Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

The Magnificent Seven is an old movie with a new cast.

Every so often, a story about a group of companies whose futures seem certain captures the imagination of investors. Previous ones have included the Nifty Fifty in 1970, Peak Oil in 1980, the Japanese miracle in 1990, the dot.com boom in 2000, and rise of China in 2010.

Every time, persuasive narratives drove high expectations and a cheery consensus, but expectations were not matched by reality. Unforeseen disruption, relentless competition, and the pressure of lofty valuations typically preceded disappointing returns for shareholders.

In the spotlight today are the “Magnificent Seven,” which include Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia, and Tesla. These seven stocks account for over 30% of the S&P 500 by market capitalization.

Avoiding the “Magnificent Seven” because of concentration alone, however, lacks rigour. While it’s worth studying patterns of human behavior, a reductionist approach overlooks the fundamental strengths of these businesses.

As unconstrained global value investors, we believe durability is the key to equity investing. Our firm invests in companies resilient to competition and disruption over decades, protecting superior returns on capital and cash flows. We also believe the price you pay is crucial to prospective returns. In short, we buy durable businesses when they are cheap.

The magnificent seven’s good run

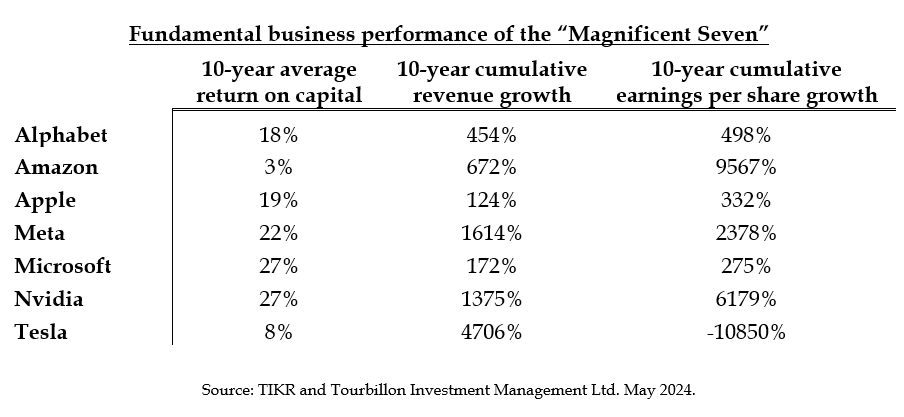

The “Magnificent Seven” are societally relevant, offering products and services that have materially improved how we communicate, work, shop, play and even travel. One can question the broader impact of social media, market share dominance of app stores, regulatory scrutiny on anti-competitive practices, or the power consumption and availability of data centers. That said, shareholders and employees have unequivocally benefitted from a significant increase in revenues and share prices at these companies.

These results are, in aggregate, excellent. Apart from Amazon (which has experienced extraordinary growth self-funded by cashflows) and Tesla (which operates in the ultra-competitive automotive market), returns on capital have been consistently high, supporting shareholder value creation. These companies have been able to leverage the power of software and the internet to grow with very little in the way of incremental capital. Software doesn’t incur high marginal costs, and the internet has made distribution cheap. This has allowed them to invest in new ventures, acquire competitors and hire the brightest people over the past several years.

The strength of these business models naturally invites competition (and regulation). As these companies have matured, market shares have consolidated, and they appear to have become more durable. However, they operate in sectors where the pace of innovation is high, and the threat of disruption equally so.

It is instructive to consider the counterfactuals. What would have happened to Meta (then Facebook) had it not acquired Instagram, or was prevented from doing so? How about Alphabet (then, Google) acquiring DoubleClick? Without the financial success of AWS, would Amazon still be able to offer the prices and convenience it does today in its retail operations? Nvidia’s unofficial motto is ‘only 30 days until bankruptcy,’ which was borne from the early days of the business when its first chip proved a total failure. Or, how about Elon Musk saying that Tesla was within three months of bankruptcy as recently as 2019?

Great expectations, little margin for error

We cannot know the answers to these questions, but we do know the essence of value investing is to allow a margin of safety about an uncertain future. This is the main reason we do not own these businesses today: At today’s valuations, there is very little margin for error.

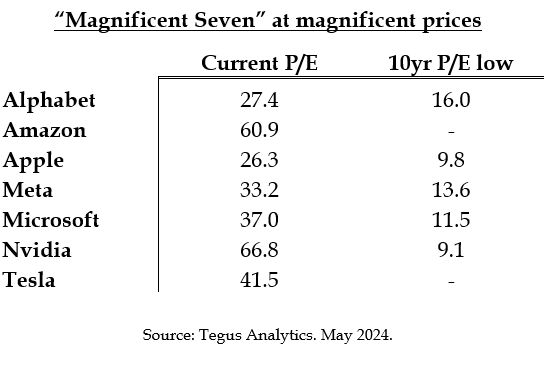

The average P/E of the “Magnificent Seven” is around 42x, hardly a bargain. To put into perspective, at today’s prices, earnings will have to almost quadruple (3.8x) to generate a reasonable nine percent earnings yield. That is a tall order for any company, let alone a group that already generates $377 billion in combined earnings.

Investors who are positively predisposed to the “Magnificent Seven” may argue that multiples are deservedly high because of their market positions, cash flows, returns on capital and large addressable markets. Perhaps… but all of that would have been true for the past decade, as well, yet these companies have frequently been available for purchase at much more attractive valuations. Is it so unthinkable that history might repeat?

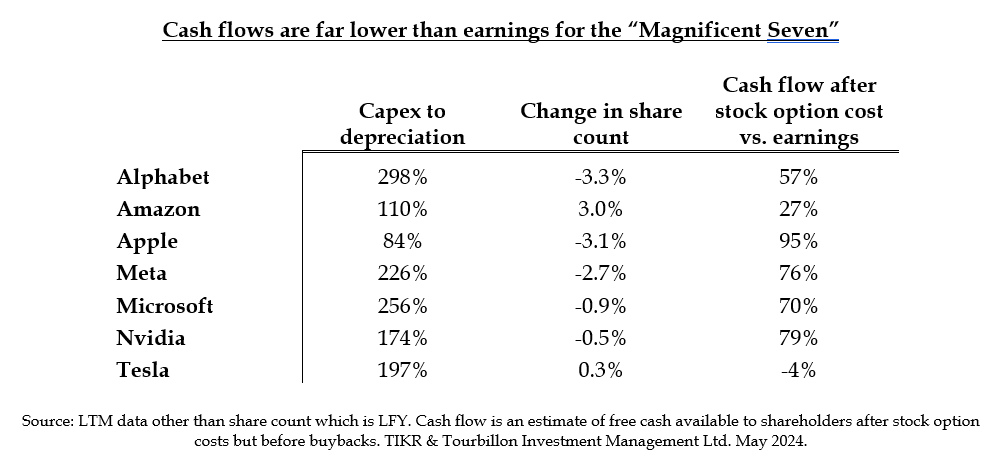

The discrepancy between cash and earnings

Although earnings are generally a reasonable proxy for cash flows, there is a growing discrepancy between the two at these companies today. True cash flows available to shareholders are lower than reported earnings by $162 billion for a conversion of only 57 percent:

There are a few reasons for this:

-

Capital expenditures. Capital expenditures for the group were $177 billion over the past year – a vast sum, nearly twice depreciation expense. This could pave the way for future growth, but nascent areas like AI are inherently less predictable.

-

Share buybacks at high valuations. At $212 billion, share buybacks have averaged 55 percent of the “Magnificent Seven”’s earnings. However, the total share count has only shrunk by around one percent. Though this is often portrayed as capital being returned to shareholders, buybacks at today’s high valuations do not create much value.

-

Stock options. Stock options are an integral part of compensation in Silicon Valley. They are a significant and real cost totalling $88 billion that shareholders must consider. Furthermore, this cost is generally understated in GAAP accounting due to inherent flaws in option pricing models.

Not all “Magnificent Seven” stocks are equally magnificent

We avoid broad heuristics based on historical analogy or the often-arbitrary nature of narratives. Instead, we apply a first-principles approach based on evidence.

The “Magnificent Seven” are not alike to our minds. For example, Tesla operates in a difficult industry, and we find it hard to judge whether it can escape the poor economics prevalent amongst automotive manufacturers. Nvidia has scarcity value today, but we are unsure about how durable that scarcity will prove to be. While Google and Meta enjoy superb unit economics in consolidating markets in digital advertising, there is a worrying deterioration in cash conversion.

However, there are some enduring businesses in the group. Amazon offers a difficult-to-replicate value proposition and operates with a stakeholder orientation by reinvesting into the franchise and the ecosystem. Microsoft enjoys strong customer loyalty and high barriers to entry. And Apple’s products are everyday necessities, with a potential customer surplus on offer.

Today, we do not own any of the “Magnificent Seven” and prefer to wait patiently until the shares trade at valuations that are cheap. When that happens they may not be viewed as so magnificent after all.

Ben Beneche and Ramesh Narayanaswamy are co-founders of Tourbillon Investment Management, a long-only public equity fund investing in 15 to 25 businesses globally using a fundamental, value-oriented approach.

Tourbillon Investment Management Ltd. is an appointed representative of Eschler Asset Management LLP which is authorised and regulated by the FCA (#510079), and a registered investment adviser with the SEC. The investment products and services of Eschler Asset Management LLP are only available to professional clients and eligible counterparties; they are not available to retail (investment) clients.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent market outlooks.

Read more articles by Ben Beneche, Ramesh Narayanaswamy

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.