Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

ETFs have always been a useful tool to play momentum and reversal in markets. However, the biggest question is always when to enter and exit such specific ETFs as the markets move through their cycles.

We decided to take a look at markets over the past 50 years and see how reversal and momentum in markets relates to macro events. This exercise is done to see the macro-level determinants of reversal and momentum and to gauge when it is best to move in and out of such positions.

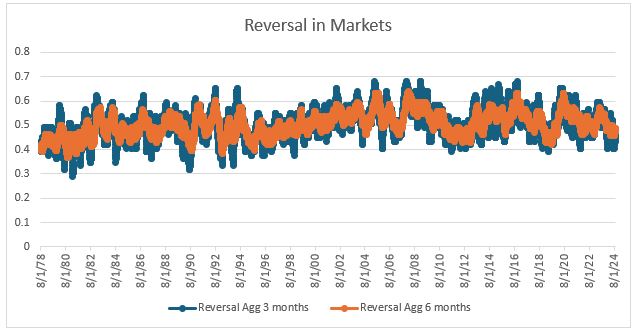

To implement this study we looked at the S&P 500 on a daily basis. We then looked at a three-month rolling average and six-month rolling average and calculated the percentage of days where the market is in reversal, positive momentum, and negative momentum. We then graphed this over time to see big outlier events on either end.

The first interesting finding relates to reversal in markets. The big takeaway on the determinants of reversal in markets is that we see spikes during periods of high uncertainty (high Cboe Global Markets Volatility Index, or VIX). We see spikes around summer 2008 and 1992, when we saw a quick recession. We also see low points in reversal when there are big secular trends in markets: 1980 to 1981 (inflation), 1990, and 1994.

Overall, we note that periods of reversal coincide when uncertainty of uncertainty is high, meaning when the Cboe Global Markets VIX of VIX (VVIX) is spiking – the index captures the volatility of the VIX, i.e. the the uncertainty around expectations of the VIX going forward. During those times, the market cannot accurately assess what is going on and when the market is shifting out of its momentum direction. There are ETFs out there to play such a strategy – see the Vesper U.S. Large Cap Short-Term Reversal Strategy ETF (UTRN) for one example.

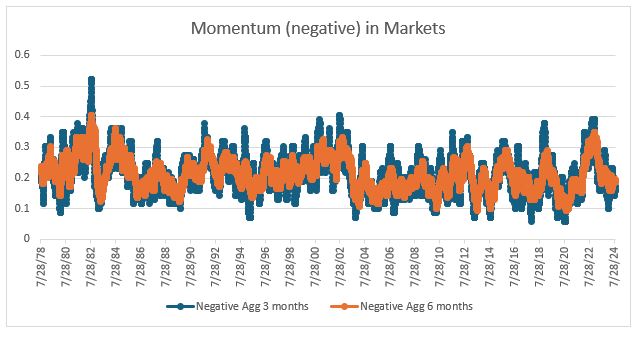

Next, we took a similar look at momentum – both negative and positive – in markets. The first interesting finding here is that negative momentum spikes when a bubble has burst (not surprisingly). We see peak negative momentum during 1981-1982, when inflation takes hold, and during 2000-2002, when the internet bubble slowly deflates.

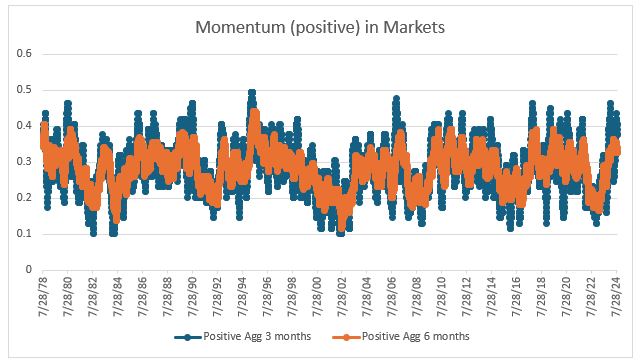

Following this, we look at positive momentum. Again, not surprisingly, positive momentum spikes when the market is in a period of exuberance. 2006 is a peak period, before the housing bubble hits, as is summer 2024, when the AI boom is taking off. There are several ETFs out there to play this phenomenon. They include the Vanguard U.S. Momentum Factor ETF (VFMO) and the iShares MSCI USA Momentum Factor ETF (MTUM), just to name two very popular ones.

All in all, instruments that track the VVIX or the VIX may be helpful in identifying the reversal in markets. The standard idea of exuberance being the main identifier of momentum in markets seems to hold true.

Derek Horstmeyer is a Professor of Finance at George Mason University's Costello College of Business.

Ruben Devia is a Financial Advisor with Fellows Financial Group and an alumni of George Mason University, where he obtained a Bachelor’s degree in Finance in 2014. He helps his clients by putting comprehensive plans together regardless of where they are in life. In his free time, he enjoys doing investment research as well as doing pro bono work for people in the community.

David Peters is a senior at George Mason University, set to graduate this May with a Bachelor’s degree in Finance. Driven by a deep passion for learning, David has developed a strong interest in understanding the complexities of the finance world and how financial strategies can be leveraged to improve individuals' lives. Throughout his academic journey, he has honed his skills in financial analysis, strategic planning, and problem-solving. David is committed to exploring innovative solutions in finance as he seeks to apply his knowledge and skills to create positive, real-world impacts for individuals and businesses alike.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Read more articles by Derek Horstmeyer, David Peters, Ruben Devia