Buffer ETFs vs. T-Bills: A Total Cost of Ownership Perspective

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

When Your Investment Time Horizon Collapses, Is It Time for a Buffer ETF?

A few months ago, my husband and I became empty nesters. To celebrate, we bought a mid-century modern house in need of renovations. And just like that, our investment time horizon contracted.

During our working years, we consistently deployed spare cash into a 70/30 stock/bond portfolio. Taking the long view, we stayed invested and then rebalanced into equities when the market dipped in 2009 and 2020. Our stamina had two sources: grit and a long investment horizon.

Our new venture abruptly changed our time horizon. Now part of our stocks and bonds are earmarked to fund a major remodel. A significant market correction would mean skimping on the remodel or postponing it altogether. It’s time to de-risk the part of our portfolio earmarked for renovations. That means reducing or eliminating equity market exposure and trimming bond duration and credit risk.

Which Off Ramp Should We Take?

Traditionally, the best way to do this is via CDs or T-bills, but in the summer of 2023 Innovator ETFs began rolling out a series of ETFs designed to offer complete downside protection and modest upside opportunity linked to popular indexes such as the S&P 500. These “100% buffer” ETFs have a fixed protection/upside term, tied to the expiration date of the portfolio’s options contracts. First Trust, Calamos, Prudential, and BlackRock soon launched copycat products.

Many buffer ETF providers advertise these products as substitutes for bank products such as CDs. However, for residents of high-tax states, T-bills are more attractive than CDs, so for us that’s the more relevant comparison.

Comparing Investment Characteristics

T-bills have fixed maturities and yields. Barring a massive default, T-bills have no downside. The trade-off here is the fixed upside. There’s no opportunity to profit from rising stock markets.

100% buffer ETFs combine index exposure (via an ETF like SPY or IVV) with an at-the-money protective put. Because these put options can be pricey, the buffer ETFs offset the cost by selling an out-of-the-money call. As a result, these funds provide complete downside protection vs. their underlying ETF to those who purchase when the put options are at or in the money. They also offer capped upside exposure, as long as their call options are not yet in the money.

The 100% buffer ETFs offer a clear payout profile to those who buy them at the moment the options positions are initiated. After that instant, the payout profile depends on both the current price of the underlying ETF and the trading price of the buffer ETF, which should reflect current options values as well as creation costs and trading spreads. Market imbalances may also create temporary premia or discounts.

Calculating what to expect at maturity from a buffer fund purchased between reset dates is a tricky business. I spent 7 years as an options trader, and 15 as an ETF expert, and still I spent a week doing a deep dive before I figured out a rubric.

Buffer ETF Due Diligence

I decided on a two-step due evaluation process. First, select the best 100% buffer ETF for our time horizon. Next, compare it to a T-bill with a similar maturity date.

The selection process took some effort. I had to come up to speed with the product terminology and each issuer’s conventions. Some adjusted the buffers and caps to account for the fund’s expense ratio; others stated them in gross terms.

I also had to select a reference asset and a maturity date. I chose the S&P 500 (sometimes appearing as IVV or SPY) as the underlying asset, because every asset manager offers one. Date-wise, we are hoping to start construction in early 2026, so I selected products containing contracts maturing in December 2025. (I chose Innovator’s 1-year product over their 2-year one, because its contract inception date matched the competitors’.)

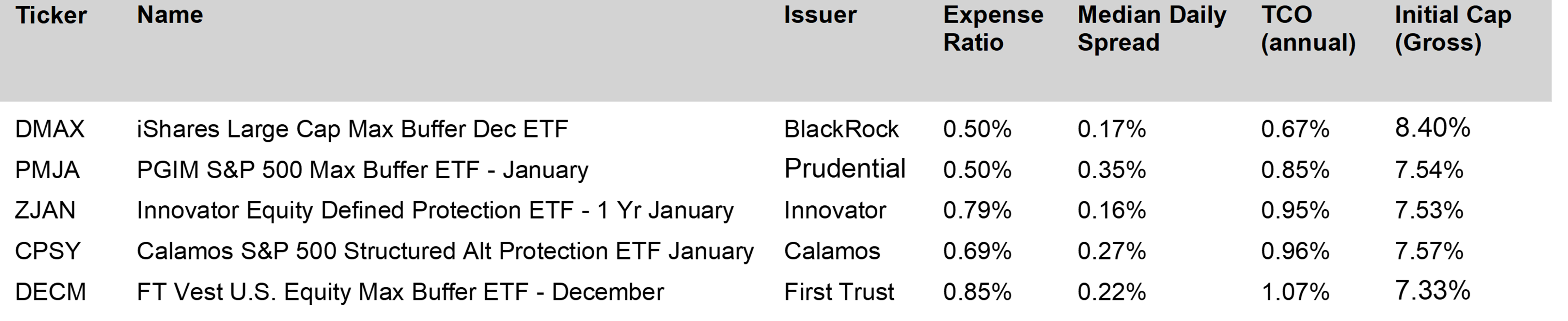

This yielded five choices.

Sources: FactSet, iShares, PGIM, Innovator, Calamos, First Trust

The term for the First Trust’s FT Vest U.S. Equity Max Buffer ETF – December (DECM) is slightly offset from the others. Luckily, its option contract terms are comparable to the rest.

Each should be evaluated based on total cost of ownership (TCO) and the attractiveness of its options positions.

The iShares Large Cap Max Buffer Dec ETF (DMAX) is the cheapest to own. Its expense ratio of 0.50% ties PGIM S&P 500 Max Buffer ETF – January (PMJA) as the cheapest options.

Trading costs also matter. Innovator Equity Defined Protection ETF - 1 Yr January (ZJAN) posts the tightest median bid-offer spreads, at 0.16%. DMAX trades a hair wider, at 0.17%.

The combined measure, TCO, shows the total cost to own each ETF over a 1-year period. DMAX is the clear winner, at 0.67%.

DMAX also offers the best options exposure, with its year-end upside capped at 8.40% gross, which is 0.83% better than runner-up Calamos S&P 500 Structured Alt Protection ETF January (CSPY). All offer 100% downside protection, after fees, and all reset on the first trading day in January, so the upside is the differentiator.

Congratulations, DMAX, and welcome to the final show-down: Best 100% buffer vs. T-bill.

Where in the Payoff Profile Are We?

The next step was to figure out the current payout profile, given IVV’s closing price and the trade date. I ran my analysis on May 12, 2025, when IVV closed at $585.71.

DMAX’s put options on IVV have a strike price of $588.68. IVV’s closing price was just 0.51% below that threshold, meaning that DMAX’s put was in the money, barely. Anyone buying DMAX with IVV at this price would have 100% S&P 500 downside protection through the end of the year.

DMAX holders could see some upside if IVV trades above the put strike price, until it hits the cap, which is 8.95% above today’s closing price.

In other words, after much year-to-date volatility, IVV’s price is just 0.51% away from where it was on DMAX’s issue date, with the appreciation zone well within reach. That makes for a relatively clean comparison between DMAX and T-bills.

DMAX’s upside is known. The downside can be calculated, once we factor in DMAX’s costs. And then we can run a comparison.

The Competitor: A Boring T-Bill

The T-bill that best matches DMAX’s options expiration timing has a maturity date of December 26, 2025. Its closing yield (quoted on the mid-point) was 4.1076%, as of May 12, 2025.

Tradeoffs

For this next section, which will compare costs and returns, all calculations will be scaled through the end of 2025, a period of 233 days. Please note this is a touch imprecise, as the actual T-bill in question matures on December 26.

DMAX’s protection comes at a cost, which includes the TCO inputs of expenses and spreads, as well as changes in options valuation and potentially trading discounts/premiums, which are jointly expressed as its price appreciation since launch.

Now we can figure out the best- and worst-case outcomes.

Because of the protective put, DMAX’s downside is limited to the investor’s costs. Its upside is the gross option cap, adjusted downwards for the costs. This is how it plays out:

In an opportunity cost framework, DMAX investors pay costs and forgo T-bill yields in exchange for additional upside. The opportunity cost amounts to 4.13%. Would you pay 1.53% in order to net up to 6.87% when you know you could earn 2.60% without any volatility?

DMAX’s holders apparently think so.

One reason might be the tax treatment.

Unequal Taxation

Despite their fixed option terms, buffer ETFs don’t mature. To cash out, DMAX’s investors must sell their shares.

If all goes well, they will realize a capital gain, which will be taxed at the federal level at no more than 23.8%, assuming they've held their shares for at least a year. T-bill interest is taxed as ordinary income, with rates as high as 37%. Long-term capital gains of 2.60% become1.98% after the federal tax, but the same amount of ordinary income leaves investors with just 1.64%. And that’s just what Uncle Sam shaves off.

Capital gains of 2.60% become1.98% after the federal tax, but the same amount of ordinary income leaves investors with just 1.64%. And that’s just what Uncle Sam shaves off.

At the state level, T-bill interest is tax-exempt, while capital gains are fully taxable. In California, capital gains rates max out at 13.3%, for those earning over $1 million/year. The Golden State’s highest earners do not benefit from capital gains treatments: 23.8% + 13.3% = 37.1%, which is 0.1% above the top ordinary income rate.

Now What?

The choice between a 100% buffer ETF such as DMAX and a T-bill involves risk tolerance—shouldering costs in the hope of a payout—and a tax analysis based on each investor’s state and income.

Personally, I’m not excited enough by the prospect of earning up to 4.27% above T-bill rates (if the S&P 500 ends the year at least 8.95% higher than today’s close) to fork over 1.53% in known costs.

Downside protection is our primary goal, so trimming our construction budget for an uncertain modest payback doesn’t make much sense. My husband and I won’t get much value out of tax arbitrage—our mid-century modern fixer upper has a California address. Even worse, if selling DMAX at the end of the year creates a capital gain, it will be short-term, and therefore taxed as ordinary income, thus increasing our tax burden.

So we will pass on DMAX as a cash substitute. Would you do the same?

This blog post is for informational purposes only. The information contained in this blog post is not legal, tax, or investment advice. FactSet does not endorse or recommend any investments and assumes no liability for any consequence relating directly or indirectly to any action or inaction taken based on the information contained in this article.

Elisabeth Kashner, CFA Vice President, Director of ETF Research and Analytics

Ms. Elisabeth Kashner is Vice President, Director of Exchange-Traded Fund Research and Analytics at FactSet. In this role, she develops tools and methodologies for all aspects of ETF and mutual fund classification and analysis with a focus on costs, risks, trading issues, and performance. Prior, she served as director of research at ETF.com and published extensively on the classification, efficacy, and persistence of strategic beta strategies and robo-adviser portfolio exposures. Ms. Kashner earned a BA from Brown University and an MS in financial analysis from the University of San Francisco. She is a CFA charterholder.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All