In the more than 20 years I’ve been a financial planner, I’ve found that many decisions revolve around the solution of 50 percent. This 50 percent rule is more a guideline than a requirement. But although I often vary from it, I don’t typically stray too far from the magic 50 percent. Here are five decisions where I use this rule.

In the more than 20 years I’ve been a financial planner, I’ve found that many decisions revolve around the solution of 50 percent. This 50 percent rule is more a guideline than a requirement. But although I often vary from it, I don’t typically stray too far from the magic 50 percent. Here are five decisions where I use this rule.

Asset allocation

What percentage of the portfolio should be in risky assets such as stocks? It, of course, is a decision based on the client’s willingness and, especially, need to take risk. I’ve had clients with percentages as low as 30 percent and as high as 90 percent. I happen to be a bit under 50 percent as my need to take risk is low.

The late Harry Markowitz was the Father of Modern Portfolio Theory (MPT), which uses concepts such as correlation, risk, and return to find the optimal portfolio weightings. What was his optimal allocation?

“I split my contributions 50/50 between bonds and equities,” he said.

Markowitz readily admitted that he did not compute co-variances and draw a mean-variance efficient frontier. He stated “my intention was to minimize my future regret. So I split my contributions 50/50 between bonds and equities.” That was back in 1952, and I don’t know whether or not he maintained that ratio.

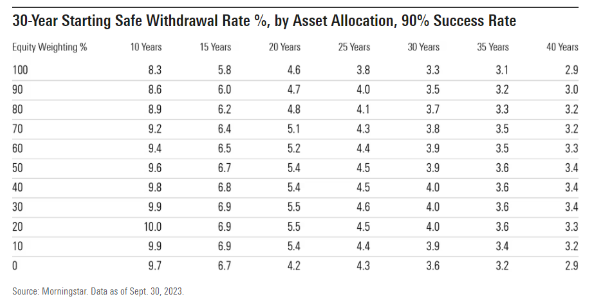

I find myself gravitating to the 50 percent stock recommendation for clients who are at or near retirement. That recommendation is about more than minimizing regret – it’s mainly to maximize a safe spend rate in retirement. Below are Morningstar’s calculations of safe spend rates, depending on both the equity allocation and the number of years the portfolio must last.

Note that for portfolios that need to survive between 25 and 40 years, the maximum safe spend rate tends to gravitate toward a 50 percent equity portfolio. Having too much in equities could lead to failure in a sustained bear market. On the other hand, having too little (or too much in bonds) could lead to failure due to the possibility of high or even hyperinflation. Thus the 50 percent stock allocation often produces the optimal safe withdrawal rate.

A final reason I often recommend a balanced portfolio is it has maximized the return from rebalancing. Morningstar’s latest Mind The Gap research shows that investors chase performance. Investors are predictably irrational, and I believe rebalancing adds to return in the long-run as it did during the 33 days when stocks lost 35 percent in 2020 as the pandemic hit. Portfolios with either very low or high concentrations in equities didn’t have as much to rebalance. The 50 percent stock portfolio allows for more dollars to rebalance by buying low and selling high when the herd is doing the opposite.

Concentrated stock positions

I often have clients come to me with concentrated stock positions. It’s typically due to their employer granting restricted stock units (RSUs) or similar incentive compensation plans. Occasionally, it’s something like owning Nvidia for years.

Typically, I recommend selling RSUs when they vest in order to diversify since the tax implications occur at vesting. But I have clients who come to me with millions of dollars of vested RSUs with huge unrealized gains. I typically sort the vested lots from the lowest to the highest percentage tax consequences. In doing so, I take into account both short-term vs. long-term and the clients’ marginal tax rates to develop a plan to diversify.

I often end up with a recommendation to sell about half. It can sometimes result in the sale of 50 percent of the value but only a third or less of the unrealized gains if you select the lots with the smallest tax consequences to sell. Not only does this minimize regret, it also provides the client an emotionally appealing option. If the stock underperforms, they can feel great about selling half. If the stock continues to soar, they can blame it on me and be glad they kept half (and likely get future RSU vesting).

Selling expensive funds

When clients come to me with narrower and more expensive funds in a tax-deferred or tax-free account, I recommend selling all of these funds as there are no tax consequences. But often clients have owned these funds for many years or even decades and have large unrealized gains. Do we pull the band-aid off or suffer the slow bleed of paying higher fees for many more years?

The answer depends on many factors from current and future tax rates to just how bad these expensive funds are and what is needed to develop a more balanced portfolio. Sometimes there are solutions such as gifting to an adult child who could sell at the zero percent Federal long-term capital gains rate, or donating to a donor-advised fund if the client has the charitable intent.

Typically, I sort the funds from the lowest to the highest percentage gains and note their expense ratios. Then I have the discussion with the client to decide on a plan to sell. Some gains can be so large that, paired with the client’s life expectancy, they’re likely better to keep with the hope the step-up basis will remain. But some will warrant ripping the band-aid off, while others will warrant selling over time. For any funds not sold, turn off the dividend reinvestments so the client is buying more. Often, we keep about half and sell the other half.

Traditional versus Roth

Should the client convert a more traditional IRA (or other tax-deferred money) to a Roth? There are seven factors I consider when recommending a Roth conversion. I point out that the ultimate answer will only be known later on in life when one sees what their marginal tax rate on money being withdrawn to live on will be.

For the most part, if tax rates are higher in retirement, the conversion will have been a good thing. If rates are lower, the conversion will not have been optimal. If the marginal tax rates are the same, it’s a breakeven (though paying the taxes from a taxable account slightly favors the conversion even at the same marginal tax rates).

What will happen to future tax rates? Logic says they must go up to fund interest on our mushrooming debt, but logic and politics don’t have much in common. Even if Congress hikes tax rates, the client’s marginal rate might be lower when they have no earned income.

So, I’m often developing a plan with conversions to get the portfolio to be 50 percent tax-deferred traditional and 50 percent tax-free Roth, though it may take many years to get there. I call this tax-diversification or diversifying from what Congress may do to tax rates.

Dollar cost averaging (DCA) versus lump sum

Sometimes a client has a big windfall such as selling their company or inheriting a large amount of money. The plan I develop typically has lower percentage of their portfolio in equities than before the windfall but far more in terms of total dollars. Mathematically, the solution is simple: They should get to the target allocation immediately, as it maximizes the risk-adjusted return. But as Harry Markowitz illustrated, we are not mathematical animals. Though he may have been one of the most quantitative beings on the planet, he acknowledged his emotional side.

For example, a client who sold her business – after a couple of decades of pouring her heart and soul into making it a success – would feel immense pain if she poured $10 million of the proceeds into equities only to see the worst day or year in the history of the stock market. This client is not likely to stay and very unlikely to rebalance. But DCA could even increase risk. If a client invests monthly over a three-year period where the market goes up over those three years only to see the plunge right after being fully invested, she could end up with less money than if it was invested all at once.

So after having this discussion, I often recommend to the client that, you guessed it, they invest half now and the remaining half using DCA.

Summing up the 50 percent rule

Rules are made to be broken, so I would call this a 50 percent starting place in your discussion with the client. I certainly wouldn’t recommend only a 50 percent equity portfolio to a young client with a high willingness and need to take risk or the same to any client who had a low willingness and need to take risk.

And sometimes gains and taxes are low enough to sell all concentrated positions and expensive funds. I could go on and on as to when I significantly vary from these 50 percent guideline decisions. But nonbinary decisions (meaning decisions that are not all or nothing) provide far more than emotionally optimal choices. Often, they result in the optimal safe-withdrawal rates and tax-diversification.

Allan Roth is the founder of Wealth Logic, LLC, a Colorado-based fee-only registered investment advisory firm. He has been working in the investment world of corporate finance for over 25 years. Allan has served as corporate finance officer of two multibillion-dollar companies and has consulted with many others while at McKinsey & Company.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Read more articles by Allan Roth

In the more than 20 years I’ve been a financial planner, I’ve found that many decisions revolve around the solution of 50 percent. This 50 percent rule is more a guideline than a requirement. But although I often vary from it, I don’t typically stray too far from the magic 50 percent. Here are five decisions where I use this rule.

In the more than 20 years I’ve been a financial planner, I’ve found that many decisions revolve around the solution of 50 percent. This 50 percent rule is more a guideline than a requirement. But although I often vary from it, I don’t typically stray too far from the magic 50 percent. Here are five decisions where I use this rule.