Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

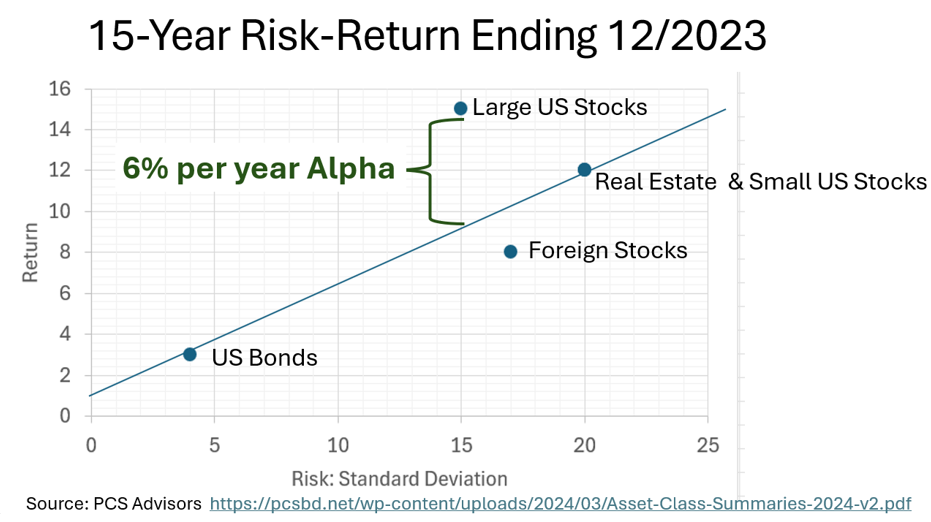

I once attended a meeting that included Harry Markowitz, father of Modern Portfolio Theory (MPT). The meeting set return and risk asset class expectations for the purpose of establishing an efficient frontier forecast. To initiate the discussion, the investment company showed the committee a risk-return X-Y graph of its expectations. Harry got up and drew an eyeballed line of best fit through the dots and directed a conversation to justify the assets that fell above (why the expected premium) and those that fell below (why the expected underperformance).

That line represents roughly equal return/risk Sharpe ratios, so equal returns per unit of risk. Distances above the line are forecasts of alpha, and those below are forecasted to return below average for their risk (negative alpha).

We all know that the past 15 years have been extraordinary for US stocks. It’s the longest bull market ever. The following graph shows how good. The 15-year alpha is a whopping six percent per year!! Large-cap US stocks have returned six percent more on average every year than the Capital Market Line of constant return per risk.

Over this 15-year period, the average return per unit of risk was 0.75 percent. Large-cap US stocks earned one percent per unit of risk – a 15 percent per year return for a standard deviation of 15. That’s a whopping 33 percent premium.

Why?

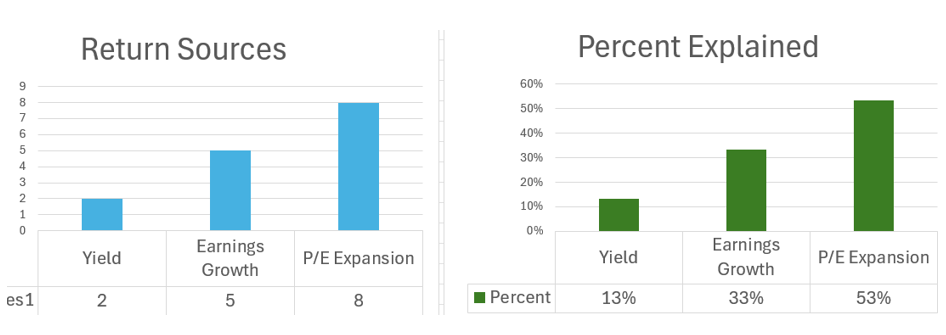

The question isn’t if large-cap US stocks outperformed. It’s why they outperformed for so long and by so much. Here’s a way to break down the answer to that question. The return formula is as follows:

Return = Dividend Yield + (1 + Earnings Growth) X (1 + P/E expansion/contraction) – 1

Here are the components of return for large-cap US stocks:

Most (52 percent) of the extraordinary return is explained by P/E expansion, which is the human behavior factor. Investors have been willing to pay increasing prices over time per dollar of corporate earnings, with P/Es increasing eight percent per year to the current 35, from 12 at the beginning of the period in 2009.

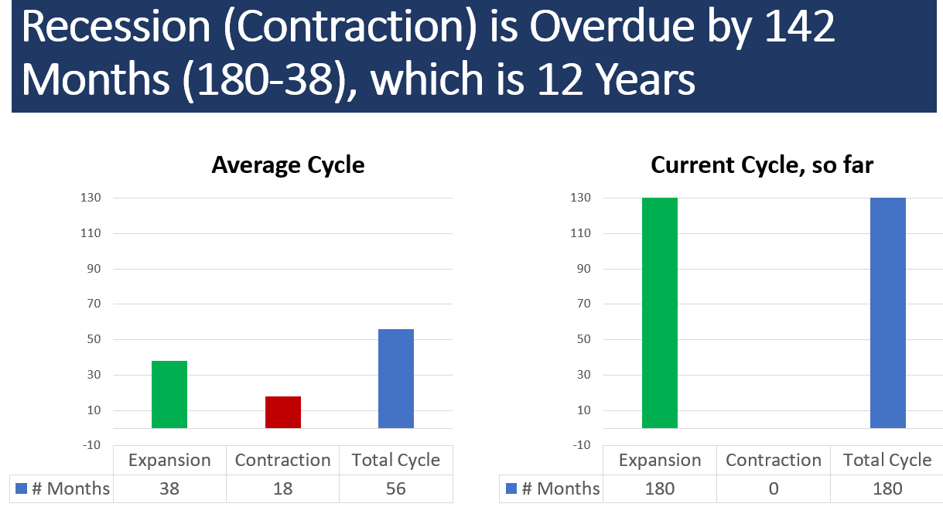

Greed is the answer to the question. The other human factor is fear. Fear will kick in sometime. Stock markets crash. They usually do every three years, so this 15-year period is a big exception. The contraction is 12 years overdue.

Conclusion

It’s been an extraordinarily great 15 years for large-cap US stocks. Can the party continue? History tells us that something will give, and there’s a name for its end. It’s called a Minsky Moment, which is a sudden and catastrophic collapse of asset prices named after economist Hyman Minsky.

I know you will say that I’m forecasting a crash and that no one can do that, and you’ll disagree, arguing for “staying the course.” However, human behavior is the reason that stock prices are so high. We have agreed to pay very high prices, introducing the “greater fool” who is someone who will pay even higher prices.

We will run out of greater fools. No one knows when, but we suspect the supply is limited.

Baby boomers are in the greatest jeopardy because most of them are in the Retirement Risk Zone, when losses can ruin the rest of their lives due to Sequence of Return Risk. They likely won’t have time to recover from the next crash. Their loss is also their heirs’ loss. There’s $70 trillion in play. Baby boomers shouldn’t be greater fools.

Ron Surz is president of Target Date Solutions, developer of the patented Safe Landing Glide Path and Soteria personalized target date accounts. He is also co-host of the Baby Boomer Investing Show. Surz’s passion is helping his fellow baby boomers at this critical time in their lives when they are relying on their lifetime savings to support a retirement with dignity, so he wrote a book, “Baby Boomer Investing in the Perilous 2020s,” and he provides a financial educational curriculum.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our videos.

Read more articles by Ron Surz

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.