Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

The Government Accountability Office (GAO) recently released the following 2 reports:

The report on target date fund risk merely rubber-stamps current industry practices that are far too risky for those near retirement, so it’s a big disappointment. But the exposure of conflicts of interest in the most recent report is applaudable. Here are quick overviews.

Target date fund risk

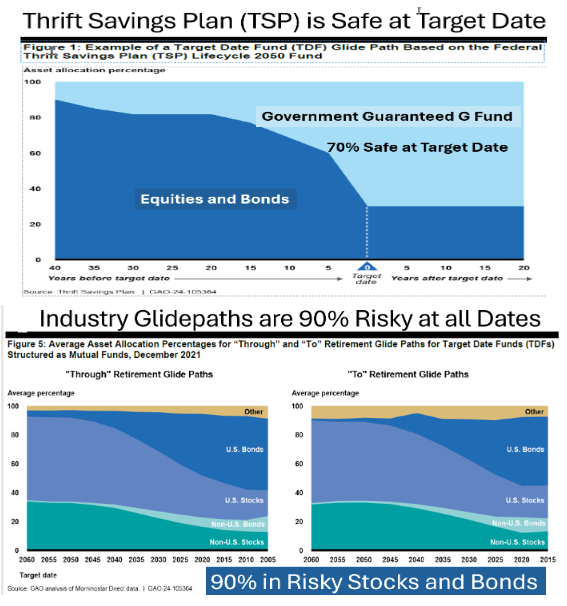

GAO contrasts the risk of the Federal Thrift Savings Plan (TSP) to that of the TDF industry, as shown in the following two graphs. TDFs say they follow academic lifetime investment theory, but most do not follow the theory, as explained in this article. The theory is 80% risk-free at the target date, but the industry is 90% risky throughout (at all ages) in risky equities and long-term bonds.

The TSP does follow the theory. It is very safe at the target date with 70% in the risk-free G fund guaranteed against loss by the U.S. government. However, the industry does not.

Regulators should know that academic theory is very safe for those near retirement, and they should demand the industry explain their claim of following the theory. This departure from theory has been rewarded for the past 15 years because U.S. stocks have enjoyed their longest bull market ever, but that will change. High risk will suffer high loss in the next stock market crash – that’s the nature of risk.

Conflicts of interest are to blame for excessive risk near the target date. Some say that participants don’t know what they need or even want, and that they need high risk because they have not saved enough. But surveys of participants show that they do know, and they want to be protected near retirement. Unfortunately, they are not.

The “industry best practices” that fiduciaries follow have come to mean common practices. But what if common practice can and should be improved? Procedural prudence is not necessarily substantive prudence. Shouldn’t we do better if we can? Oligopolies stifle innovation and create conflicts of interest.

There are conflicts of interests between participants, advisors, and investment managers that are discussed in the recent GAO report.

Conflicts of interest

In the following table, GAO recommends that advisors and investment managers openly address their conflicts.

There are three interest groups in TDFs. Investment managers create TDFs for profit, which is, after all, their business. Fiduciaries choose TDFs, presumably for the benefit of participants, but that’s not what is happening. Beneficiaries want to be protected, especially as they enter retirement, but they are actually exposed to substantial risk.

At the very least, investment managers need to acknowledge that they exclusively use proprietary funds in their TDFs, and that it is unlikely that those funds are the best in every asset class. Fiduciaries – namely advisors – need to recognize they are conflicted between procedural prudence and substantive prudence. Procedural prudence mandates usage of the Big 3 oligopoly. Substantive prudence argues for protecting participants near retirement.

Conclusion

GAO reports are intended to improve industry practices. GAO failed in its target date fund report but succeeded in its conflicts of interest report. What do you think?

Ron Surz is president of Target Date Solutions, developer of the patented Safe Landing Glide Path and Soteria personalized target date accounts. He is also co-host of the Baby Boomer Investing Show. Surz’s passion is helping his fellow baby boomers at this critical time in their lives when they are relying on their lifetime savings to support a retirement with dignity, so he wrote a book, “Baby Boomer Investing in the Perilous 2020s,” and he provides a financial educational curriculum.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Read more articles by Ron Surz

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.