Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

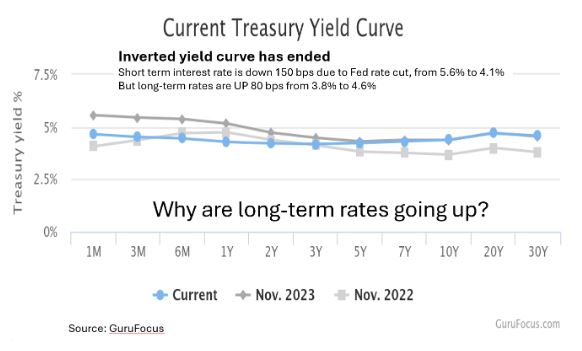

Most of the time the yield on long-term bonds exceeds that on short-term bonds, in order to compensate for the greater risk attached to long-term debt. But until recently the yield curve was inverted, with short-term rates exceeding long-term rates. This happens when investors expect interest rates to decline in the future.

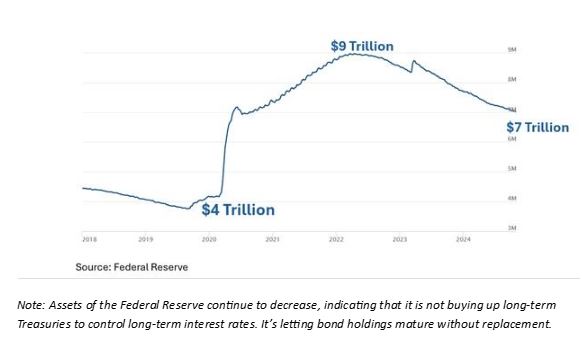

Until June 2022, the Fed had been using quantitative easing (QE) to stimulate the economy following COVID-19. QE was designed to keep interest rates low in a zero-interest rate policy (ZIRP). Accordingly, the Treasury issued short-term bills at a very low rate, and these cleared the market. But long-term bonds needed help to clear the market at low rates, so the Fed purchased most of the new-issue long-term bonds.

In this way, money was printed and the Fed’s balance sheet increased substantially. It grew to $9 trillion, up from $4 trillion – more than doubling. Printing money is inflationary and brought the inflation rate up to 9% in June 2022, at which time the Fed moved to quantitative tightening (QT) by raising interest rates. The Fed is an arsonist charged with fighting the inflation fire. As part of QT, the Fed allowed the bonds it holds to mature without replacement, so the $9 trillion became $7 trillion.

The Fed is an arsonist charged with fighting the inflation fire. As part of QT, the Fed allowed the bonds it holds to mature without replacement, so the $9 trillion became $7 trillion.

Then, in October of 2024, the Fed announced that QT was over, and lowered interest rates. So, short-term interest rates declined, which would have uninverted the yield curve on its own. But uninversion got a boost from rising long-term interest rates. That’s right – short-term rates have come down, but long-term rates have gone up. What just happened?