Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

According to Understanding Stock Market Corrections and Crashes:

- On average, the market has declined 10 percent or more every 1.2 years since 1980, so you could even say corrections are common.

- However, once the market starts to turn, it can recover quickly. The average recovery time for a correction is just four months!

The history of stock market crashes provides confidence in “staying the course” and “buying the dip” because recovery is expected to be quick. Most recently, the recovery from the 2022 stock market decline took only four months; it was average, fast and V-shaped.

But no one knows how long the next stock market crash will last nor how long it will take to recover from that crash. We do know that the past 15 years of rising stock markets is the longest bull market ever and that stock prices are at all-time highs. And we also know that there has never been 78 million people in the Retirement Risk Zone at the same time – these are the baby boomers.

Baby boomers cannot afford a bad crash

Baby boomers need to be concerned about worst cases because the rest of their lives could be ruined by the next crash, and with $70 trillion at risk the stakes are high for them and their heirs. So rather than averages, let’s look at worst cases. That’s what baby boomers need to protect against.

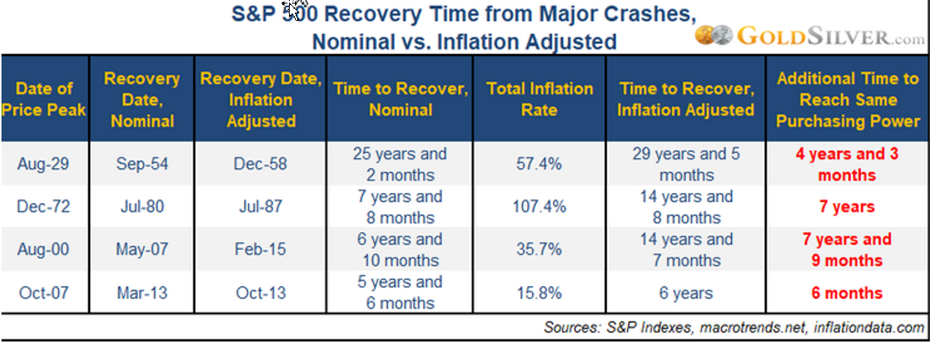

These are the four worst crashes – other than the Great Depression – and the time it took to recover from them:

The Great Depression was the worst crash. It took 25.2 years to recover in nominal terms and an even longer 29.4 years in real (inflation-adjusted) terms. Baby boomers do not expect to live another 20 years. The other bad crashes took 14 years to recover in real terms.

The average boomer is 68 years old and has a life expectancy of 16 years. Many will bail in the face of a crash rather than “staying the course” because they’ll limit their losses, as they should. Even better, baby boomers should not be in the stock market when it crashes. They better get out now.

A longer historical view

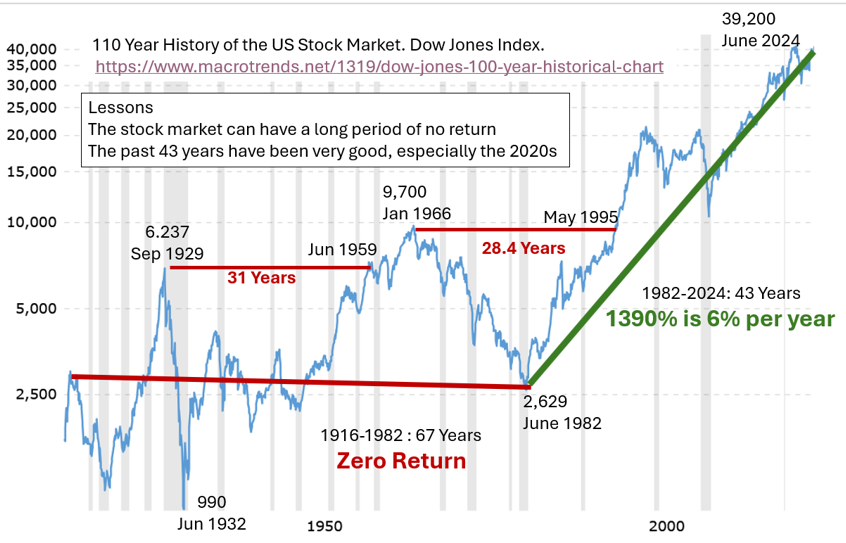

Recovery averages are based on the recent past, but a long 110 year view reveals that the early days of stock investing were very disappointing, with long periods of no returns – it took all the running you could do to stay in the same place. It’s a hockey stick picture, with the last 43 years excelling. The time periods of zero returns are not on the horizon for baby boomers.

The fact that the stock market is currently at its highest price level ever does not portend well for even higher prices. Are the Big Seven and artificial intelligence stocks worth even more than their current price? Time will tell. Remember the dot-com bubble.

As you can see, the “good times” began in 1982 and the really good times have been the current Roaring 2020s – which have begun much like the Roaring Twenties of 100 years ago that led to the Great Depression. Stock prices are at all-time highs, drawing many in who fear missing out (momentum) when there’s reason to fear a bubble burst (crash).

The odds are on a stock market crash, because the stock market always crashes. A crash is long overdue (2022 was a head-fake). The Buffet Indicator stands at an all-time 200 percent high, which is two standard deviations above trend: The stock market value of $56 trillion is twice the GDP of $28 trillion. It is a very expensive stock market and becoming more expensive every day.

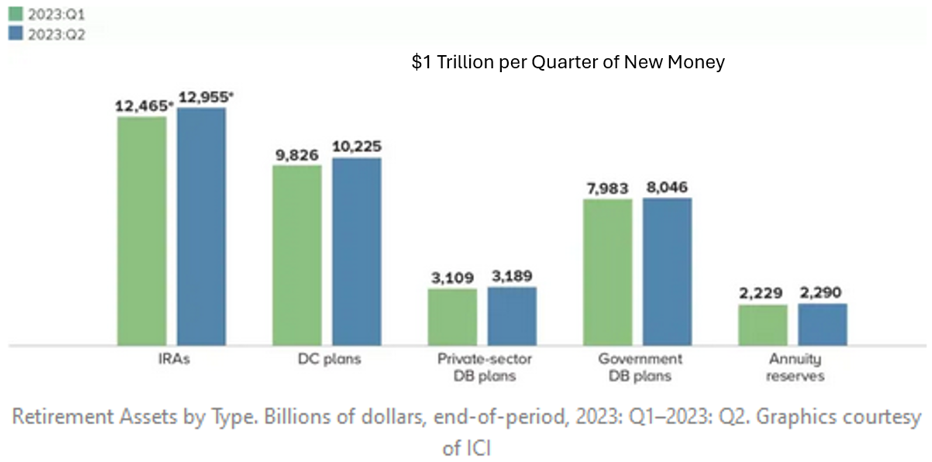

Some attribute the buoyancy of the stock market to the ongoing growth of $4 trillion per year in retirement plans; contributions persist regardless of market values, and much of those new monies are flowing to passive stock index funds. The retirement plan faucet doesn’t care about market values. $4 trillion is seven percent of the $56 trillion total stock market value, which is enough to matter. The Big Seven Megacap stocks are worth $16 trillion.

Baby boomers, protect yourself

Younger people have the time to recover from the next crash. It will be painful for them, but they’ll be okay. Baby boomers, not so much. Baby boomers need to move to the safety of “cash” – low risk assets like Treasury Bills and short maturity Treasury Inflation Protected Securities (TIPS). Baby boomers in target date funds need to get out unless they’re in one of the few that protect, like the Federal Thrift Savings Plan (TSP).

We only live once (I’m a baby boomer). We’ll be out of the Risk Zone in 2030, so we need to defend at least until then.

Conclusion

Wharton Professor Jeremy Siegel’s Stocks for the Long Run is in its fifth edition. It is a very popular book. It is pre-ordained that stocks always win if you wait long enough. But baby boomers do not have the luxury of waiting very long. Their “long run” is very short. Baby boomers should not be in the stock market at this time in their lives. They will spend this decade in the Retirement Risk Zone when investment losses can devastate.

Financial advisors are inclined to recommend staying the course. There’s a business risk in doing otherwise because annual stock returns are positive 75 percent of the time. But this time advisors should focus on protecting, rather than growing, their older clients’ lifetime savings. Life is short, and those savings are all there is.

Ron Surz is president of Target Date Solutions, developer of the patented Safe Landing Glide Path and Soteria personalized target date accounts. He is also co-host of the Baby Boomer Investing Show. Surz’s passion is helping his fellow baby boomers at this critical time in their lives when they are relying on their lifetime savings to support a retirement with dignity, so he wrote a book, “Baby Boomer Investing in the Perilous 2020s,” and he provides a financial educational curriculum.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent market outlooks.

Read more articles by Ron Surz

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.