Corporate America is buying back its own shares at a near record pace, despite a new one percent buyback excise tax instituted in 2023. While buybacks are often criticized, they are wonderful for investors – though probably not in the way most people think. Let’s dig deeper into what they are and aren’t, and then look at how you can produce tax-advantaged income for your clients.

Corporate America is buying back its own shares at a near record pace, despite a new one percent buyback excise tax instituted in 2023. While buybacks are often criticized, they are wonderful for investors – though probably not in the way most people think. Let’s dig deeper into what they are and aren’t, and then look at how you can produce tax-advantaged income for your clients.

Goldman Sachs estimates that S&P 500 companies will buy back $0.93 trillion of its own stock this year and a record $1.08 trillion next year. That’s significant given the roughly $44 trillion total value of the S&P 500 companies. In fact, between 2010 and 2023, these companies have bought back an estimated $8.77 trillion of their own stock, which represents roughly 20 percent of the current U.S. stock market capitalization.

Buybacks – the myth and the math

Many, like Senator Elizabeth Warren, argue that stock buybacks are “nothing but paper manipulation.” She claims they “line the pockets of corporate executives.” Others claim they are done to increase the earnings per share since they reduce the number of outstanding shares. As someone who has been involved in stock buybacks since the late ‘80s, let me explain both the logic and the math.

At that time, I worked in the treasury department of one of the baby Bell telephone company spinoffs from AT&T. We were printing money and buying businesses we had no core competency in running, such as a real estate business. I pointed out to the Board some of the lessons from the energy business when Mobil Oil bought the retailer Montgomery Wards and Exxon bought companies to create an information systems business. They were epic failures because of the aforementioned lack of a core competency in running those businesses.

I had absolutely no idea whether our company stock was over- or undervalued, but research showed that investors can diversify in a much more efficient manner than companies can. So the argument was that we should return the cash to our investors if we couldn’t invest within our core competency and earn more than our cost of equity. Then those investors could invest the capital returned in companies that already have a core competency in their industries.

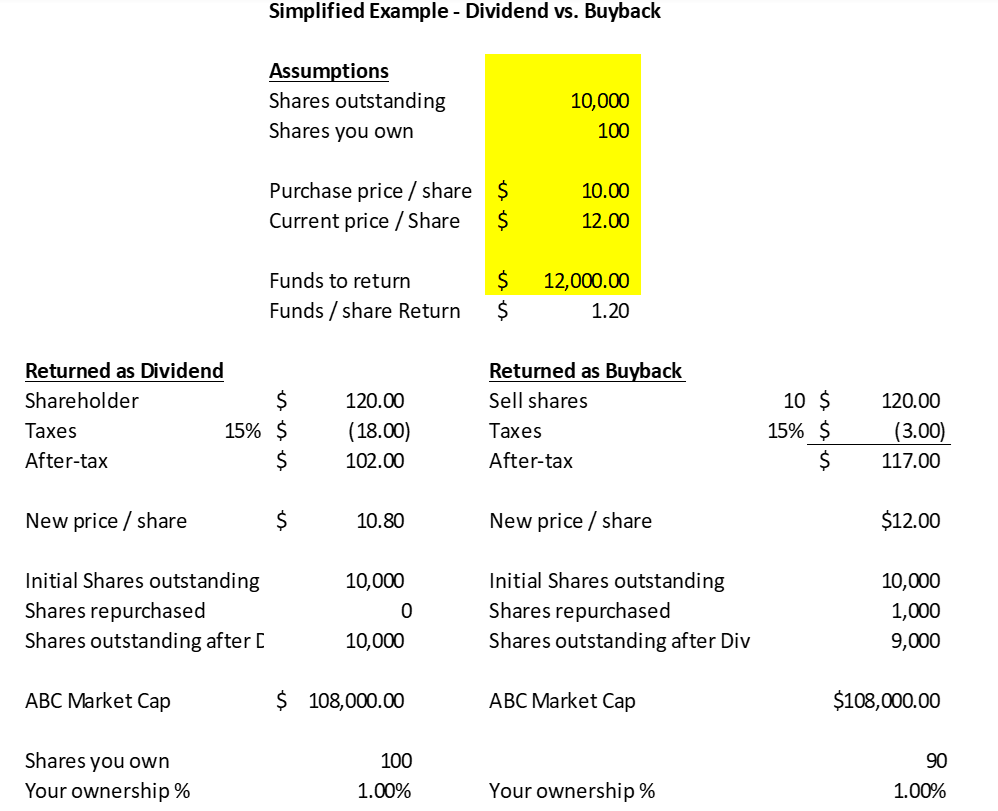

There were two ways to return cash to shareholders – either increase our dividend or buy back our own stock. We concentrated on the latter as the math of the tax-efficiency was compelling. Here is a simplified illustrative example.

Say you own 100 shares of ABC Company that you bought for $10 a share a little over a year ago. ABC has 10,000 outstanding shares so you own exactly one percent of the company. ABC is currently trading at $12 a share and wants to return $120,000 or $1.20 per share to its shareholders. If it pays you a $120 dividend, you will likely be taxed at least at the 15 percent marginal tax rate so you will be left with no more than $102. All things being equal, the share price will drop by the $1.20 dividend and you’ll still own one percent of ABC.

But if ABC instead decides to do a stock buyback, it can buy 10 percent of its outstanding shares. It returns the $12,000 by buying back 1,000 shares at the $12 per share price. You sell 10 shares (10 percent of your 100 shares) and are left with 90 shares. You receive the same $120 but now have a long-term capital gain of two dollars per share or $20 in total. At the same 15 percent marginal tax rate, your taxes are only three dollars and you are left with $117, or $15 more than the dividend scenario.

You may be thinking that you own less of the company since you sold some. But, in reality, you are left with 90 shares and the company now has 9,000 shares outstanding. You still own the same one percent of the company. In each case, you own stock worth $1,080 in a company with a market cap of $108,000. If you decided not to sell your 10 shares, it would be similar to letting your dividends reinvest though, in a more tax-efficient manner. You’d own 100 shares of the 9,000 outstanding or 1.11 percent of the company.

This is before the new one percent buyback tax but you get the principle. Though now ABC would have to pay a $120 tax, it would save shareholders far more. That’s likely why so many of the S&P 500 companies are opting to pay the tax since they work for their shareholders.

Applying this theory to the real world

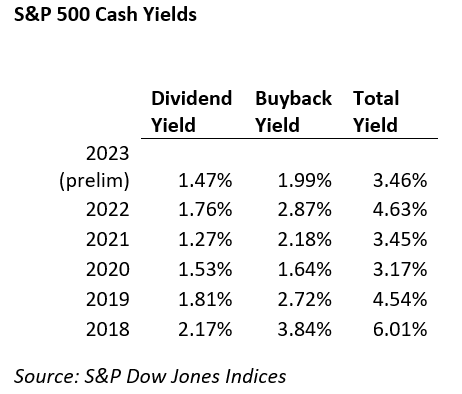

The dividend yield of the S&P 500 has been plummeting. At the end of 2023, it was only 1.47 percent. Yet S&P Dow Jones Indices reports that buyback yields were nearly two percent bringing the total yield to 3.46 percent.

You can see above that the total yield of the dividend and buyback has been as high as 6.01 percent and as low as 3.17 percent so it’s not nearly as stable as the pure dividend yield. While dividend yields are more tax-efficient than ordinary income, the buyback yield is even more tax-efficient. For example, one could sell 1.99 percent of their S&P 500 index fund and still own the same proportion of the total S&P 500 but pay an even lower tax rate. Our clients come out better than if they had paid the entire 3.46 percent in a dividend.

And stock buybacks aren’t just in the U.S. S&P Global reports that 29 percent of dividend buybacks occurred outside the U.S.

Valid criticisms of stock buybacks are in decline

The biggest criticism I used to see is that they benefit senior management in the value of their stock options. As we saw in the simplified example, the stock share price declines by the dividend per share paid which reduces the value of management’s options. The stock price does not decline with stock buybacks, so it benefits the option holders.

But management financial incentives are moving away from stock options toward restricted stock units (RSUs) which, once vested, generally carry the same rights as other common shareholders. Thus, management’s incentives are more similar to shareholders’ and they benefit irrespective of whether cash is returned through dividends or buybacks.

In fact, management may actually see reduced bonuses with buybacks. That’s because the one percent buyback tax is paid by the company, which lowers post-tax profits that may be linked to bonuses paid in cash or RSUs. So I view it as encouraging that management has put shareholders first.

Another criticism to stock buybacks is that they give too much flexibility to management. If a company lowers their dividend, Wall Street punishes the stock when it is announced. Yet when the company buys less of their own stock, very little happens to the share price. While the company can do a special dividend, continuing to do so would likely lead to shareholders expecting a dividend ever year. But management should be focused on the long-run and less concerned with quarterly dividends.

Yet another criticism is that companies should be rewarding employees rather than buying back their shares. While that may be true, it’s irrelevant in whether cash is returned via a stock buyback or dividend. One final criticism is that the capital should instead be invested in strengthening supply chains, creating good jobs, and bringing down prices for consumers. I couldn’t disagree more. When the capital is returned to shareholders, it is being invested in our economy to do just that.

Conclusion

The resurgence of stock buybacks is great for shareholders in that cash is being returned in a far more tax-efficient manner than dividends. Buybacks should only be done when the management has no good options to invest capital in their core competency and earn more than their cost of equity. Management should return any excess cash to shareholders to allow them to redeploy their capital into the economy. This can be done via dividends or stock buybacks. The latter is still more tax-efficient even with the one percent buyback tax.

Explain to your clients that the best income fund may actually be something like an S&P 500 or total stock index fund. It produces good cash flow which the client can either decide to take in cash (by selling the same percentage as the buyback) or reinvest some if they don’t sell. Most of that cash flow is in the buyback yield which is even more tax-efficient than dividends.

While we don’t know the future, the fact that markets are now near an all-time high means most of the $8.77 trillion of stock buybacks since 2010 were purchased at much lower prices than today. Our clients have benefitted greatly from stock buybacks and likely will continue to do so.

Allan Roth is the founder of Wealth Logic, LLC, a Colorado-based fee-only registered investment advisory firm. He has been working in the investment world of corporate finance for over 25 years. Allan has served as corporate finance officer of two multi-billion-dollar companies and has consulted with many others while at McKinsey & Company.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our videos.

Read more articles by Allan Roth

Corporate America is buying back its own shares at a near record pace, despite a new one percent buyback excise tax instituted in 2023. While buybacks are often criticized, they are wonderful for investors – though probably not in the way most people think. Let’s dig deeper into what they are and aren’t, and then look at how you can produce tax-advantaged income for your clients.

Corporate America is buying back its own shares at a near record pace, despite a new one percent buyback excise tax instituted in 2023. While buybacks are often criticized, they are wonderful for investors – though probably not in the way most people think. Let’s dig deeper into what they are and aren’t, and then look at how you can produce tax-advantaged income for your clients.