Cathie Wood’s Prediction at the Halfway Mark

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

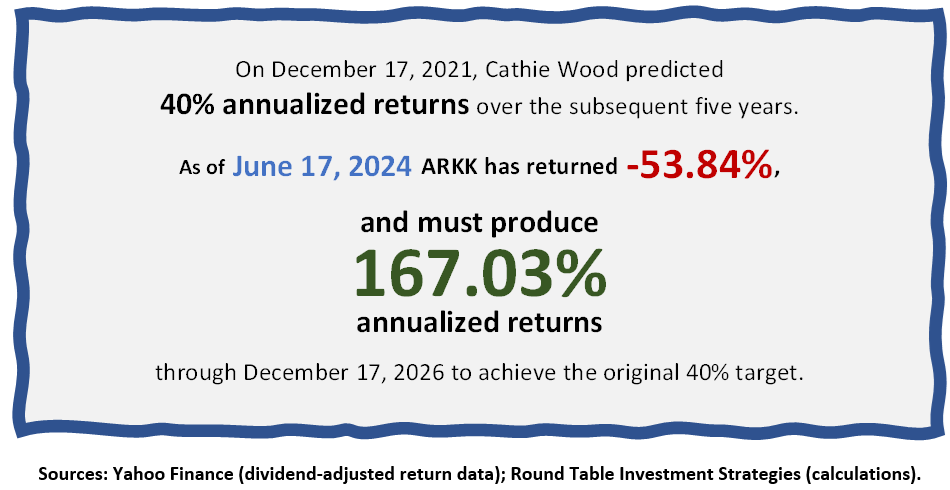

On December 17, 2022, Cathie Wood, CEO/CIO of ARK Investment Management, (in)famously predicted that her firm’s strategies could see a 40 percent annualized return1 over the subsequent five years. On June 17, that prediction rounded the halfway pole and is now headed home, so this seems like a good time to check in on how it is faring:

Wood’s original prediction implied that $1 invested would grow to be $5.47 just five years later, on December 17, 2026. By contrast, the approximately 10 percent annualized long-run total return2 whereby the stocks in the S&P 500 have famously created enormous wealth for investors, would turn $1 into a measly $1.64 over five years.

However, halfway through the five-year prediction window, ARK Invest’s flagship fund, the ARK Innovation ETF (ticker ARKK),3 has returned a whopping negative 54 percent!4 Between that performance and the fact that the prediction horizon has shrunk to 2.5 years, the fund would now have to return over 167 percent per year for that $1 (now $0.46) to reach $5.38 by December 17, 2026!

Granted, I can’t predict with certainty how this will turn out. But let’s just say that if you offered me an even-money bet on whether Wood’s original 40 percent goal would prove successful, I know which side I would take. (Though really, if you thought it was a 50/50 chance or better, why would you offer me a bet that could net you two times your money in two-and-a-half years, when you could just buy ARKK and earn 11 times?)

The 40 percent prediction was unrealistic

I point this out for a couple reasons. First, this seems a sensible time to reiterate how extraordinarily aggressive – I and many others would argue, irresponsibly so – a prediction of 40 percent annualized returns was to begin with. It’s the kind of return figure typically only achieved by the Renaissance Medallion Fund (a hedge fund which, to be clear, doesn’t need or want your money). ARKK is not Medallion, being a long-only exchange-traded fund of listed stocks.

Second, to understand what is implied by a 40 percent per year return prediction, consider what this means about the prices the market – that classic aggregator of the “wisdom of the crowds” – places on these particular stocks. One way to frame how the market sets prices is that the future value of a stock, or really the average of many possible futures, is estimated and then brought forward to the present via some discount rate, which is the return the market requires in expectation5 in order to be willing to take the risk of holding the stock or portfolio of stocks.

So, for example, if the market projects that a proportional slice of the stock portfolio held by ARKK will be worth $5.38 (again, on average, across all possible futures) in five years, it will use that future value and some discount rate to arrive at a price for that portfolio today. What are the odds that that price would be $1? Does it seem likely that the market would really demand a 40 percent expected return to hold that portfolio? The required return from the market’s perspective is the cost of capital from the companies’ perspective, and a 40 percent cost of capital would imply that the market is offering investment dollars to a portfolio of publicly listed stocks at pawn shop-worthy rates.

Again using as a baseline the 10 percent-ish long-run return of the S&P 500 – an index that has done much better historically than the global market overall – we can conclude that a 40 percent return prediction implies one or both of the following:

1. Contrary to the notion that the “innovative” companies in the ARKK portfolio represent with any certainty the economy of the future, the market is demanding a gigantic risk premium relative to what it demands of stocks in general.

2. Or, enormously contrary to the notion of market efficiency, the market has massively underestimated the potential of ARKK’s stocks and thus massively underpriced them.

And if one of these was true of a 40 percent per year prediction back then, imagine what it means for the implied 167 percent per year return now! (Relatedly, stocks are not “on sale” just because they are down. This is true even of entire stock markets, a point I will cover in a future article. But it is especially true of a concentrated subset of stocks, given that many stocks ultimately go to $0.)

My guess is that Cathie Wood’s opinions when making the prediction more closely aligned with the second option, considering that Wood, at that time, could often be heard berating the markets for their manifest foolishness in treating ARK’s “innovative” companies to a collective beating that had already seen ARKK drop 38 percent from its all-time high by December 17, 2022. (You read that right: ARKK has dropped 54 percent after it had already dropped 38 percent. The total drawdown in the fund is a Great Depression-worthy 71 percent.)

One of my bedrock principles of investing is “DATMIS”: Don’t assume the market is stupid! Admittedly, my views occasionally diverge somewhat from this principle. But such divergence is generally driven by an observation that market efficiency makes a better floor than a ceiling, largely due to so-called “limits to arbitrage.”

But insofar as that is correct, there are two implications:

1. It’s relatively easy for prices of (some) securities to be too high,6 because it is much harder for rational actors to exert pressure to bring prices down to equilibrium than it is for rational actors to push prices up to equilibrium. The latter can be accomplished simply by buying in the open market, whereas the former requires the employment of short selling or other complex, potentially expensive tools.

2. Consequently, it may be possible to find inefficiently low expected-return investment opportunities7 (um…hooray?) but finding unexpectedly high expected-return opportunities is far more difficult.8

If someone were to offer me an investment opportunity with a 40 percent annualized return, my refusal of their generosity would be predicated on the following four questions:

1. If they could really generate that return, why would they be offering it to me (a.k.a., the Medallion Fund principle)?

2. Why couldn’t they find someone who would offer them more money today for the same outcome down the road? Surely someone would take 30 percent returns per year? Or 20 percent? Or 15 percent? Or…

3. If #2 isn’t true, then perhaps it’s a crazy risky investment?!

4. Or maybe… just maybe… the 40 percent prediction is too optimistic?

ARK ETFs are available to all, so #1 doesn’t apply. At the very least, #2 through #4 – and the actual performance of ARK ETFs halfway through the five-year prediction window – argue for caution.

In his roles as chief investment officer for Round Table Investment Strategies and portfolio manager for Torren Management, Nathan Dutzmann is responsible for applying financial science and investment research to the process of constructing portfolios tailored to our clients’ individual needs and goals. Nathan was previously an investment strategist with Dimensional Fund Advisors and a partner and chief investment officer with Aspen Partners. He is also a member of the investment industry advisory council for The American College of Financial Services. He holds an MBA from Harvard Business School and a master’s degree in international political economy and a bachelor’s degree in mathematical and computer sciences from the Colorado School of Mines.

1 Okay, really it was a 30 percent-40 percent return, but 30 percent is qualitatively just as absurd and quantitatively mildly less comical.

2 From January 2026 through May 2024, the annualized total return of the S&P 500 Index has been 10.35 percent, enough to turn $1 into $16,200 over 98 years. (Data and calculations: Dimensional Fund Advisors; the S&P 500 Index is owned and calculated by S&P Dow Jones Indices.)

3 Notably, ARKK has significantly underperformed the S&P 500 since ARKK’s inception, despite the fact that the only reason any of us have even heard of ARKK was its significant outperformance prior to 2022.

4 By the way, the S&P 500 Index (total return) was up 23 percent from December 17, 2021 through June 17, 2024.

5 Both “expectation” and “expected” are used here in the strict statistical sense, referring to the projected average of potential future outcomes.

6 Meme stocks, anyone?

7 In an ironic twist, ARKK’s portfolio includes many small cap stocks with low-to-negative profitability, which multiple lines of research suggest may in fact be the lowest expected return segment of the stock market.

8 In a frictionless market, an irrationally low expected return really is an investment opportunity, because you can reverse the investment to capture the inefficiency. But overly high prices caused by limits to arbitrage are, by definition, held in place by market frictions that prevent investors from capitalizing on irrational pricing.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All