Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Recently, a few media outlets have warned of the imminent demise of the petrodollar agreement, commonly called the petrodollar. With such narratives comes investor anxiety. Consider the following article titles on the topic:

-

OPEC Will Sever Link with Dollar for Pricing of Oil – The New York Times

-

The petrodollar is dead and that’s a big deal – FX Street

-

After 50 Years, Death of the Petrodollar Signal End of U.S. Hegemony – The Street Pro

Before jumping to conclusions, let’s discuss what the petrodollar is and isn’t. With that knowledge, I will address concerns about the death of the petrodollar and discredit menacing headlines like this one: Petrodollar Deal Expires; Why This Could Trigger ‘Collapse of Everything.’

Before starting, a disclaimer: The New York Times article I refer to above is not recent. I added it to show this is not a new story. The article, dated June, 1975, starts as follows:

LIBREVILLE, Gabon, June 9 — The oil‐producing nations agreed today to sever the link between oil prices and the dollar and to start quoting prices in Special Drawing Rights, the governor of the Iranian national bank, Mohammed Yeganeh, said.

What is the petrodollar?

In 1974, following the economically devastating oil embargo in which the price of crude oil per barrel rose four-fold, sparking a surge in inflation and weakening the economy, the U.S. desperately sought to avoid another embargo at all costs. U.S. politicians theorized that a stronger relationship with Saudi Arabia would go a long way toward achieving its goal.

Fortunately, the Saudis also hoped for a beneficial relationship with the U.S., and they needed a trustworthy investment home for their new oil riches. They also desired better military equipment. At the time, Saudi Arabia was running a huge budget surplus because of its windfall from high oil prices and relatively minor spending needs from within the country.

While there was never a formal petrodollar pact, it is widely believed that the U.S. and Saudi Arabia had a handshake agreement to meet each other’s needs. Saudi Arabia was encouraged to invest its surplus dollars in safe, high-yielding U.S. Treasury securities. In exchange, the U.S. would sell Saudi Arabia military equipment. Both hoped a better relationship would be a productive byproduct. Such is the petrodollar agreement.

The petrodollar was not really about the dollar

The petrodollar discussions were principally about Saudi Arabia needing a safe home for their surpluses and the U.S. seeking dollars to fund large fiscal deficits. While the dollar would be the currency for said transactions, it was not likely the focus of the talks.

In dealing with the immense costs of the Vietnam war and ambitious social spending to pacify social unrest, America sought deficit funding. Saudi Arabia needed to invest its surpluses. Given the unprecedented liquidity and safety of the U.S. Treasury market compared to other options, the “agreement” made a lot of sense for both parties. Furthermore, because Saudi oil revenue would be used to buy dollar-based U.S. Treasury bonds, it made sense for Saudi Arabia to require other oil buyers to pay in U.S. dollars.

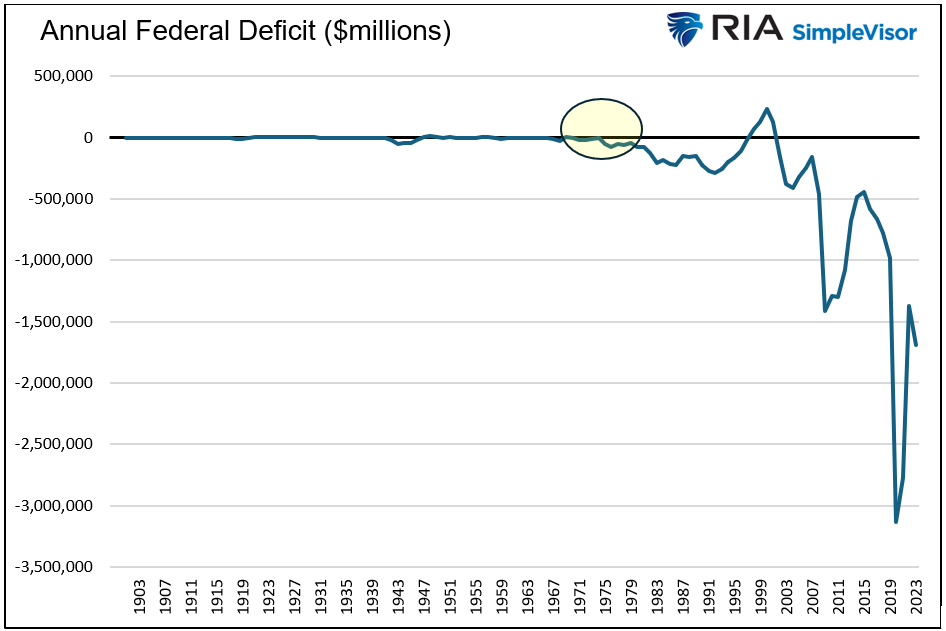

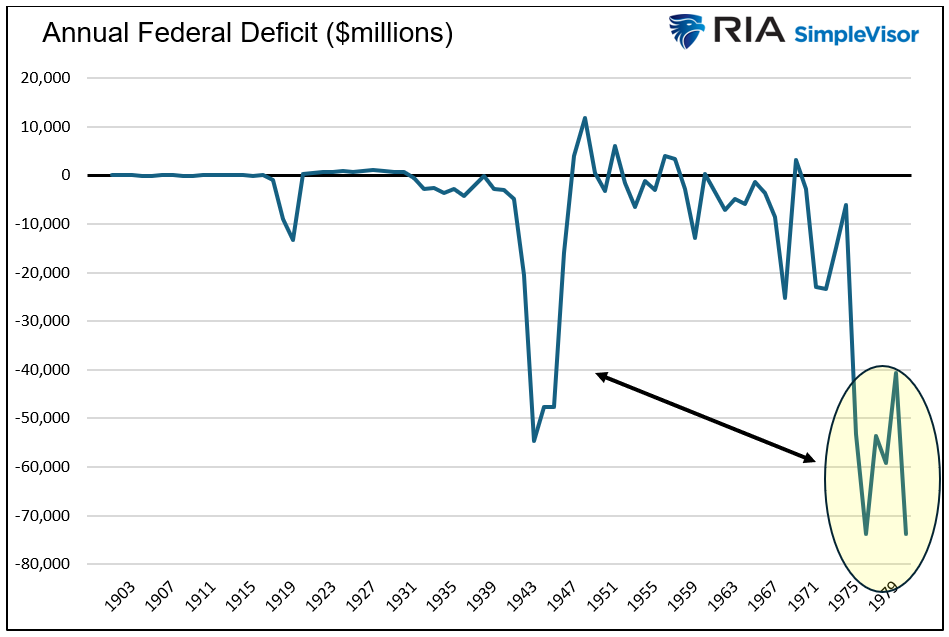

The two graphs below illustrate the deteriorating U.S. fiscal position at the time. The first graph highlights the deficits during the mid-1970s. Today, many would consider a $50- or $60 billion-dollar deficit minimal. But then, the deficits incurred were a sharp departure from the norm.

The second graph provides proper context. The nation was experiencing more significant federal deficits in the mid to late 1970s than it faced during World War II. Given the immense spending on World War II, that fact was stunning to many people at the time.

Saudi Arabia doesn’t have investible dollars

Today, the situation is different. America still desperately needs funding, but Saudi Arabia doesn’t have budget surpluses to invest. Per a Bloomberg article entitled The Petrodollar Is Dead, Long Live The Petrodollar:

Fast forward to today, and Saudi Arabia doesn’t have a surplus to recycle at all. Instead, the country is borrowing heavily in the sovereign debt market and selling assets, including chunks of its national oil company, to finance its grand economic plans. True, Riyadh still holds significant hard currency reserves, some of them invested in US Treasuries. But it’s not accumulating them anymore. China and Japan have significant more money tied up on the American debt market than the Saudis do.

The dollar monopoly

Many believe the U.S. government bullies foreign countries into using the dollar, thus forcing them to have dollar reserves. This seems logical as the reserves must be invested and can help fund our deficits.

I do not know what our politicians say to other countries behind closed doors. But I presume some “persuasion” presses other countries to use the dollar. Regardless, there are not many options competing with the dollar.

The U.S. offers other nations the best place to invest for four primary reasons. As I outline in Four Reasons The Dollar Is Here To Stay:

The four reasons, the rule of law, liquid financial markets, and economic and military might, all but guarantee the death of the dollar will not occur anytime soon.

No other country has all four of those traits. China and Russia lack the rule of law and liquid financial markets. Russia also has a small and fragile economy. Europe does not have liquid enough capital markets or military might.

Gold and Bitcoin are often rumored candidates to usurp the dollar. For starters, they do not earn a return on investment. Possibly more problematic, their prices are incredibly volatile. There are many other difficulties precluding them from full-fledged currency status, which I will save for another article.

Summary

Notwithstanding whether there was a formal agreement, the petrodollar is not going anywhere. Even if Saudi Arabia accepts rubles, yuan, pesos, or gold for its oil, it will need to convert those currencies into dollars in almost all instances.

Consider that Saudi Arabia keeps its currency value pegged to the dollar, as shown in the graph below, courtesy of Trading Economics. They also hold approximately $135 billion of U.S. Treasury securities, a three-year high. Does it seem like Saudi Arabia is trying to disassociate from the U.S. dollar and U.S. financial markets?

Stories like those on the petrodollar and others on the “imminent” death of the dollar have been around for decades. Someday they will be right, and the dollar will follow the way of prior global reserve currencies. But for that to happen there needs to be a better alternative, and today, nothing even close exists.

Michael Lebowitz is a portfolio manager with RIA Advisors and author for Real Investment Advice. For more information, contact him at [email protected] or 301.466.1204.

A message from Advisor Perspectives and VettaFi: Join us on July 25th for the Q3 Fixed Income Symposium, where advisors will gain insights into essential fixed income strategies and market trends to navigate 2024's challenges.

Read more articles by Michael Lebowitz

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.