Does Dollar Cost Averaging Affect Investment Results?

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Dollar cost averaging involves committing money to the stock market gradually, rather than all at once. This time spent out of the market leads to lower returns, but also to commensurately lower risk.

In talking to investors, we often hear the idea that if one has a certain amount of cash to invest in stocks, it might be better to not do so right away, but to leg into the stock exposure while keeping the cash sitting in a money market account. With the S&P 500 index setting successive new highs, there is increasing angst among investors about entering the market at such lofty levels.

Say you are an investor with $120 to invest. Should you allocate the full $120 to stocks on day one? Or, should you slowly allocate that money to stocks over the course of a year – say $10 per month – while keeping the remainder sitting in a savings account or in a money market fund? We refer to the latter, incremental investment strategy as dollar cost averaging.1

With respect to the U.S. market hitting all-time highs, it should be noted that the S&P 500 in the U.S. and many markets globally have been hitting successive all-time highs for the last 100 years or longer. The next chart shows the S&P 500 index, in log terms to make the trend visible, going back to 1926. Historically, long-term investors would have been poorly served by not buying S&P at the highs, as new highs were perpetually on offer.

Timing market entry

For this analysis, I take dollar cost averaging (DCA) to mean that an investor with $X to invest will allocate a fixed amount of $X into stocks over time, while keeping the remainder in cash.

Importantly, DCA may have psychological benefits for investors: less sense of regret; less anchoring to a fixed price level; a feeling of doing something active. I will not examine these important aspects of the strategy, but instead we focus only on economic outcomes.

To understand the investing implications of DCA, I simulated two daily trading strategies, both of which receive a $1 deposit, inflation adjusted at an annual rate of 2.5 percent, at the start of each calendar year. So there is $1 to be invested at the start of year one, then $1.025 at the start of year two, then $1.051 ($1 x 1.025 x 1.025) at the start of year three, and so on.

- In the first variant, investors put the inflation-adjusted $1 into the U.S. stock market at the beginning of each calendar year. I refer to this as the start-of-year strategy.

- In the second variant, investors put 1/252 (there are 252 trading days in a year) of the inflation-adjusted $1 into the U.S. stock market in every trading day of the year. Alternatively, investors allocate to stocks 1/252 of the value of their cash account, if this is greater.

I added two additional allocation strategies to serve as benchmarks:

- Invest the full cash amount into stocks at the high point of each year. This is not an implementable strategy because it requires knowing the high point of stocks in every year, but it provides a benchmark for a really bad timing strategy.

- Invest the full cash amount into stocks at the low point of each year. Ditto about implementability. But this serves as a benchmark for a really great timing rule.

In all cases, any uninvested cash earns interest at the short-term T-bill rate. Once allocated to stocks, capital stays in the stock account (so no going back to cash). The only timing being tested is when to use cash (or a portion of cash) to buy into the U.S. stock market.

Performance

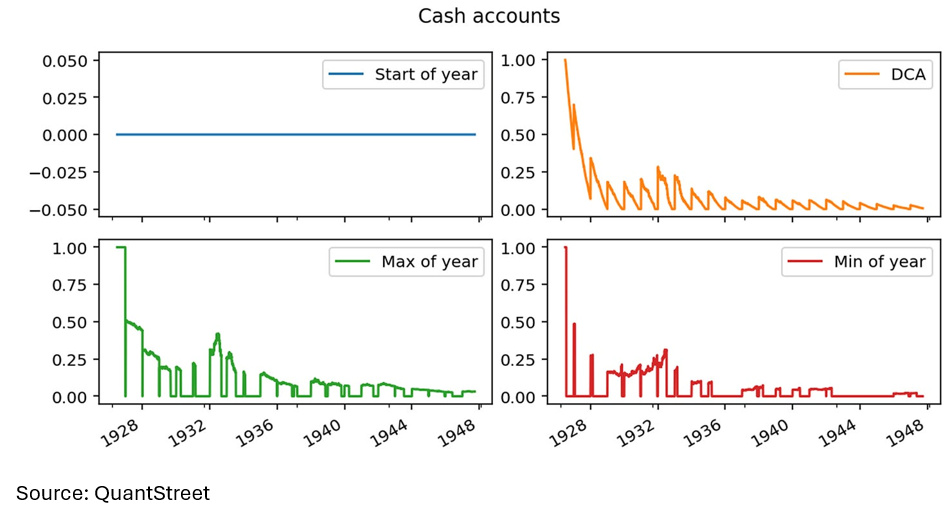

The next chart shows the evolution of the cash account under the four strategies in the early years of the simulation. The solid blue line in the upper left shows the start-of-year fully invested strategy. The cash account is always at zero because as soon as money comes into the portfolio at the beginning of every year it is immediately allocated to the stock market. The upper right panel of the figure shows the percent of the portfolio value represented by the cash account under the dollar cost averaging plan. The saw tooth pattern indicates the receipt of an inflation-adjusted $1 at the start of each year, which then gets slowly allocated to the U.S. stock market over the remainder of the year. Successive jumps in the fraction of wealth sitting in the cash account are smaller because the value of the portfolio grows more quickly than the assumed inflation rate of 2.5 percent.

The lower two panels show what happens to the cash accounts (as a fraction of the portfolio value) in the max-of-year and min-of-year strategies. In both cases, cash sits in the account until a given year’s maximum or minimum stock market level is attained, at which point the cash is invested into the stock market.

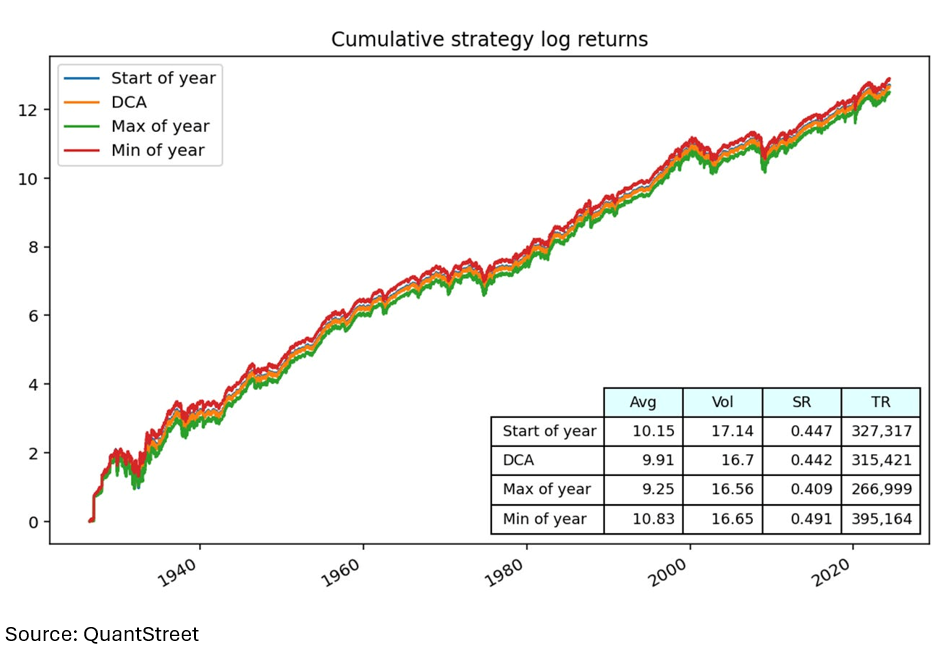

The next chart shows the cumulative return, in log terms, of each strategy. Keep in mind that, in each of the four cases, an inflation-adjusted $1 deposit hits the account at the start of each calendar year. From an initial value of $1, all accounts end up in the vicinity of $300,000 at the end of the simulation period (shown in the TR column of the table below). This just shows what consistent savings combined with compounded interest can achieve.

The average return of the start-of-year strategy is 10.15 percent per year. Since this version of the strategy is always fully invested in the stock market, this just represents the average annualized return of the U.S. stock market over the time period of the analysis. The annual volatility of the start-of-year strategy is 17.14 percent. The reward-to-risk ratio, as measured by the Sharpe ratio, is 0.447. The Sharpe ratio is the ratio of the average historical return of an investment above the risk-free (e.g., T-bill) rate divided by the volatility of such excess returns.

The dollar cost averaging strategy has a lower annual return, of 9.91 percent. It also has a lower volatility, at 16.7 percent. The net effect of these two is that the Sharpe ratio of the DCA strategy is 0.442, just slightly lower than the Sharpe ratio of the start-of-year investment strategy. DCA lowers average returns but it also lower risk, while largely maintaining the same reward-to-risk tradeoff as the invest-right-away variant.

The max-of-year and min-of-year strategies

Not surprisingly, the worst strategy is the max-of-year allocation plan, which allocates the cash account into stocks on the day of the year which represents the high point of that year’s stock prices. What is much more surprising is that the almost 100-year performance of this atrocious timing strategy is still a respectable 9.25 percent annualized return with a 0.409 Sharpe ratio! So if, in every single year going back to 1926, you had picked the absolutely worst day on which to invest in the stock market, you would still have done very well.

On the other hand, if in every year you had a crystal ball telling you to invest at the very lowest price of that year, your annualized return would have been 10.83 percent with a Sharpe ratio of 0.49. So even this full-prescience, optimal timing strategy only does a little bit better than the plain invest-on-the-first-day-of-the-year variant.

The main takeaway from this analysis is that being invested in the market matters more than the exact day on which you choose to make the investment. At least this has been true in the U.S. over the past almost 100 years.

Rolling five-year windows

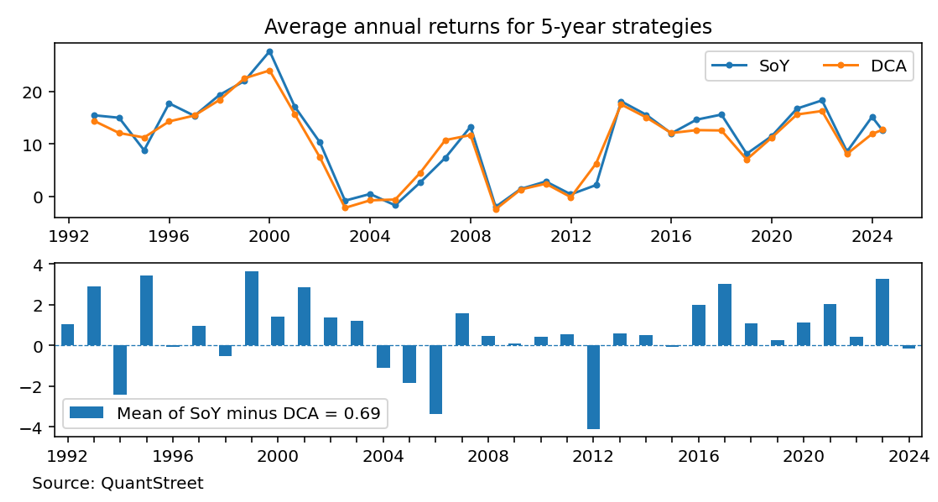

So far I’ve analyzed an almost 100-year investing strategy, which committed an inflation-adjusted $1 into the market in each calendar year. To examine a more practical investment horizon, we now analyze how dollar cost averaging works in rolling five-year windows, starting in 1988. In each window, an investor can allocate only $1 into the stock market. She can either do this at the start of the entire period, which we again refer to as the start-of-year strategy, or allocate daily 1/252 of the $1 into stocks starting on the first day of each five-year window.

The next chart shows the average annual returns earned by the start-of-year (SoY) and DCA strategies in each five-year window, which are labeled with their ending year (so the 1988-1992 window is labeled with “1992”). The bottom portion of the figure shows the annual difference between the start-of-year and the DCA strategy in each five-year window. DCA did better in the five-year windows ending in 2004 (i.e., 2000-2004), 2005, and 2006 because these contain the dot-com bubble, as well as in the five-year window ending in 2012 because this window begins with the 2008 market selloff associated with the global financial crisis. On average, the start-of-year investment strategies outperform the DCA ones by 0.69 percent per year.

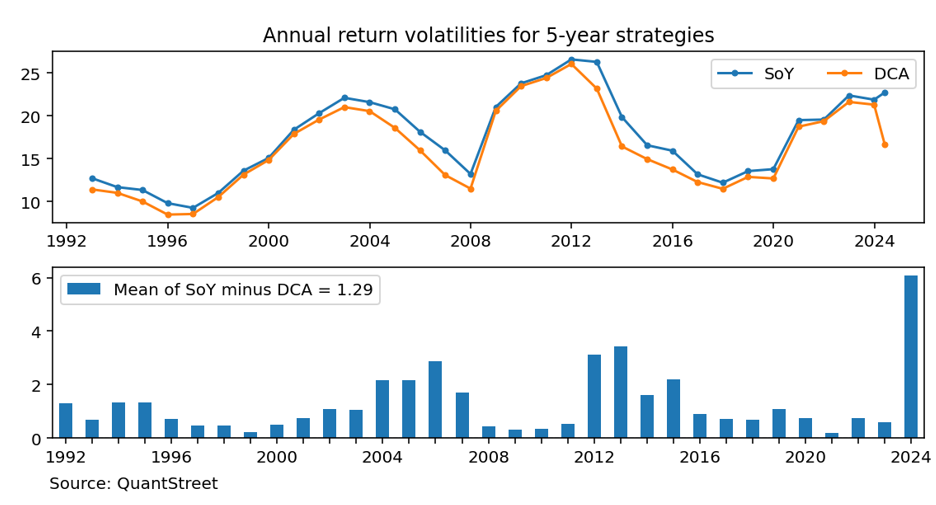

The next chart shows that, while they have lower average returns, the DCA strategies are, in all cases, less volatile than the ones where the investment is made at the beginning of the five-year period. Particularly large volatility gaps occur in the five-year periods ending in 2006, 2012, 2013, and especially 2024. The latter is associated with using dollar cost averaging at the start of the 2020 COVID-19 pandemic, which would have greatly reduced the volatility of the DCA strategy relative to the full capital commitment at the beginning of 2020. Despite this large volatility gap, as of now, there is almost zero return differential in the 2020-2024 time period between the start-of-year and DCA strategies.

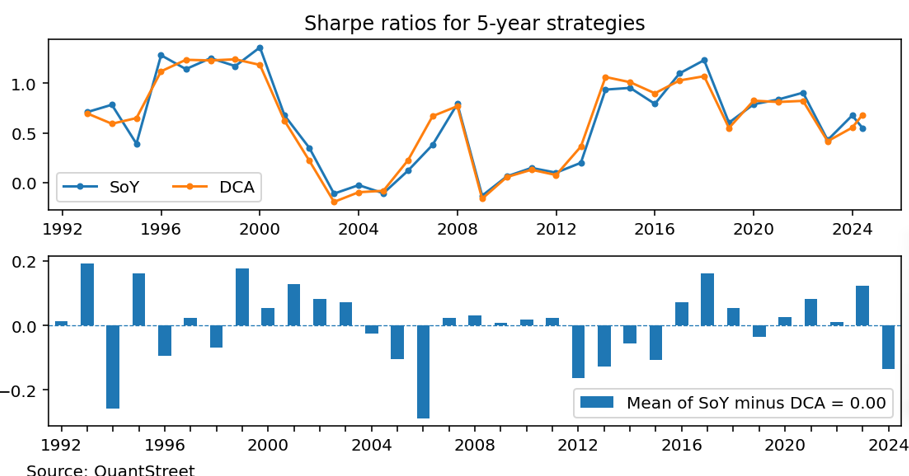

The next chart reports the annualized Sharpe ratios of the start-of-year allocation and DCA strategies in each of the rolling five-year windows. While there is some time variation in the relative level of the Sharpe ratios, the average Sharpe ratio difference between the two strategies is exactly zero, suggesting that the difference in returns and volatilities between allocating to stocks immediately and dollar cost averaging leave the overall return-to-risk tradeoffs of the two plans exactly unchanged.

Summary

Relative to committing capital immediately to the stock market, dollar cost averaging is associated with lower returns and lower risk levels. However, the return-to-risk tradeoff, as measured by the Sharpe ratio, of the two strategies turns out to be the same. Interestingly, full-prescience strategies don’t help that much on the good side (min-of-year allocation) or hurt that much on the bad side (max-of-year allocation). Just being invested in the stock market is the key dynamic. Timing entry using DCA lowers returns by exactly the amount warranted by the drop in volatility.

Outside of behavioral issues, like experiencing regret or anchoring of price levels, investors appear to be better off just setting a targeted risk level for their portfolios, e.g., the appropriate stock-bond mix, and trading to that risk level right away. Waiting to invest simply has the effect of implicitly modifying the targeted risk level.

The caveat is that, while these observations have been true in U.S. markets since 1926, they may not continue to hold in the future. All investors must ensure that their portfolios are constructed in line with their own risk preferences and liquidity needs.

Harry Mamaysky is a professor at Columbia Business School and a partner at QuantStreet Capital.

1 The other type of dollar cost averaging is when individuals simply invest a part of their paycheck into the stock market every month (usually in their 401k or a similar account). In this study, my definition of dollar cost averaging is that only a part of investable capital is moved into stocks every month, with the remainder sitting in cash.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our videos.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All