Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

On December 12 and 13, the Department of Labor's (DOL) Employee Benefits Security Administration held a virtual public hearing on its proposed “Retirement Security Rule: Definition of an Investment Advice Fiduciary.” Had I had the opportunity to testify at that hearing, I would have made the points below summarizing the comment letter that I submitted at the submission deadline of January 2, 2024.

The heart of the matter that I sought to explain to the DOL in my comment submission is the following:

- Advice can only occur at the end of an advising process.

- Only advisors can “sell” (receive compensation for) advice.

The DOL does not have jurisdiction to say to either the SEC/FINRA or to state insurance regulators that distributors (broker-dealers in the case of FINRA, agents in the case of state regulators) operating under their respective regimes are entitled to sell advice. Historically, the title and identity “advisor” has belonged, and should continue to belong, solely to those individuals entitled by an overseeing regulator to sell advice.

- Services are verbs, products are nouns, and, as the pre-DOL4.0 regulatory regime has stood in financial services for many decades, only service providers can sell advice, which occurs at the end of a process of advisement.

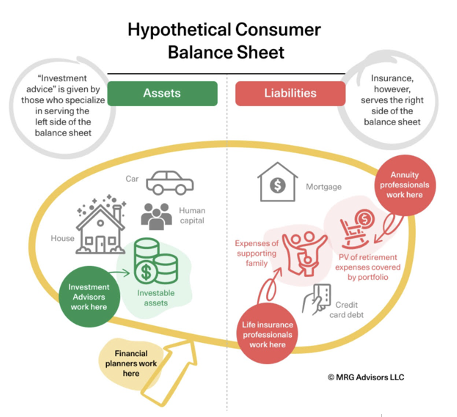

- “Financial” and “investment” are not synonyms. Finances refer to the ability of, and solutions for, a person to meet their cash-flow needs. Understanding of finances incorporates planning, risk tolerance and management, portfolio construction and monitoring, and other disciplines; notably, it also includes consideration of managing liabilities. Investments, on the other hand, are limited to products included within an asset portfolio.

- Financial = wealth (assets – liabilities). Financial in this context refers to the ability of a financial plan to meet the cash-flow needs represented by the liabilities.

- Insurance (from the standpoint of the purchaser) means liability minimization.

Regulatory conflation between financial and investment advisement results in recurring advisory compensation almost exclusively through the lens of AUA/AUM, which in turn results in suboptimal American retirement outcomes, because an investment advisor acting in a fiduciary capacity can absolutely be a fiduciary in the field of asset management (which means asset maximization subject to risk tolerance constraints) while not at all being a fiduciary in the field of wealth management.

Why is this an issue? For example, a fiduciary in the field of investment management may recommend a portfolio allocation that is consistent with an investor’s risk tolerance. A standard “risk tolerance” questionnaire that a financial professional may use to assess risk tolerance is not required to include “risk that my portfolio runs out of money before I die” as an investment risk worth asking the investor about.

This standard process for investment recommendation-making by asset management fiduciaries carries no obligation to consider how such a portfolio may or may not meet the need of steady retirement income for the investor, as long is it is invested to their investment risk tolerance. As such, a fiduciary in the field of asset management will not be held responsible if the client’s portfolio runs out of money before they die.

In this case, the asset manager’s GIPS-compliant performance metrics do not include reporting on cash flows into and out of the portfolio. Irrespective of how frequently clients’ portfolios run out of money in retirement, AUM-billing asset management fiduciaries remain entitled to call themselves fiduciaries. This is why regulators must distinguish financial advisement from investment advisement.

- As such, I recommended to DOL:

-

- Do a find/replace of “investment” to “financial” in its legislation.

- Complete the field of financial advisement by codifying one of the three fiduciary advisory roles suggested below, while getting financial planning out from under the Investment (which is not financial) Advisers Act of 1940 (as amended):

- Retirement Income Adviser (advisement upon income statement)

- Wealth Adviser (or financial adviser or financial planner not under Investment Advisers Act) (advisement upon statement of net worth)

- Insurance Advisor (advisement upon right side of balance sheet)

- Regulate distributor behavior under the additional regulatory regime that it picks from among these three options.