Life Expectancy: The (F)Law of Averages

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Let’s talk about life expectancy. More specifically – should it play a role in retirement planning? You might be surprised to learn that the answer is: Absolutely not.

At least, not in the way many people think. There’s a flaw in their thinking about the “average life expectancy.” It’s simply not a good indication of how long a person will live.

Let’s begin with a simple exercise.

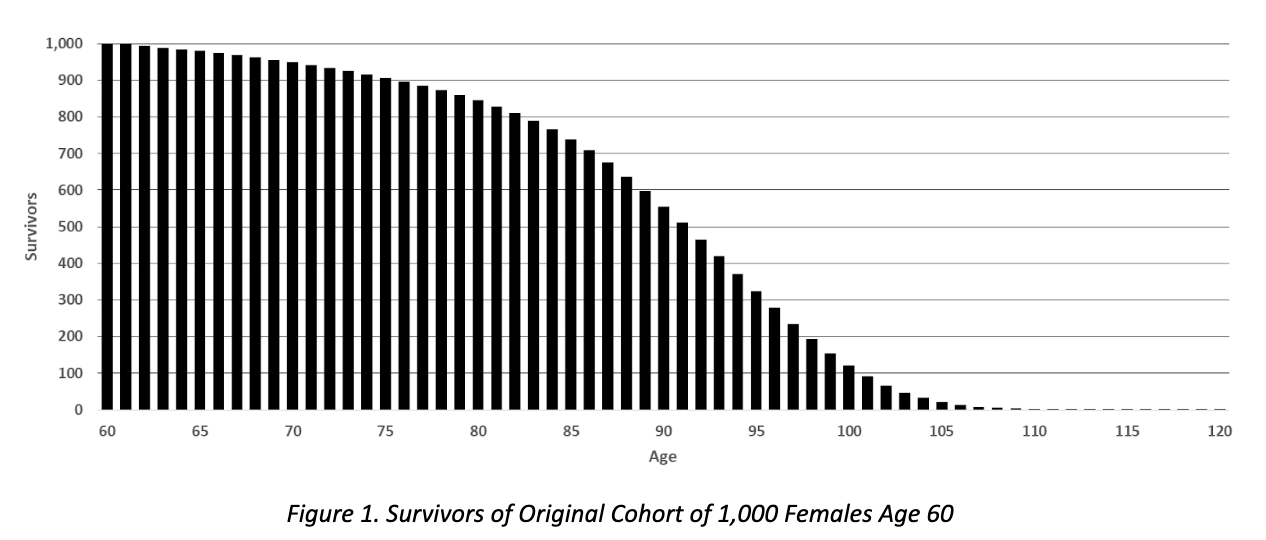

Imagine we’re tracking 1,000 women who all just turned 60. Year after year, we follow their lives. Some will pass away; others will continue on. What we’re building here is called a survival curve — you can picture it as a descending staircase, each step showing how many remain alive at each age.

In fact, if you believe that:

- Life expectancy is the age when half the people in a group have died;

- It’s a good indicator of how long someone will live; or

- It’s a sensible planning horizon for retirement income...

I regret to inform you: we need to have a serious conversation. (And if you're a financial advisor, you might want to hand in your badge at the front desk.)

Imagine a group of 1,000 women, all exactly 60 years old. If we follow them through the years, some will pass away early, others will live well into their 90s and beyond, as shown in Figure 1:

Life expectancy represents the mean (average) future lifetime at a particular age. For these 60-year-old women, that’s 29.17 years. So, on average, they’ll live to about 89.17. Sounds useful, right? Not so fast. Here’s the catch: average doesn’t mean typical, and it certainly doesn’t mean safe. It’s definitely not a magic number you can plan your retirement income around.

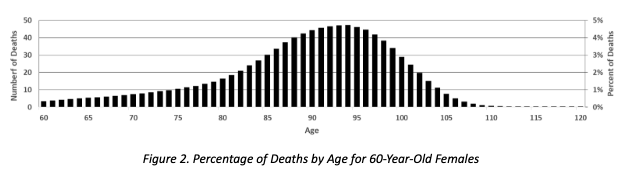

The number who die at a given age is simply the difference between the height of one bar in Figure 1 and the immediately following one. We look at the number of deaths at each year of age in Figure 2:

The most common age at death in our group — the mode — is 94. That means more of our 1,000 women die at 94 than at any other age. If you plan your retirement to end at 89, you’re not just playing with fire — you’re practically inviting it in for dinner!

If this age seems high to you, it applies to females turning 60 in 2025, reflects mortality improvement in future years, and is based on individuals in sufficiently good (not perfect) health willing to purchase a lifetime annuity. However, the same concepts apply to the general population.

Think about it: if every one of those 1,000 women lived exactly 29.17 more years and then passed away on the same Tuesday morning in the year 2054, planning around life expectancy would work beautifully. (Also: The obituary section would be wild that week.)

But that’s not how life works. We don’t live — or die — on schedule.

Where’s the Flaw?

Life expectancy is just an average. And relying on an average for something as individual and variable as human life? That’s The Flaw of Averages.

It’s obvious that it would be a disaster to set up a retirement income program that covered an individual for a period of time equal to her life expectancy as calculated at inception of retirement income. Quite simply, it’s not enough to plan for the average future lifetime because you might not be average.

Let’s go one level deeper.

At age 89.17 — the actual so-called “life expectancy” — nearly 60% of our group is still alive. That alone should stop any advisor from using it as a cutoff point for retirement income planning. And yet, I often hear advisors say things like “average life expectancy.” That’s a double whammy: not only is it redundant (life expectancy is already by definition an average), but it reveals a deeper misunderstanding of what the number actually represents.

To calculate life expectancy, we track how many people survive each year, then tally up the fractions of years lived across the cohort. This process gives us an average — but again, it doesn’t tell us about you, your client, or anyone in particular. It only tells us about the group.

Want to make it even more precise? We can distinguish between curtate life expectancy (which only counts full years lived) and complete life expectancy (which adds a half-year, since people die on average midway through a year). For our group, curtate life expectancy is 29.17 years; complete is 29.67. That difference matters if you're splitting hairs — but neither one makes for a sound financial plan.

Imagine we start with 1,000 women who are all 60 years old. If 996 of them are expected to survive to age 61, then — on average — each original member of the group lives 0.996 years during that first year. Now, suppose that 992 of those 996 women survive to age 62. That means, during the second year, each original member of the group lives an average of 0.988 years. This is calculated by multiplying 99.6% (who made it to 61) by 99.2% (who survived to 62).

This process continues year by year, until none of the original group remains. If we add up all the fractions of a year lived across the years, we get the group’s life expectancy — the average number of years a member of the original group is expected to live. Life expectancy is a population-level measure. It’s valuable for comparing life expectancy of different countries — but it’s not a practical tool for personal retirement income planning.

Why? Because you, the individual, are not a “population.”

You’re one person. And variability — the range of possible outcomes — is far more important than any single average.

The Insight in the Curve

As Figure 2 makes obvious, life expectancy is a poor predictor of individual outcomes. It’s not representative of any individual’s time frame for retirement income. Rather, life expectancy is calculated as an average measure of a large population and is best viewed through that lens.

Life expectancy is different than life span. Life span is the upper age limit to which any humans are assumed to survive, typically taken as age 120, as in Figure 1. Life expectancy is a simple average — a single number that summarizes survival across a group. But it’s a blunt tool. It misses the nuance shown in a full survival curve (like Figure 1) or a distribution of deaths (like Figure 2).

For example, if a group of 60-year-old women have a life expectancy of 30 years, some of that average comes from years after age 90 – it also includes years lived during the next 30 years, from ages 90 to 120. That’s why life expectancy is best understood as a population-level measure. It reflects the overall pattern of a group, not the fate of any one person.

Sir Francis Galton, the great statistician, once mocked the obsession with averages. He joked that an Englishman so bored by the Swiss Alps wished the mountains could be shoved into the lakes — “two nuisances gone at once." Galton’s point? Averages can be blind to the beauty and complexity of variation.

Or to put it another way: When Bill Gates walks into a room, that makes the room’s occupants billionaires on average. But unless you're Bill, that statistic doesn’t mean you should now feel free to buy a yacht.

The Bottom Line

Planning your retirement based on life expectancy is — for the majority — planning to run out of money. It’s the financial equivalent of flying a plane over the Himalayan Mountains at just above 20,000 feet, their average elevation — despite well over 100 mountain peaks, including Mount Everest, exceeding this height. It might sound good in theory — but in practice, it’s dangerous.

Instead, focus on the full distribution of outcomes. Look at survivor curves, not single-point estimates. Plan for longevity, not for averages. Be a superstar advisor: Forswear all use of life expectancy in retirement planning.

Because in retirement, as in life, it’s not about being average.

It’s about being prepared.

Jeffrey K. Dellinger, FSA, MAAA, is the author of Another Day in Paradise: The Handbook of Retirement Income, available on Amazon and at retirementincomehandbook.com. This landmark book is written for individuals on the cusp of retirement and takes you step by step through understanding and solving the retirement income challenge.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All