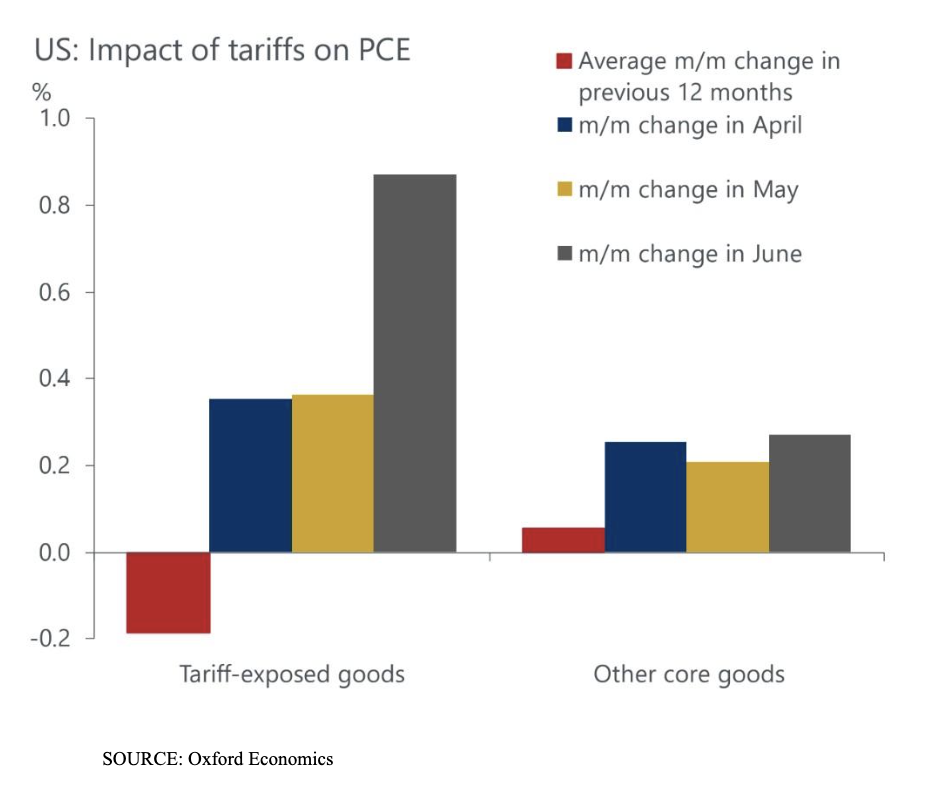

But the long-term consequences of these moves are less certain. Tariffs, by design, raise costs and — while they can protect domestic producers in the short run — tend to do so at the expense of consumers and long-term efficiency. These higher costs will either be absorbed by corporations, which reduce earnings, or will be passed along to households via higher prices.

Trump’s recent tariff surge is beginning to push higher the costs of imported goods. These extra costs will work their way through the economy, creating short-term inflation that the Fed is already struggling to contain. Conversely, multiple analyses consistently show that such protectionist measures reduce long‑run GDP growth, undermining productivity and consumer purchasing power over time.

Institutional integrity & regulatory landscape

Grade so far: D | Future implications: F

It has been widely reported that President Trump is dismayed with the Federal Reserve and its unwillingness to lower interest rates at the pace he prefers. While Trump has not formally altered the Fed’s leadership structure, his public criticisms of interest rate policy, suggestions of alternative monetary tools, and reported threats to replace senior officials have raised serious red flags. The Fed’s independence is a core pillar of investor confidence. Undermining it, even rhetorically, introduces a risk premium that affects everything from Treasury yields to currency stability.

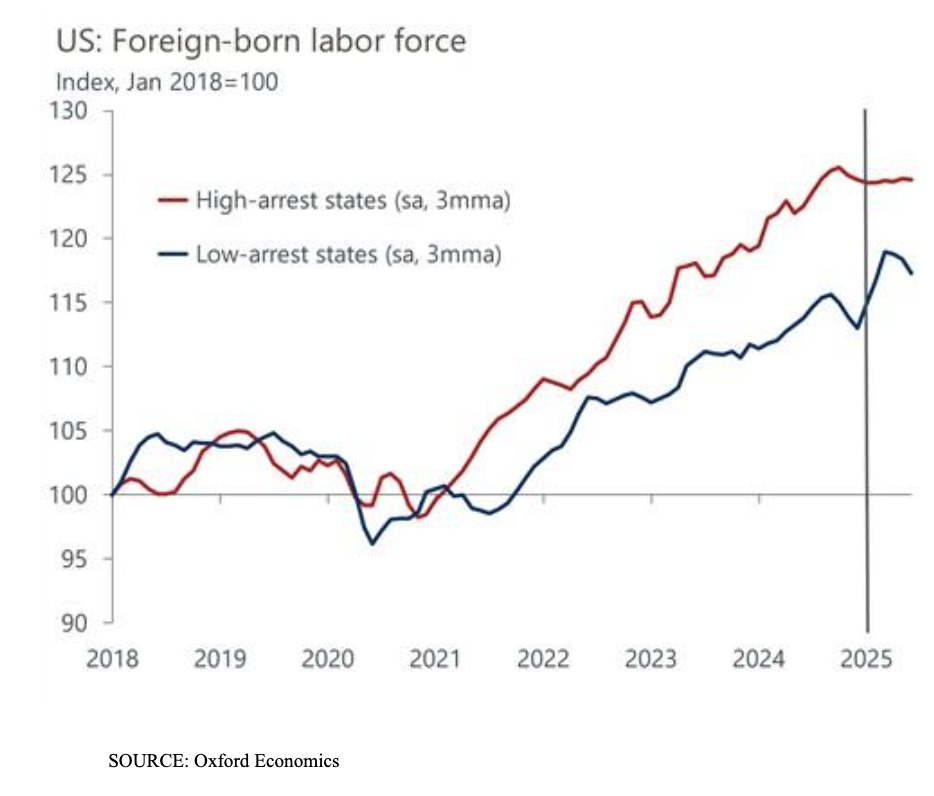

The Trump administration’s immigration policy has adopted an exceptionally restrictive stance, targeting undocumented individuals through stepped-up arrests, deportations, and bureaucratic slowdowns. This approach is directly shrinking the available labor pool, particularly in sectors like agriculture, construction, and caregiving that rely heavily on immigrant labor. Just as critically, the climate of hostility is deterring future immigration altogether, limiting long-term population growth, productivity gains, and the very workforce expansion needed to sustain economic momentum.

More broadly, the administration’s confrontational tone toward watchdog agencies, data transparency offices, and even the Congressional Budget Office is eroding norms that markets rely on to interpret policy risks. The loss of neutral, credible analysis makes it harder for investors, economists, and voters to navigate what’s coming next.

Regulatory rollbacks, a hallmark of TrumpBessenomics, have also been aggressively pursued. In the short term, they are providing exactly what markets want: fewer constraints on banks and lending, corporate behavior, lower compliance costs, and faster permitting in sectors like energy and real estate. But the long-term implications are far less market-friendly. The weakening of environmental protections, financial oversight mechanisms, and consumer safeguards increases the probability of systemic failures. Crises, as history repeatedly shows, are born in the quiet spaces where oversight was gutted for the sake of growth.

Conclusion: Navigating the TrumpBessenomics cycle

TrumpBessenomics is a maximalist economic experiment rooted in ambitious growth targets, fiscal disruption, and aggressive deregulation. In its first six months, the administration has delivered some real momentum: strong financial markets, new tariffs appear to have been absorbed without major consequence, and select sectors — particularly defense and technology — have seen meaningful investment gains. But momentum is not the same as durability.

Beneath the surface, structural risks are mounting. The fiscal outlook is deteriorating, institutional independence is under pressure, and immigration policy is constraining labor supply at a time when demographic growth is essential. The current trajectory is increasingly dependent on fragile assumptions: that growth will continue, that inflation will remain tame, and that confidence in institutions will hold. If economic growth fails to stay ahead of interest rates, the future may not be so bright.

David Tepp is the founder and managing principal of Tepp Wealth Management, a SEC-registered investment adviser based in Westfield, New Jersey. With over 20 years of experience in financial and wealth management, David provides strategic financial planning and investment advisory services to high-net-worth individuals and families. He frequently writes on macroeconomic policy, fiscal risk, and market strategy to help investors navigate an increasingly complex global economy.

Sources:

Oxford Economics, “Q2 GDP Rebound Masks Glowing Fundamentals,” written by Bernard Yaros, July 30, 2025

BCA Research, “One Big Beautiful Basket,” written by Max Malakveitshouk, July 16, 2025

https://www.cnn.com/2025/05/30/politics/doge-musk-government-savings

JP Morgan Chase, “Guide to the Markets,” July 31, 2025

Oxford Economics, “Made in America – The Manufacturing Sectors With the Best Prospects,” written by Nico Palesch, July 22, 2025

Oxford Economics, “PCE Nowcast – Tariffs Are Starting to Hit Inflation,” written by Grace Zwemmer, July 16, 2025

Oxford Economics, “ICE Arrests Proving a Hinderance to Labor Force Growth,” written by Matthew Martin, August 4, 2025

DISCLOSURES:

Tepp RIA, LLC dba (Tepp Wealth Management), is a SEC registered investment adviser. For information pertaining to the registration status of Tepp Wealth Management, A copy of Tepp Wealth Management’s current written disclosure statement discussing Tepp Wealth Management’s business operations, services, and fees is available at the SEC’s investment adviser public information website – www.adviserinfo.sec.gov (CRD# 283899) or from the Adviser upon written request: Tepp Wealth Management, 210 Elmer Street, Westfield, NJ 07090.

This article is an expression of corroborated facts along with the opinions of the author. This is for informational purposes only and is intended to inform the reader about market related activities which could affect individual portfolios and provide insight on specific relevant topics. It is not intended to recommend or suggest any specific course of action or investment strategy. The reader should not infer the likelihood of any future events. Past performance is not indicative of future results. Investors should always consult an investment professional and/or tax professionals to discuss their unique needs and objectives.

Please remember that different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment or investment strategy (including those undertaken or recommended by the Adviser), will be profitable or equal any historical performance level(s).

Tepp Wealth Management may discuss and display, charts, graphs, formulas which are not intended to be used by themselves to determine which securities to buy or sell, or when to buy or sell them. Such charts and graphs offer limited information and should not be used on their own to make investment decisions. This information is provided for guidance and information purposes only and is not a solicitation. Be sure to first consult with a qualified financial adviser and/or tax professional before implementing any strategy.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Live Virtual Event: Join Now

Upcoming Virtual Events View All