Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

One year ago, Wall Street analysts braced for an economic downturn, if not a full-blown recession. The post-COVID inflationary environment coupled with a hawkish Fed significantly strained households, causing consumers of all income levels to feel less financially secure as they saw their savings dwindle and their debt rise.

But the prognosticators couldn’t have been more wrong.

Over the past year, we’ve seen strong economic indicators across the four key metrics – job growth, wealth levels, consumer confidence and housing – and all signs point to a positive long-term outlook for American consumers.

Why? For one, we are experiencing enduring generational shifts. While baby boomers are retiring, millennials are buying homes and forming families, further driving household consumption. Since roughly three-quarters of the U.S. GDP is driven by consumer spending, this trend will lead to prolonged growth.

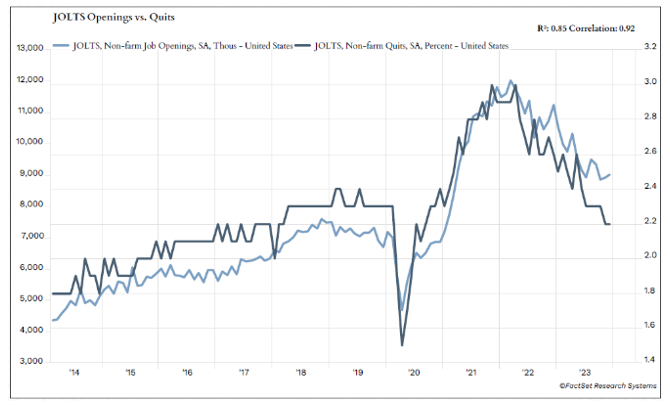

We continue to see positive news on the labor front as the U.S. economy added jobs for the third year in a row. According to the Bureau of Labor Statistics’ Job Openings and Labor Turnover Survey (JOLTS), job openings held steady at 8.8 million, and quit rates fell below even pre-pandemic levels to 2.5%. This demand for skilled labor has empowered workers across multiple industries, leading to last year’s highly publicized strikes by actors, directors and auto workers, among others.

Dubbed the “Year of the Strike,” 2023 saw a record number of work stoppages – the Wall Street Journal reported 354 in 2023 involving 492,000 workers – or nearly eight times the number of workers engaged in strikes in 2021 and almost four times the number for the same period in 2022. But greater awareness around unionization hasn’t translated into meaningful increases in participation rates. Last year, the Economic Policy Institute noted that 16.2 million workers were represented by a union – which, though an increase of 191,000 workers, also represents a slight decrease in the percentage of total workers represented by a union.

Though the economy bounced back quickly from COVID-19, some pandemic-era changes have had more permanency. According to a survey last year from Pew Research, about one-third (35%) of workers with jobs that can be done remotely are working from home, and 41% of these employees are working a hybrid schedule, up from 35% in Sept. 2022. This aspect of the “new normal” has staying power, as office workers have prioritized flexibility and a better work-life balance.

No longer constrained by location, highly skilled workers are becoming choosier about their overall well-being, which has created a new equilibrium in the jobs market with a drive toward innovation and greater productivity. It’s also caused a “brain drain” in some of the largest cities, as skilled employees relocated to suburbs that offer more value and a higher quality of life.

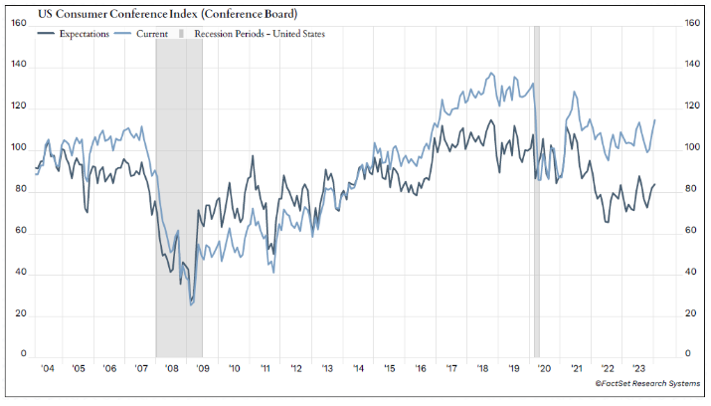

With a robust jobs market and inflation cooling, consumer confidence has increased. The University of Michigan Consumer Sentiment Survey soared 13% in January, reaching its highest level since July 2021. Meanwhile, real wages are up, and so are personal savings, with Americans, on average, saving 4.1% of their disposable personal income.

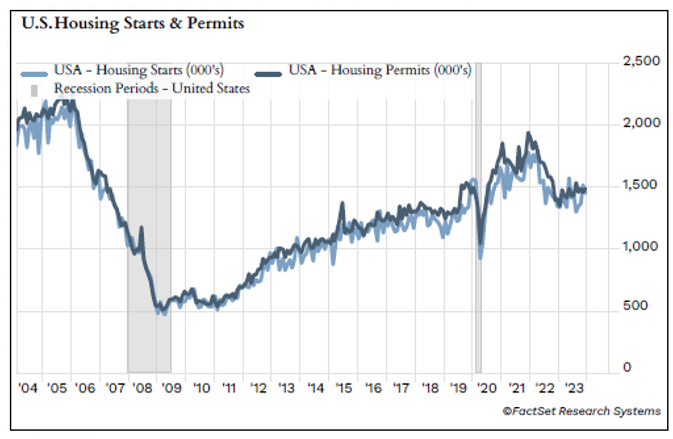

On the housing front, after pending home sales hit their low point in August, the index for sales of existing homes (PHSI) rebounded to just over 8% to 77.3 in December, according to data from the National Association of Realtors. We believe home-buying rates will be on an upward trajectory as the Federal Reserve begins cutting interest rates later this year.

Since the start of the pandemic, home prices have continued to set records. In November, the Case-Shiller Home Price Index was 313.28, up from 311.26 in October and 298.92 over the previous year. But new housing stock, coupled with lower mortgage rates, should help to alleviate some pricing pressure. In December, building permits for privately owned housing units were issued at a seasonally adjusted annual rate of 1,495,000 – a 1.9% increase from November and a 6.1% year-over-year rise from December 2022.

Today, more Americans than ever are graduating from college with a four-year degree. A recent study conducted by the National Center for Educational Statistics of the 2.7 million high school graduates in 2021, roughly 62% enrolled in college by October 2021. There is an overwhelming demand for trained and highly skilled talent in sectors such as cybersecurity and engineering, health care, transportation, and retail – in corporate America and the private sector, more broadly.

Demand also remains elevated for skilled trade positions such as electricians, welders, plumbers, mechanics, and equipment technicians. The U.S. Bureau of Labor Statistics projects 4% employment growth for construction and extraction occupations between 2021 and 2031. The report also indicated that specialized skilled trades, such as wind-turbine service technicians and solar photovoltaic installers, are among the top 20 fastest-growing U.S. occupations.

Despite the positive data, not all Americans advanced economically at the same rate, which can distort the picture. A growing inequality exists between those upwardly mobile and the bottom 20% of the population. In certain parts of the country, climbing the economic ladder has proven more difficult, increasing the divide between the haves and have-nots. It will take significant motivation and participation to ensure that all Americans – regardless of their origin – have access to opportunity.

Though the overall health of the U.S. consumer is strong, we must also be mindful of potential longer-term risks. G20 nations are grappling with a shrinking population, impeding economic growth. By 2040, there will be a graying of the population as the percentage of those under the age of 18 will fall from 22.2% to 20.6%. – a demographic shift likely to strain the future funding of defined benefits programs.

Even with challenges on the horizon, the American worker and consumer has rarely been on firmer footing. From low unemployment and real wage growth to high educational attainment rates and a better work-life balance, Americans are earning more and saving more; they’re putting down roots and working to live, not living to work.

Though moving from the lowest rung of the economic ladder to the highest may be more challenging than in generations past, Americans continue to possess an adaptive, resilient, and entrepreneurial spirit. They lead the way, staking out new opportunities, relocating to better economic environments and flooding the economic system with new small businesses. Since the onset of COVID-19, there have been 16 million new small businesses launched nationwide, a near doubling of the rate from before the pandemic. The American consumer/worker/owner is driving growth and prosperity by both quantifiable and qualifiable metrics.

Our economic system and free markets benefit from our uniquely American ability to chart new paths. Though we are still grappling with the post-pandemic shock, throughout last year pundits underestimated the durability of the American consumer. We endeavor to allow the weight of the evidence to guide our conclusions and forecasts.

While each investor’s objectives are unique, we encourage you to contact your Callan Family Office relationship team to learn more about how this information can impact your portfolio. By Douglas Evans, chief investment officer, and Patrick Thompson, investment management partner, at Callan Family Office.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

More ETF Topics >

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.