Bifurcated Advancements in 401(k) Investments

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

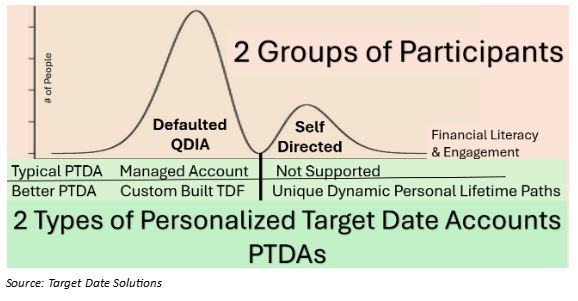

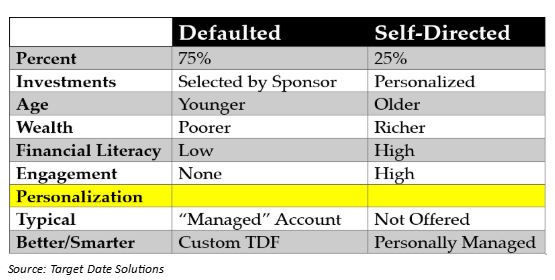

There are two distinct groups of 401(k) participants. The majority (75%) do not make an investment election, so they default their investment choice to their employer, who chooses an appropriate Qualified Default Investment Alternative (QDIA) on their behalf. Most of these defaulted participants (85%) are invested in target date funds (TDFs).

The remaining 25% of participants self-direct their retirement savings; they manage their retirement investments. The following table summarizes the two distinct groups and the two different approaches for personalizing their investments:

Improvements for both groups have been introduced, but they are not yet mainstream. Personalized target date accounts (PTDAs) are the new best thing in 401(k) investing, but there are two distinct kinds of PTDAs to be aware of. In the following, I separately discuss each type of PTDA used as a QDIA – managed account and target date fund – and then I discuss PTDAs for self-directed participants, which is not a QDIA.

Typical PTDAs are “managed” account QDIAs, but they’re not actually managed

Most newly introduced PTDAs are sold as individualized managed account QDIAs, so they need to address the challenge of making decisions for people who do not want to engage. Because you really don’t know what these people need and want, this flavor of managed account is not actually managed. According to Investopedia an account is “managed” when:

Armed with discretionary authority over the account, the dedicated manager actively makes investment decisions pertinent to the individual, considering the client's needs and goals, risk tolerance, and asset size.

Managers of these PTDAs do not know the client's needs and goals, risk tolerance, and asset size, because a defaulted participant does not engage. These managers guess risk preference based on an estimate of asset size alone, derived from recordkeeper data. There is no assessment of needs, goals or risk tolerance – just wealth.

Even if wealth were enough to determine risk preference – which it isn’t – recordkeeper data says very little about participant wealth, because the median tenure of participants is less than five years, and even less for those most likely to be defaulted into participation – workers under age 35. These PTDAs make bad guesses in order to “manage” this QDIA.

And then there’s the assumption that rich people can afford more risk, versus the counter argument that poor people need more risk because they have not saved enough. Which is correct?

Smarter PTDAs are used to build custom target date fund QDIAs

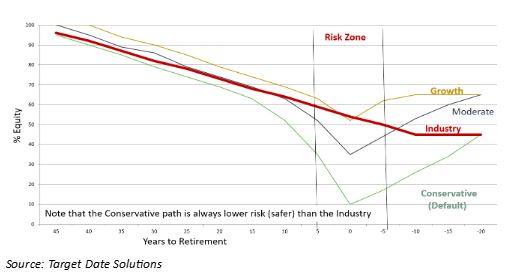

A more practical approach is to use the PTDA structure to give the 401(k) sponsor great flexibility in designing a unique custom target date fund (TDF) QDIA for all. This would conform to DOL guidance to match the TDF glidepath to the demographics of the workforce. Specifically, the sponsor chooses the appropriate risk for the QDIA by blending Conservative-Moderate-Growth glidepaths like those shown in the following:

The sponsor uses the PTDA structure to custom build a one-size-fits-all-set-it-and-forget-it target date fund QDIA for all defaulted participants. Academic lifetime investment theory argues for the very safe Conservative path in the exhibit. But current common practice (“Industry” in the exhibit) is much riskier, even though providers say they follow the theory.

The Industry is not following the theory, but the next market crash should change that, because it will wake up investors to the risk they’re taking. There has been little risk in the past 16 years – the longest bull market ever.

The U shape in the above glidepaths is unique. It’s designed, first, to manage sequence of return risk near retirement, and second, to extend the life of assets in retirement by re-risking, following the guidance of Kitces and Pfau.

The other choice – in addition to risk – is the retirement date that is recognized as the actual day, rather than grouping the participant into 5-year or 10-year age bands.

In summary, 75% of participants who default can benefit from judicious employer use of PTDAs to customize a glidepath that best serves the demographics of the plan.

Dynamic glidepaths for self-directed participants

Self-directed (SD) participants want to engage, and many like TDFs. About a third of the assets in TDFs are from self-directed participants, but they are limited to the one TDF that is on their platform. Note that this usage is not a QDIA, because these participants have not defaulted. TDFs are not a QDIA when they’re affirmatively selected by non-defaulted participants.

Unlike typical PTDAs that are not offered to self-directed participants, better and smarter PTDAs welcome their usage. These better PTDAs give SDs lots of flexibility in managing their retirement savings. Life brings surprises that can change individual risk preferences through time. SD use of PTDAs allows for changes in risk anytime. SDs “manage” their own unique personalized lifetime investment path; each path is unique to the self-directed participant.

As stated above, the retirement date is recognized as the actual day, rather than grouping the participant into 5-year or 10-year age bands. This can also be changed by SDs at will. The system can be “tricked” by choosing a later or earlier date than actually anticipated. Earlier increases safety and later increases risk.

Better investments for all in better and smarter PTDAs

Importantly, the investments used in better and smarter PTDAs are intended to be the best in each asset class, rather than limited to the proprietary funds of a particular investment manager, as is the case with most off-the-shelf TDFs. A common complaint about TDFs is that the underlying management is all proprietary, so you pay a fund company to hire itself as an asset manager in addition to the costs associated with relying on its glidepath. PTDAs can be less expensive than TDFs.

Partners in better and smarter PTDAs

Recordkeepers and investment advisors play key roles in structuring and implementing better and smarter PTDAs. Investment advisors select the underlying managers and help customize the QDIA. Recordkeepers collect participant decisions and rebalance accordingly. PTDAs are great opportunities for recordkeepers and advisors.

Conclusion

Finally, an innovation has arrived in 401(k) investing. PTDAs are new. They combine multiple target date glidepaths with managed accounts, potentially using the best of both. Because they are new, it will be easy to think of them all as being the same, but that is far from the truth. PTDAs vary widely because there is no standard.

401(k) participants need PTDAs because investing is personal, so they should request them. Fiduciaries should perform serious due diligence and choose the best PTDA, recognizing the important distinction between PTDAs as managed account QDIAs versus PTDAs used to build custom target date fund QDIAs. Also, some PTDAs are exclusively for defaulted participants, while others are for all participants.

Ron Surz is president of Target Date Solutions, developer of the patented Safe Landing Glide Path and Soteria personalized target date accounts. He is also co-host of the Baby Boomer Investing Show. Surz’s passion is helping his fellow baby boomers at this critical time in their lives when they are relying on their lifetime savings to support a retirement with dignity, so he wrote a book, “Baby Boomer Investing in the Perilous 2020s,” and he provides a financial educational curriculum.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All