It’s official: In the 150 years that the longest, the most valuable 500 U.S. companies have been tracked, stocks have never been more concentrated than this year. According to Bryan Taylor, chief economist at Global Financial Data, as of June 30, 2024, the top 10 stocks had a market cap of $17.07 trillion, which represented 35.77% of the S&P 500. While these mega cap stocks have declined significantly over the past few weeks, they now actually comprise an even greater 36.19% of the S&P 500 as of August 5, 2024 intra-day.

It’s official: In the 150 years that the longest, the most valuable 500 U.S. companies have been tracked, stocks have never been more concentrated than this year. According to Bryan Taylor, chief economist at Global Financial Data, as of June 30, 2024, the top 10 stocks had a market cap of $17.07 trillion, which represented 35.77% of the S&P 500. While these mega cap stocks have declined significantly over the past few weeks, they now actually comprise an even greater 36.19% of the S&P 500 as of August 5, 2024 intra-day.

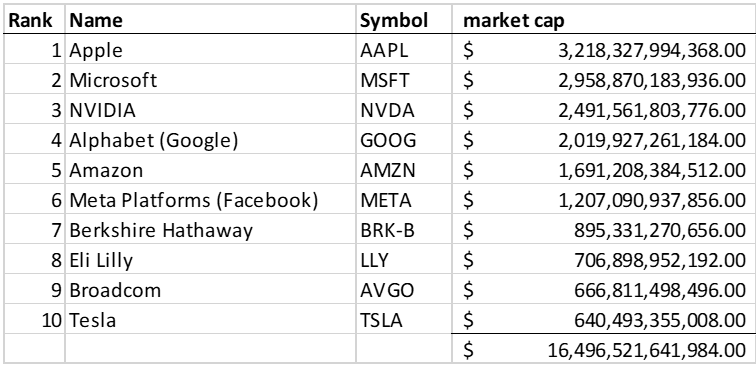

As of August 5, 2024, it’s $16.5 trillion as shown below from CompaniesMarketCap.com.

Is this the beginning of the inevitable bear, where these then-most-valuable stocks could get clobbered? Here’s what history teaches us about the current concentrated market and the current correction.

Of the 10 most valuable stocks, all but two are in what I consider to be heavily technology related, even though some (Amazon and Telsa) aren’t technically in the tech sector. And these 10 companies comprise nearly a third of the total market capitalization of all U.S. stocks. Each of the top three companies has capitalizations close to the combined value of the entire roster of Russell 2000 companies.

This concentration isn’t limited to the U.S. CompaniesMarketCap.com shows the top 10 companies comprising 17.4% of the 9,143 publicly held global stocks. Saudi Aramco and TSMC were the only non-U.S. companies on the list, and most of Saudi Aramco’s shares aren’t publicly traded.

Admittedly, data on the number of publicly held companies and market capitalization can be a bit ambiguous. Edward McQuarrie, professor emeritus at Santa Clara University, pointed out to me that there is judgment in deciding how many micro-cap companies -- such as those that might be on the pink sheets today -- should be included. He stated that different definitions of market capitalization exist such as only including free-floating shares or excluding warrants or in-the-money employee stock options. Elon Musk, for example, owns more than 20% of Tesla (TSLA). Rockefeller is believed to have owned an even larger share of Standard Oil.

Irrespective of what definitions are used, the stock market is now highly concentrated. The implications, of course, are that if these top stocks falter, it could be disastrous for portfolios. By my estimation, a 50% decline in the top 10 U.S. stocks would cause a 15.6% correction in the entire U.S. stock market. That’s if the other thousands of U.S. stocks had no decline at all, which would be virtually impossible.

Looking Back at History

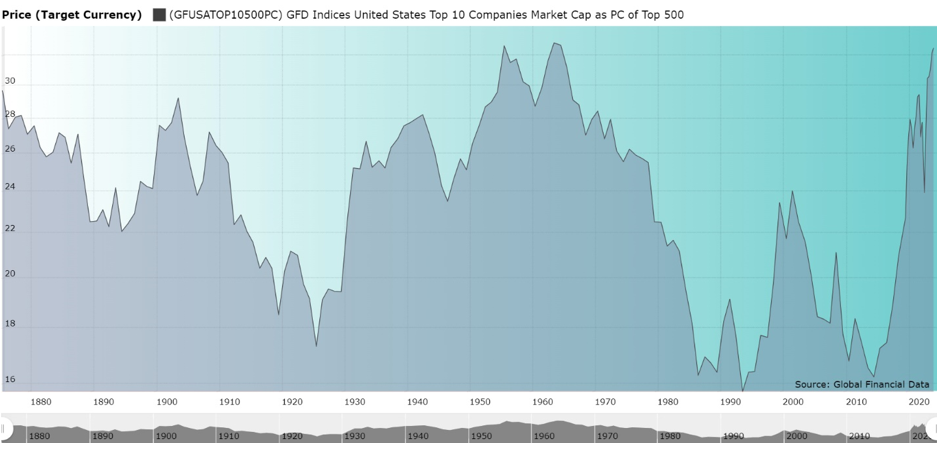

I noted that U.S. market concentration is higher than it’s been for at least the last 150 years. So I decided to take a look at what has happened in the past during periods of high market concentration. Several paths led me to Bryan Taylor’s research on 200 years of market concentration. Normally I’m skeptical of the accuracy of investment data that is more than a century old, but McQuarrie stated this was the best-researched data available. Taylor described the painstaking methodology of going back to newspaper articles of the day.

Taylor’s paper looked at the concentration of the 10 most valuable U.S. companies relative to the 500 most valuable companies since 1875. He started with that year because there were not 500 publicly listed companies before then.

Ten Most Valuable U.S. Stocks as a Percentage of the 500 Most Valuable (1875 – 2024)

You can see that, while the current concentration is a record, there have been other periods with high concentration.

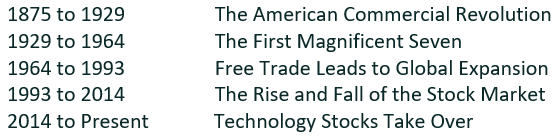

Prior to 1875, the U.S. stock market changed from being dominated by banks to the rise of railroads. And of particular interest, our current ”Magnificent Seven” isn’t the first. For 35 years, from 1929 to 1964, the market was dominated by AT&T, General Motors, IBM, Standard Oil, General Electric, Du Pont, and U.S. Steel. Yet market concentration stayed high after this period even though there was a shift in those 10 most valuable companies.

At the turn of the 21st century, the market was dominated by Microsoft, GE, and Cisco. Today’s market is dominated by the Magnificent Seven, of which Microsoft was the only one that maintained that domination. I found this video of the rise and fall of the most valuable companies in the world between 1998 and 2004 to be fascinating.

The chart below shows the change in the most valuable companies over a 40-year period. Not one of the then-most-valuable companies in 1980 stayed on the list. And some of the most valuable companies in 2020 and today didn’t exist back in 1980.

What This Means for Investors Today

The next area of analysis is to see what happened to both the stock market and those most valuable companies during periods of high market concentration. Taylor concluded that each period of high concentration occurred during a bull market and that decreasing concentration happened during a bear market. He also told me that, based on history, today’s 10 most valuable companies are likely to change dramatically over the next 40-50 years.

Should we reduce exposure to the current most valuable stocks? Should we at least overweight the nontechnology sectors? Taylor’s answer is “no” for both questions.

And while a dominant sector historically gives way to a new dominant sector, it can take many decades for that to happen. What sector will dominate? What are the right companies to buy now? Taylor, of course, responded that he doesn’t know. I asked him how he invests his own money, and he said he invests in a market-cap-weighted S&P 500 index fund.

One way often mentioned to reduce concentration risk is to buy an equal-weighted S&P 500 index fund. That way, Microsoft, Apple, and Nvidia combined only account for 0.6% of the fund, rather than more than 20%. But that is active investing, and extremely overweights the smallest companies in the S&P 500. These were often mentioned 10-15 years ago when small-cap value investing was the rage. They significantly underperformed.

Perhaps we should reduce overall stock exposure? Taylor points out that, though high concentration occurs during bull markets, it’s not predictive of a bear.

Conclusion

Though I’m quite concerned about the high concentration of a handful of stocks, that doesn’t mean I think I’m smarter than the market. Taylor’s work is fascinating. That said, I don’t agree with ignoring the thousands of stocks that aren’t in the S&P 500. Thus, a total stock index fund and a total international stock index fund reduces some of this concentration risk, though both have underperformed large-cap U.S. funds.

We are also more likely to own the 2034 list of the most valuable companies on the planet with total stock index funds than we are to own an S&P 500 index fund, since the S&P 500 committee must admit a company into this index (as it moves another out). Tesla, for example, went public on June 29, 2010, but was only admitted to the S&P 500 10 and a half years later on December 21, 2020.

I know a bear market will be coming, and perhaps it’s already started. In the last few weeks, small-cap and value have outpaced the 10 most valuable stocks, meaning they have declined less than these concentrated stocks. Is this the beginning of a bear? I don’t know.

Obviously, I would be the world’s first trillionaire if I could predict bull and bear markets, or the most valuable stocks a decade from now. But rebalancing to a target equity allocation will reduce this risk a bit. Rebalancing manages risk rather than betting on a bear or bull market.

Again, Taylor’s work and knowledge of the stock market’s history is fascinating. In my opinion, it supports a basic boring approach to investing: Own the entire world through low-cost total stock index funds and rebalance between stocks and low risk assets periodically.

Allan Roth is the founder of Wealth Logic, LLC, a Colorado-based fee-only registered investment advisory firm. He has been working in the investment world of corporate finance for over 25 years. Allan has served as corporate finance officer of two multibillion-dollar companies and has consulted with many others while at McKinsey & Company.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Read more articles by Allan Roth

It’s official: In the 150 years that the longest, the most valuable 500 U.S. companies have been tracked, stocks have never been more concentrated than this year. According to Bryan Taylor, chief economist at Global Financial Data, as of June 30, 2024, the top 10 stocks had a market cap of $17.07 trillion, which represented 35.77% of the S&P 500. While these mega cap stocks have declined significantly over the past few weeks, they now actually comprise an even greater 36.19% of the S&P 500 as of August 5, 2024 intra-day.

It’s official: In the 150 years that the longest, the most valuable 500 U.S. companies have been tracked, stocks have never been more concentrated than this year. According to Bryan Taylor, chief economist at Global Financial Data, as of June 30, 2024, the top 10 stocks had a market cap of $17.07 trillion, which represented 35.77% of the S&P 500. While these mega cap stocks have declined significantly over the past few weeks, they now actually comprise an even greater 36.19% of the S&P 500 as of August 5, 2024 intra-day.