Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Private equity can play an important role in an investor’s portfolio, offering strong return potential, increased diversification, and expanded investment opportunity. But a key step to the success of these investments is selecting the right manager. Why? The potential for significant performance variability is far greater in the private markets than the public markets.

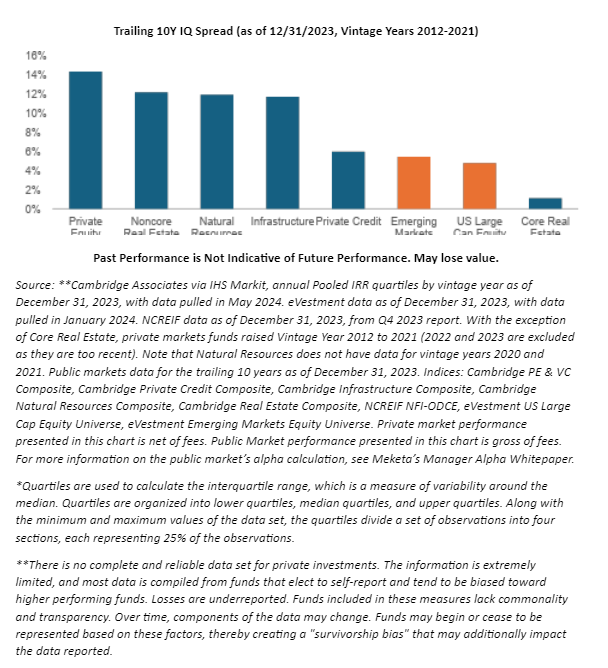

Historical data reveals a more than 14-percentage-point performance differential between the top-performing private equity managers and the bottom-performing managers over the past 10 years (see chart). For comparison, the performance difference for public large-cap stocks over the same period was 4.8 percentage points. Thus, performance dispersion is an important consideration when it comes to private investments and manager selection is critical.

What’s driving the performance dispersion in private equity?

The concept of performance dispersion refers to the range of returns achieved by different investments or investment managers over a specified period. It quantifies the gap between the best and worst performers, indicating the variability – or spread – of returns within a particular market or investment strategy. In the context of private equity investments, performance dispersion refers to the variability in returns across different private equity funds.

Historical data has shown that skilled active management can add more value in some asset classes than others. While performance dispersion in public equity funds tends to be relatively low due to the speed and transparency of available information which makes these markets highly efficient, that’s not the case in private markets. Private equity asset classes have historically exhibited higher performance dispersion as measured by interquartile spreads.*

While there are roughly 4,500 publicly traded companies in the U.S. today, the number of private companies is far larger – more than 30 million. Because the investable universe is much larger, and since these companies have less readily available financial and operational information, private equity is a less efficient asset class than public stocks. This means that skilled investment managers can potentially take advantage of the larger mispricing opportunities to add value.

Attributes of top-quartile performers

Top-performing managers typically share certain characteristics that contribute to their performance success:

-

Better deal sourcing. Unlike public markets, there are no perfect sources of information about private companies. Relationships and sources of deal flow become critical. An experienced manager with an extensive, developed network may have the ability to source, negotiate, and execute more attractive deals. As their experience and reputation grows, they typically can access and win the most attractive and competitive deals which, in turn, enhances their reputation further, creating a virtuous cycle.

-

More favorable entry valuations. Experienced managers who can negotiate favorable terms and lower entry valuations as they acquire companies often improve the risk/return profile of their investments. A lower entry point to purchase a high-conviction company likely results in higher return potential while limiting the potential for losses if the investment fails to meet expectations.

-

Potential for value creation. In many private equity investments, new management is brought in to grow or turn around a business. Managers who are skilled at growing or improving a business that then generates higher performance may add value relative to their peers. Skilled managers can potentially enhance portfolio companies by improving their operations, increasing margins, implementing growth strategies, and upgrading management personnel.

Advisors and their clients can invest indirectly through a private equity fund rather than direct investment in individual companies. These funds perform the manager due diligence and may in turn gain access to top-performing general partners to create an effective and convenient approach to private equity investing. Further, these private equity fund investments are often diversified across managers, styles, and geographies.

Manager selection drives performance

Advisors and their clients who seek to take advantage of the potential rewards of private equity investing should understand the performance dispersion between top- and bottom-performing managers, a factor that heightens both the risk and opportunity. Since private equity investments are designed to be long-term investments where capital can be locked up for years, getting the manager selection wrong can be a vexing obstacle to success.

Top-performing managers typically have skill in distinguishing better investments. They get preferred access to deals and preferential terms in investments. And they may have the ability and resources to add value after the investment. Careful diligence of managers is important when pursuing the potential benefits of private equity investing.

Michael Bell is the CEO of Meketa Capital.

This document is for general information and educational purposes only, and must not be considered investment advice or a recommendation that the reader is to engage in, or refrain from taking, a particular investment-related course of action. Any such advice or recommendation must be tailored to your situation and objectives. You should consult all available information, investment, legal, tax, and accounting professionals, before making or executing any investment strategy. You must exercise your own independent judgment when making any investment decision.

All information contained in this document is provided “as is,” without any representations or warranties of any kind. We disclaim all express and implied warranties including those with respect to accuracy, completeness, timeliness, or fitness for a particular purpose.

We assume no responsibility for any losses, whether direct, indirect, special, or consequential, which arise out of the use of this article. All investments involve risk. There can be no guarantee that the strategies, tactics, and methods discussed in this document will be successful.

Data contained in this document may be obtained from a variety of sources and may be subject to change. We disclaim any and all liability for such data, including without limitation, any express or implied representations or warranties for information or errors contained in, or omissions from, the information. We shall not be liable for any loss or liability suffered by you resulting from the provision to you of such data or your use or reliance in any way thereon.

Nothing in this document should be interpreted to state or imply that past results are an indication of future performance. Investing involves substantial risk. It is highly unlikely that the past will repeat itself. Selecting an advisor, fund, or strategy based solely on past returns is a poor investment strategy. Past performance does not guarantee future results.

Meketa Capital is an investment advisor registered with the U.S. Securities and Exchange Commission

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Read more articles by Michael Bell

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.