Is the Future of Financial Advice Online?

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

The internet and other online solutions are an increasingly important resource for Americans when making savings and investment decisions. For example, leveraging data from the Survey of Consumer Finances, we find that among households with at least $100,000 in financial assets (in 2022 dollars), the percentage of 25-34-year-olds who note using the internet or an online service for savings and investment decisions increased from 27% in 2001 to 74% in 2022. For 65-80-year-olds, the increase was from 9% to 38%. Even when controlling for aging (i.e., focusing entirely on organic growth), there is clearly growing interest in online tools and guidance among Americans, especially among households from ages 45-54.

The adoption of digital advice solutions (e.g., robo-advisors) has been relatively stagnant. However, the growing acceptance of the internet as a resource for investment savings decisions, the increasing sophistication of advice solutions (e.g., leveraging artificial intelligence), and the ability to offer solutions at an attractive price point suggest the possibility of rising growth in the future. The defined contribution (DC)/401(k) space seems especially ideal for digital advice solutions given the relatively low average balances within DC plans today and the economies of scale in the market.

Therefore, while it seems unlikely that digital solutions or the internet will ever fully supplement human advisors, the ecosystem of financial advice and information is likely to continue to evolve and increasingly be online in the future.

Sources of investment and savings advice

The U.S. continues to shift toward defined contribution plans, such as a 401(k)s and 403(b)s as the primary means of savings for retirement. As a result, households are increasingly forced to make relatively complex financial decisions, such as how much to save for retirement, how to invest those savings, when to potentially retire, how much to spend in retirement, etc. Therefore, the need for advice around financial matters is becoming increasingly important.

While financial advisors would be one obvious option to help households make more informed financial decisions, usage of advisors varies notably. For example, we can leverage data from the Survey of Consumer Finances (SCF),1 which is a triennial cross-sectional survey of U.S. families with detailed information on household finances, to get a better understanding of which sources of information a household is using to make financial decisions. There are a number of potential options to select for the SCF question. We focus on three general responses for this piece: financial advisor (which is technically aggregated from “banker,” “broker,” and “financial planner”), the internet/online service, friend (which is both “call around” and “friends/relative”), etc.

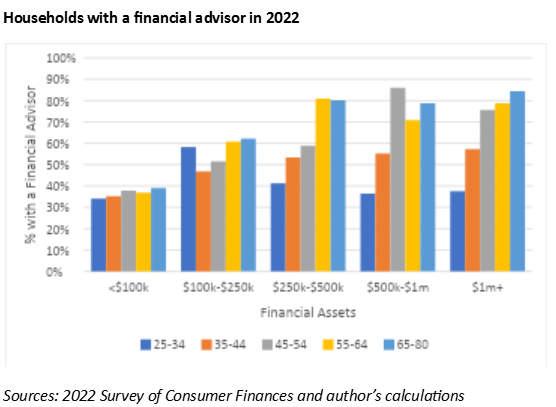

First, in the figure below, we include information about what percentage of U.S. households note working with a financial advisor in 2022 by respondent age and total household financial assets. Note that the household is assumed to be working with an advisor if the source is noted at all (i.e., it doesn’t have to be the first source provided in the question response).

There is a clear trend where households who are older with higher assets are much more likely to be working with a financial advisor. For example, only about 35% of households with financial assets under $100,000 work with a financial advisor (although there is a slight positive trend by age). In contrast, while only 38% of respondents between the ages of 25-34 with $1 million or more in financial assets not using a financial advisor, and 82% of those between the ages of 65-80 with same level of assets do.

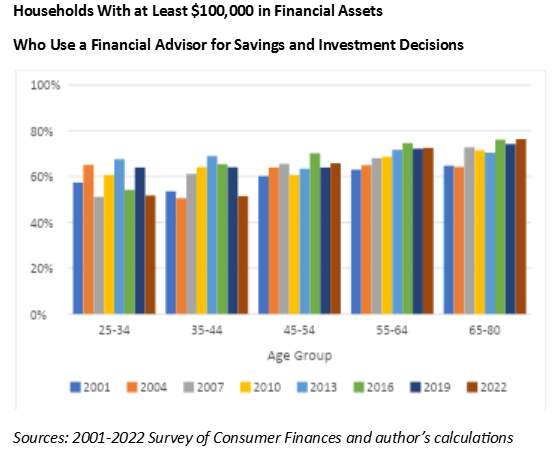

There has been little change in utilization of a financial advisor when it comes to making savings and investment decisions over the last two decades. This effect is demonstrated in the next exhibit, which includes households who note using a financial advisor with at least $100,000 in financial assets (in 2022 dollars).

We can see that while there has been a slight positive trend at older ages (i.e., those age 55 and over), there has been no real change among younger households, and the increases are relatively minor.

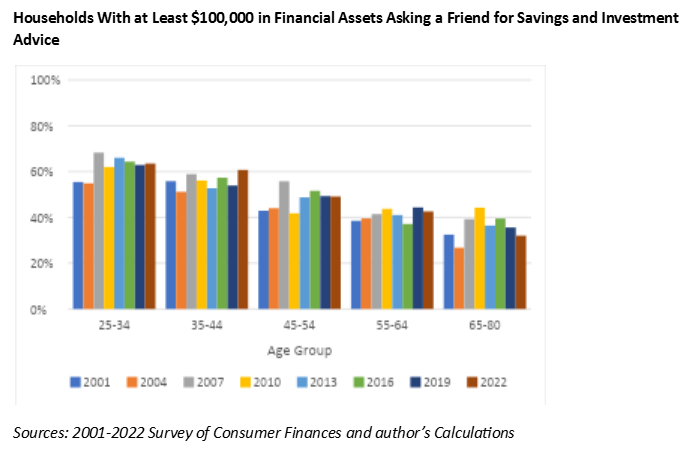

There has also been relatively little change in households using informal sources (e.g., friends) when it comes to making financial decisions. The next figure includes households with at least $100,000 in financial assets (in 2022 dollars) who note asking a friend when making financial decisions.

While not much has changed over time, there is a clear difference by age; for example, approximately 60% of respondents age 25-34 note using a friend versus only approximately 35% among those 65-80. More formal sources (i.e., financial advisors) appear to become prominent among older ages. This is probably a smart decision, as financial advisors should be more informed about financial matters.

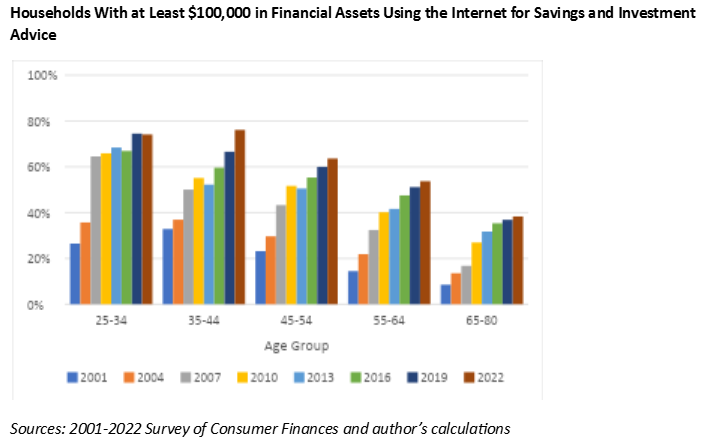

One notable shift in financial resources is the use of the internet or online solutions for savings and investment decisions, as noted in the following figure.

We can see a significant shift in the use of the internet and online services over the last two decades. For example, the percentage of 25-34-year-olds who note using the internet or an online service for savings and investment decisions with over $100,000 in financial assets (in 2022 dollars) increased from 27% in 2001 to 74% in 2022. For 65-80-year-olds, the increase was from 9% to 38%.

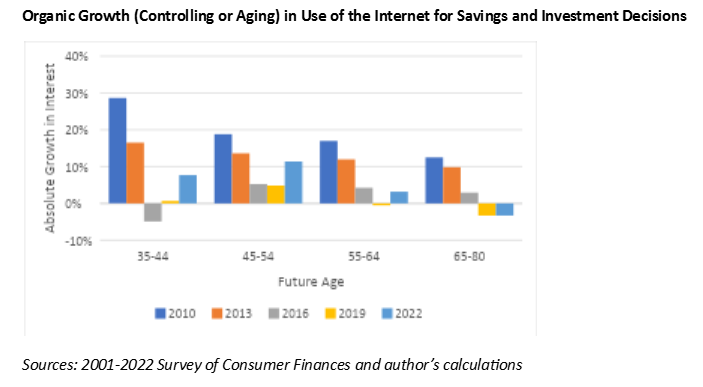

This is a pretty staggering increase over the period. While part of the shift could be due to aging – since someone in the 2001 wave would be 41 years old by the 2022 wave (note the data is cross-sectional – it’s not the same people included in each survey over time), we can demonstrate that aging does not describe the entire increase in the use of the internet in the next figure.

For this analysis, we subtract the percentage of people who note using the internet or an online service at a given age and the SCF survey from those who are 10 years younger for the survey nine years prior. While there is a slight mismatch in the periods, it provides some perspective on how adoption is changing beyond simply aging.

For example, 26% of respondents age 25-34 were using the internet in 2001. Fast-forward to the 2010 wave, approximately a decade later, and usage of the internet for 35-44-year-olds is 55%. We could expect at least approximately 26% of 35-44-year-olds to be using the internet a decade later, since they were using the internet the previous decade. This approach gives us some perspective on the organic growth rate over time.

While the organic growth adoption of the internet is slowing, part of this effect could be simply because of the large number of individuals who have already adopted it. For example, as noted previously, 74% of respondents from the age of 25-34 were using the internet by 2022, and 63% of respondents from the age of 45-54 were doing so. The wide adoption suggests that while organic growth may be slowing, the internet has become relatively pervasive. Among the demographic groups, though, those from 45-54 have seen the largest growth, with an organic growth rate of approximately 10% over each period.

Where Can Digital Work?

While the internet is becoming an increasingly common source for households in making financial decisions, the overall growth of digital advice solutions (i.e., robo-advisors) has not met many of the early forecasts made when they were introduced (e.g., since Betterment was launched in 2010).

Customer acquisition can be difficult for retail-focused robo-advisors, and balances for many of the existing robos are relatively small. For example, the average balance2 at Betterment is only approximately $44,000 versus approximately $70,000 for Wealthfront. A 2023 Morningstar report3 notes that the median robo-advisory fee is around 25 basis points (for a $15,000 balance, which excludes the investment expenses).

The DC workplace market seems like an ideal environment for digital solutions to continue to grow. DC-focused digital solutions – typically referred to as managed accounts – have been available for over two decades, and assets in these solutions exceed $400 billion. The DC environment seems well-suited for digital solutions because balances tend to be well below the threshold that would generally be considered attractive for a human financial advisor. For example, the median 401(k) balance at Vanguard (2024)4 as of December 31, 2023, was $35,286. While the average balance was notably higher – $134,128 – 28% of participants had a balance of less than $10,000 versus only 15% who had balances above $250,000.

In other words, while some DC participants have relatively significant balances (which skews the average balance), the average worker (i.e., the median) has a balance that is quite small, especially given typical thresholds required for more comprehensive financial advisors. For example, a 25 basis point fee (average robo fee) on a $40,000 balance (approximate median 401(k) balance) only yields revenue of approximately $100 per year, which is less than half the median hourly rate for a flat-fee financial planner ($220).5

With a median DC participant tenure of seven years, according to the Morningstar report, it will be difficult for workers to accumulate balances in employer-sponsored DC plans unless they roll over existing savings in the DC plan. Additionally, it will be relatively expensive to deliver any type of human advice to participants at scale; therefore, digital advice solutions may provide a missing link to enable participants access to quality financial advice at an attractive price point.

Conclusions

The resources investors use to make financial decisions are evolving. While financial advisors still appear to be a trusted source, especially among wealthier and older Americans, the internet and online services are becoming increasingly prevalent. There are several ways increasing familiarity and comfort with online solutions could play out, in which human advisors still serve as the primary source (for those with enough assets to afford one), while internet-based solutions (and information sources) serve as a “second opinion.” Regardless, awareness of the changes in consumer preferences is important, especially to the extent the tools can be made available to households in a cost-efficient manner to potentially improve retirement outcomes.

David Blanchett, PhD, CFA, CFP® is Managing Director, Portfolio Manager and Head of Retirement Research at PGIM DC Solutions.

1 https://www.federalreserve.gov/econres/scfindex.htm

2 https://www.forbes.com/advisor/investing/top-robo-advisors-by-aum/, Accessed July 19, 2024

3 https://www.morningstar.com/lp/robo-advisor-landscape, Accessed July 20, 2024

4 “How America Saves” 2024. https://institutional.vanguard.com/insights-and-research/report/how-america-saves.html, Accessed July 20, 2024

5 https://www.kitces.com/blog/average-financial-plan-fee-hourly-retainer-aum-plan-cost/, Accessed July 19, 2025

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All