International Investing: A New Paradigm?

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits The views presented here do not necessarily represent those of Advisor Perspectives.

The views presented here do not necessarily represent those of Advisor Perspectives.

The University of Chicago’s Center for Research in Securities Prices (CRSP) shows that between 1926 and 2024, U.S. stocks earned an average annualized return of 10.3%, while international stocks returned only 7.8% annually. Both were measured in U.S. dollars. But this year is a different story.

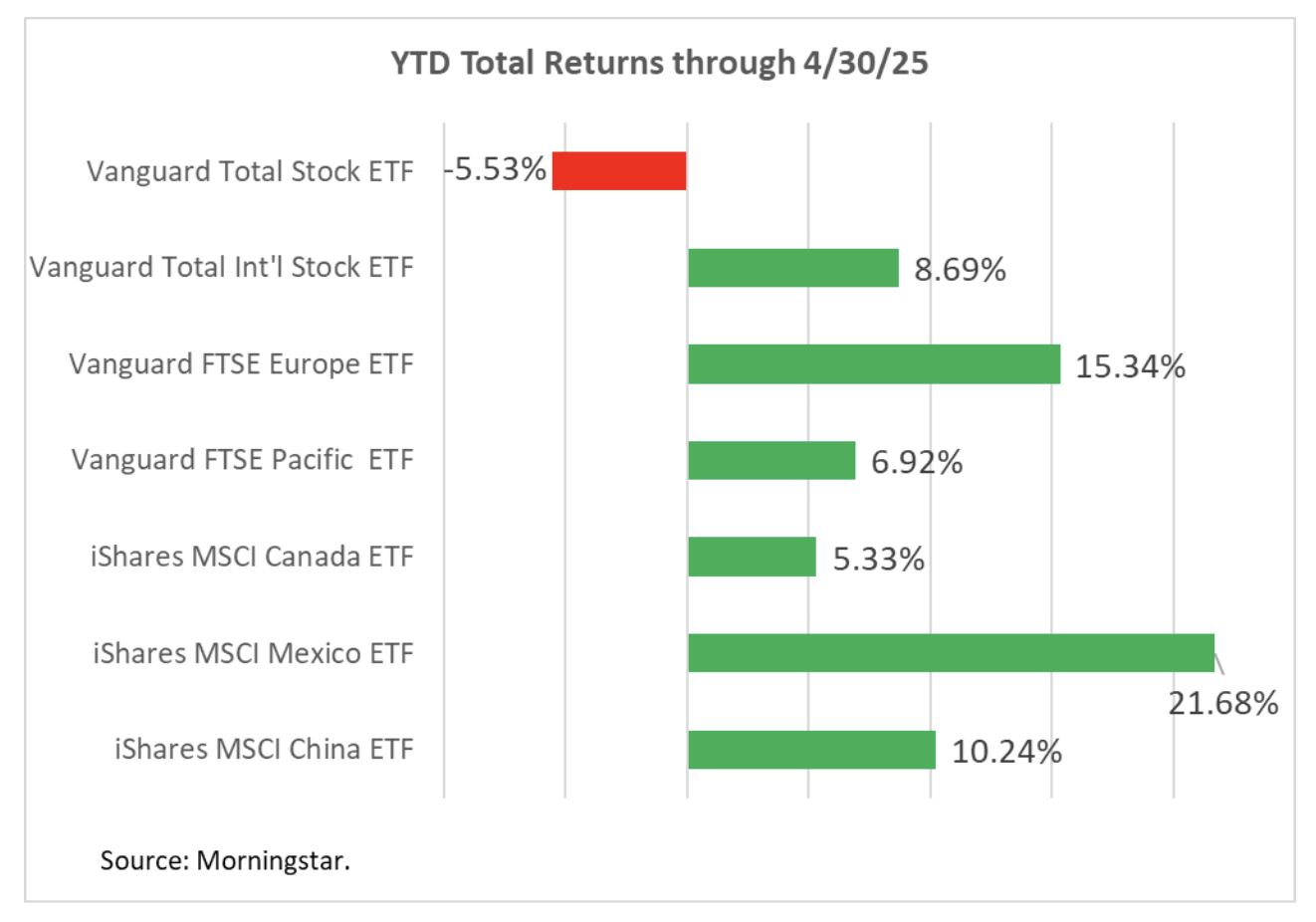

As of April 30, 2025, the Vanguard Total Stock Market ETF (VTI) is down 5.5%, while the Vanguard Total International Stock ETF (VXUS) has gained 8.7 %. That’s a 14.2 percentage point differential. And the Vanguard Europe ETF (VGK) gained 15.3%, or a staggering 19.7 percentage point differential. Is this just a short-term anomaly, a case of mean reversion, or are we witnessing the emergence of a new investing paradigm?

The last decade has seen the dominance of the U.S. in global markets. For the 10 years ending December 31, 2024, U.S. stocks gained an average of 12.5% annually, while international stocks gained only 5.1%. That’s a 224.8% gain for U.S. stocks and only a 64.4% gain for international.

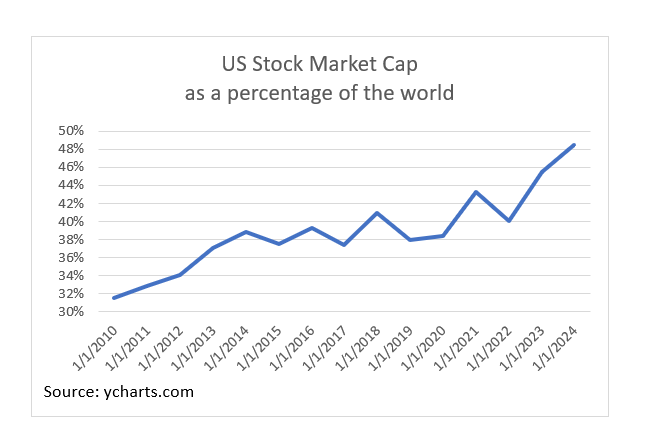

The value of the U.S. stock market as a percentage of the world grew dramatically, as shown in the following chart that reflects full market capitalization. As measured by free-floating shares (only publicly traded), the U.S. is more than 60%.

Driving the dominance of U.S. stocks was the economy. The GDP of the U.S. grew from about 22% to 26% of the world over the 10-year period. Unemployment fell to record-low levels not seen in over half a century. In 2008, the U.S. economy was about the same size as the eurozone. By 2023, it was nearly twice that size. The U.S. dollar was dominant, gaining 19.8% versus other currencies, as measured by the US Dollar Index (DX-Y.NYB).

The stock market is theoretically the net present value of all future cash flows, and markets rewarded the growth in the U.S. as measured by the US Dollar Index. In addition, technology innovation drove U.S. stocks. All of the Magnificent Seven are U.S. based.

Why is this year different?

So what has caused such a surge in international returns versus the U.S. so far this year? Is it just short-term noise, reversion to the mean, or something more systematic?

If the last few months were purely short-term noise, we will soon know, as U.S. stocks will resume dominance.

There is significant evidence to support the explanation that reversion to the mean is the cause. Many have been arguing that international stocks are currently a much better value than U.S. stocks. In early November 2024, Vanguard’s 10-year forecast for international stocks was that it would return an average of 7.9% annually versus only 3.8% for U.S. stocks. That differential of 4.1 percentage points has been reduced to only 1.8 percentage points in its March 31, 2025 updated forecast.

Furthering the argument not to jump to conclusions, on March 13, Morningstar’s John Rekenthaler presented some strong evidence that “Tariffs Aren’t the True Cause of the Markets’ Selloff.” He wrote, “Because current performances owe to the marketplace disruption that arises from risk-on, risk-off conduct, rather than a careful assessment of the economic impact of tariffs, the downturn could be brief.”

Yet less than a month later, Rekenthaler penned a piece, “This Time It Really Is the Tariffs,” in which he presented data to support the conclusion. He wrote, “I will not write the same today. President Trump’s Liberation Day tariffs are the most radical economic proposal of my lifetime.

If enacted, they will reverse a 75-year trend of increasing free trade and mutual cooperation among the world’s developed nations. The global marketplace would begin a new era.”

The 2024 Nobel Prize was awarded to Daron Acemoglu, Simon Johnson, and James A. Robinson for their groundbreaking work on the economic impacts of political systems. They demonstrated how democratic systems foster inclusivity, openness, and sustained growth, while autocracies, despite initial economic gains, often stifle these critical factors over time. One vivid example is the per capita GDP of South Korea being at least 25 times larger than that of North Korea.

Democracy Investments has an ETF called the Democracy International Fund ETF (DMCY) that weights each country based on a combination of market capitalization and the Economist’s Democracy Index. The following is a chart from its website along with the Nobel Prize press release.

It’s hard to argue against the fact that, over the last few months, power has been more consolidated in the executive branch, away from Congress and the courts. One example is the radically escalated tariffs being enacted unilaterally by the executive branch. The constitutional authority to levy taxes, including customs duties (tariffs), indisputably rests with Congress.

However, various laws over the past few decades have ceded more authority to the executive branch. The Brookings Institute notes the trade war really began six years ago under President Trump, and the tariffs levied then were largely retained by President Biden. But new and proposed tariffs take the war to new levels.

I spoke with Dr. Richard Rikoski, chief economist at Democracy Investments. I asked him if he thought next year’s Economist democracy score would show a major change for the U.S. He declined to answer, but he did note the U.S. democracy score had been declining over the past decade. Dr. Rikoski told me that the next few months will be crucial for the future of the U.S. stock market.

He said, “If we tariff the whole world, ultimately we just tariff ourselves.”

Indeed, most of the world could have far more free trade with each other and the U.S. could be isolated. Democracy Investments CEO Julie Cane told me, “Despite the decline in democracy in the U.S. and internationally, I am an optimist. I continue to be bullish on democracy over the long run.”

My advice to clients

Several clients have told me something like, “This time feels different.” One wrote to me: “I predict that Europe will replace the United States as the world’s leading destination for business investment.”

Even the dollar, as the world’s reserve currency, is being tested. It gave up 8.2% of its value so far this year as of April 30. In addition to tariffs, other damages to the U.S. economy come from sources such as reduced international travel to the U.S. and Canadians selling their U.S. homes as we pull back from our traditional allies.

I tell clients that though this down market feels different, they all do. So far, this down market is pretty tame compared to the dot-com crash, the Great Financial Crisis, and COVID. All three of those bear markets were accompanied by the phrase “this time is different” as the reason to sell low.

I agree with John Rekenthaler that the outperformance of international stocks is due to the tariffs and the uncertainty around them. He notes that for more than 40 years, U.S. equity investors have benefited from buying on dips. But I also agree with Rekenthaler’s conclusion that it would be rash to assume that recent stock market history will repeat. Then again, I didn’t know markets would quickly recover during the last three bears.

I’ve long been a believer in international investing as part of a diversified strategy. Though nobody wins a trade war, markets are signaling that the U.S. will be the biggest loser. Particularly in times like these, I’m glad to have recommended that international stocks comprise a third of equities.

For the vast majority of my clients, I’ve had them take risk off the table only because they are winning or have won the game, meaning they have enough to live on for the rest of their lives. Stocks are risky, and Edward McQuarrie, Professor Emeritus at Santa Clara University, set the record straight that stocks don’t always outperform bonds for the long run.

Anyone who claims they know the duration and scope of this trade war is kidding themself. Ironically, it’s easier to convince clients to have significant international stock exposure now that it has outperformed the U.S. I can say with 100% certainty that it would have been better to accept that recommendation at the beginning of the year.

The ever-growing size of the U.S. debt continues to be an argument for international investing. I’ve been somewhat neutral on international bonds but am warming up to the idea of having a little.

The Vanguard Total International Bond ETF (BNDX) has a fairly high credit rating and a 0.07% annual expense ratio. It’s hedged to the U.S. dollar, which I thought was a good thing. However, if the U.S. dollar loses the status of the world’s reserve currency, that may no longer hold. The iShares International Treasury Bond ETF (IGOV), in contrast, is unhedged, though it has a 0.35% annual expense ratio.

And bonds are much more attractive than they have been in a long time. As of April 28, 2025, a 30-year TIPS ladder can protect investors against the unknown of inflation and produce a 2.3% return above inflation and a 4.6% real safe withdrawal rate for 30 years. That will likely be the most valuable asset should the U.S. falter and lose its reserve currency status.

In short, I acknowledge client concerns that this time feels different. That said, I’m changing virtually nothing. I don’t know anything the market doesn’t already know. Jason Zweig, author of the Intelligent Investor column at The Wall Street Journal, recently wrote me that "Every investing decision that can be made according to predetermined rules should be made by those rules." I couldn’t agree more.

Allan Roth is the founder of Wealth Logic, LLC, a Colorado-based fee-only registered investment advisory firm. He has been working in the investment world of corporate finance for over 25 years. Allan has served as corporate finance officer of two multibillion-dollar companies and has consulted with many others while at McKinsey & Company.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All