Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

- Current high P/E ratios mean future stock returns are at risk unless P/Es remain elevated or earnings growth is exceptionally strong.

- Target date funds, popular in 401(k)s, are much riskier near retirement than most realize, with significant exposure to equities and long-term bonds.

- If the stock market corrects to historical P/E averages, even strong earnings growth won't prevent large losses for equity-heavy portfolios and TDFs.

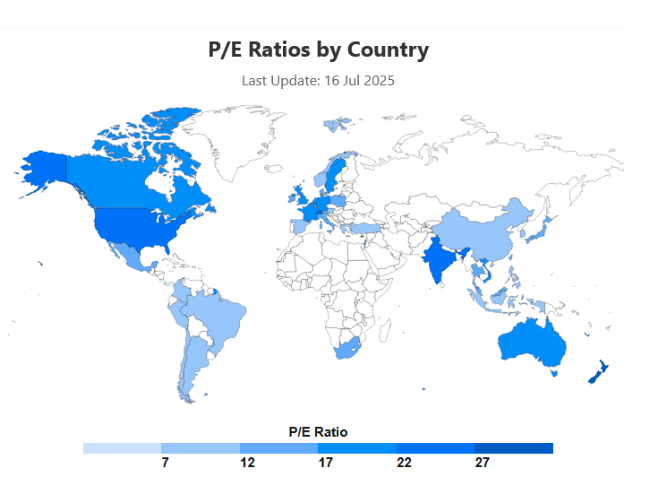

- Investors, especially baby boomers in TDFs, should consider shifting to safer assets like TIPS and Treasury bills or less expensive global equity markets.

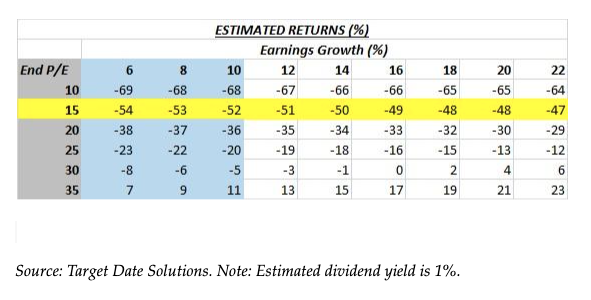

Here’s the formula for forecasting returns:

Return = Dividend Yield + (1 + Earnings Growth) X (1 + P/E expansion/contraction) – 1

And here’s a table that uses the formula to calculate returns for various levels of earnings growth and future P/E. Dividend yield is estimated at 1%.

Note the last row in the table, in which P/Es remain at their current level of 35, meaning zero P/E expansion/contraction. That estimated return is simply earnings growth (top row) plus the current dividend yield of 1% (not shown).

Note that all the rows above the last row reflect P/E contraction. All returns in those rows are negative, ranging between a 5% loss and a 69% loss for earnings growth in the range of 6–10%, the historic range.

Now consider the row highlighted in yellow, which identifies the historical average P/E of 15. P/E contraction to the historic norm produces an estimated loss of around 50%, even if earnings growth is as high as 22%.

P/E multiples need to remain at or above the current level of 35 in order to produce a positive return. Strong earnings growth above 16% could help, but P/Es cannot contract any more than 14% (from 35 to 30) if they are to earn a single-digit positive return.

Target Date Fund Losses

At $4 trillion and growing, target date funds (TDFs) are a massive part of 401(k) plans and by far the most popular Qualified Default Investment Alternative (QDIA). Most think that TDFs are safe for those near retirement, but only a few actually are. Remember that most TDFs for those near retirement lost more than 30% in 2008. Most TDFs are 85% risky at their target date, with 55% in equities and 35% in risky long-term bonds.

If the stock market loses 50%, TDFs will lose 27.5% for those near retirement — even if bonds lose nothing. Baby boomers in TDFs will be shocked.

What’s the Point?

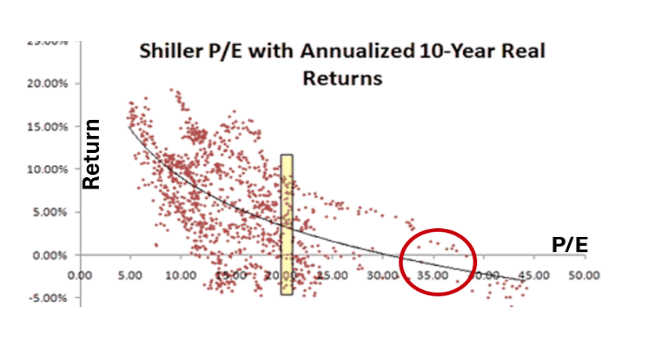

The math does not support the contention that strong earnings growth is the reason that stock prices keep going up. Investor euphoria is the reason that P/Es remain high. P/Es could get even higher, but it’s also simple math that the more you pay for a stock, the lower the subsequent return on that stock, as shown in the following.

Baby boomers in TDFs should consider getting out and moving to safety. Stock investors should consider less expensive stock markets, and safer asset classes like TIPS and Treasury bills.

Source: World P/E Ratio https://worldperatio.com/

Ron Surz is president of Target Date Solutions, developer of the patented Safe Landing Glide Path and Soteria personalized target date accounts. He is also co-host of the Baby Boomer Investing Show. Surz’s passion is helping his fellow baby boomers at this critical time in their lives when they are relying on their lifetime savings to support a retirement with dignity, so he wrote a book, “Baby Boomer Investing in the Perilous 2020s,” and he provides a financial educational curriculum.

For anyone who relies on TDFs — or advises those who do — Surz’s new book is a must-read guide to understanding the risks, solutions, and future of a secure retirement.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Read more articles by Ron Surz

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.