Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

You could say exchange-traded funds (ETFs) changed everything.

They took the concept of a mutual fund, rewrapped it in a low-cost, easily traded package, and offered it to investors on a silver platter. Today, ETFs account for $15 trillion AUM globally, making them one of the most dominant forces in modern markets. And behind the scenes, they’re working even harder than you think.

The revenue engine inside ETFs

Investors may assume their ETFs are sitting idly in their portfolios, passively tracking an index. But in the background, ETF issuers are constantly putting those holdings to work – lending out the underlying securities to generate additional revenue.

In recent years, securities lending has contributed an average boost of 1 to 9 basis points to fund returns. This additional income helps offset operational costs and reduce fees for investors. For example, Vanguard, which recently announced its largest fee cut in history, has been able to offset between 23%-90% of its mutual fund and ETF expense ratios through securities lending.

Cambria has seen similar success, with some of its ETFs generating enough securities lending revenue to cover its entire expense ratios – effectively making them cost-neutral for investors.

While not all ETFs achieve this level of offset, the additional income from securities lending can effectively reduce the net cost of ownership for investors. They may not realize it, but this mechanism is constantly at work, making their ETFs more cost-effective and competitive.

Now for the real magic: Individual investors, via their advisors, can lend out their ETFs, too.

The next layer of value generation

ETF issuers have been collecting extra revenue this way for years, but some investors don’t realize they have access to the same opportunity through fully paid lending. By lending out the ETFs in their portfolios, they can generate passive income while staying invested.

And here’s the thing: Almost everyone is already doing it. From institutional investors to retail investors through their trading platforms, many are already seizing the opportunity to lend out their securities. If you’re not, you’re leaving money on the table.

The lending market for ETFs is active and full of opportunity. ETF lending rates in the U.S. averaged 73 basis points in 2024, according to this S&P snapshot.

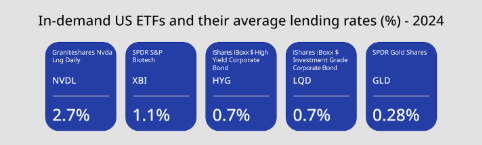

Here’s a look at some of the ETFs that saw high demand for borrowing in 2024:

The securities presented above are based on Sharegain’s proprietary lending data from 1 January 2024 to 31 December 2024 and are provided for informational purposes only. The lending rates displayed represent the ‘price’ borrowers are paying to borrow securities on the given date. This is quoted as a percentage (annually).

As with all investment activities securities lending can involve risk, and past performance or demand does not necessarily predict future results. The inclusion of specific securities on this list does not constitute an endorsement or recommendation to buy, sell, or hold any security. Investors should conduct their own research and consult with a qualified financial advisor before making any investment decisions. Please note, the lending of an ETF or security is determined by market demand. If there is no demand, the asset will not be lent out.

Who wants to borrow ETFs?

Some investors hesitate to lend stocks, fearing they’re handing their shares to short-sellers who want to drive down the prices. While that’s a common misconception about lending in general (read more here), it’s even less relevant for ETFs – where borrowing is driven primarily by market making and hedge funds.

- Market makers borrow ETFs to keep bid/ask spreads tight, ensuring smooth trading and liquidity.

- Hedge funds use them for arbitrage strategies, capturing small price discrepancies across markets.

In fact, lending ETFs helps markets to function more efficiently, creating better outcomes for all market participants by improving liquidity and price stability.

Understanding the risks of ETF lending

Like any investment strategy, ETF lending comes with risks that investors should understand. However, these risks are considered relatively low due to strong safeguards and mitigations in place.

-

Counterparty risk – The risk that a borrower defaults and fails to return the securities. This is mitigated by rigorous borrower selection and overcollateralization, meaning borrowers must post collateral that typically exceeds the value of the ETF loan. This ensures investors are always fully covered.

-

Collateral risk – If cash collateral is reinvested, it introduces market risk. Choosing a noncash collateral program or a conservative reinvestment approach helps mitigate this.

-

Loss of voting rights – Lending ETFs transfers ownership temporarily, meaning investors lose voting rights during the loan period. However, ETFs can be recalled ahead of key dates if voting is a priority.

-

Dividends & coupons – When ETFs are on loan, dividends are paid as a manufactured payment by the borrower and may be subject to different tax treatment than regular dividends. Investors can choose not to lend during dividend periods. They should consult a tax advisor to understand the broader tax implications.

-

Regulatory oversight – ETF lending operates within a well-regulated framework, ensuring transparency, risk controls, and investor protections.

These factors make ETFs a strong candidate for lending, offering a balance of opportunity and careful risk management.

The potential of ETF lending

ETFs are often perceived as a passive investment tool, designed to make investing easier for individuals. However, the truth is that ETFs are actively working behind the scenes, creating value beyond their core function. While they remain in portfolios, they can generate additional opportunities for income.

ETF lending is already benefiting issuers, institutional investors, and many retail investors. However, some advisory clients may not yet have access to these potential benefits. For financial advisors, this presents an opportunity to help clients unlock greater value within their portfolios, potentially generating additional income while enhancing their investment strategy.

As ETFs continue to provide value, advisors can explore the potential of ETF lending to further maximize portfolio returns and enhance client outcomes.

Robert Akeson, CFTe, is the director of sales US at Sharegain.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Read more articles by Robert Akeson

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.