Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

While cost of living adjustments (COLAs) with single-premium immediate income annuities (SPIAs) are uncommon, they are often discussed as a way to provide inflation protection for retirees. But nominal COLAs with SPIAs can actually increase inflation risk because they place a greater strain on the portfolio earlier in retirement (due to the lower initial payout) and are less likely to result in more income in higher inflationary environments, especially if the retirement portfolio is designed with some degree inflation hedging. Therefore, while fixed COLAs seem like an attractive way to address inflation in retirement, they actually increase inflation risk, not reduce it.

Fixed COLAs

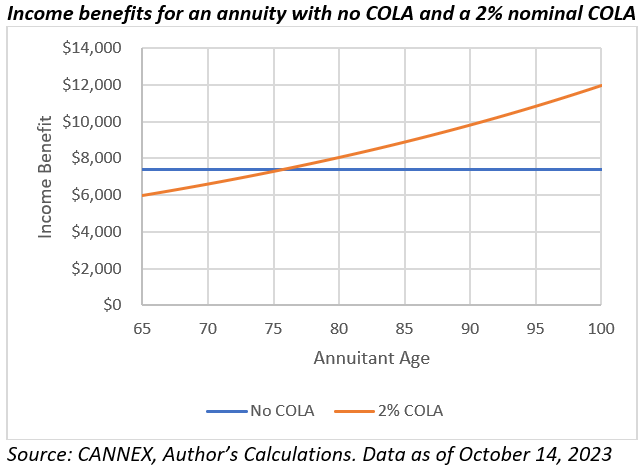

A fixed COLA provides a predetermined increase in the income benefit of an annuity for the life of the contract. For example, with a 2% COLA, if the initial income benefit (in the first year, assuming annual payment frequency) was $10,000, the next year it would increase by 2% to $10,200, and then that benefit to $10,404 and so on (i.e., 2% per year for life). The adjustment typically compounds over time, which results in a benefit that can increase significantly at older ages, but also means a lower starting benefit, as noted in the following exhibit, which includes the income benefits based on two quotes obtained from CANNEX on October 14, 2023, for a 65-year-old male life-only SPIA.

The average payout rate for an annuity with no COLA (among the highest 10 available) was 7.37% versus 5.8% for an annuity with 2% annual COLA. You can see how the income benefits would change throughout retirement in the exhibit below.

The decision to include a COLA represents a “trade.” The annuitant gets a lower initial benefit but can get higher income the longer they survive. COLAs on SPIAs and deferred-income annuities (DIAs) are relatively rare, though. For example, only approximately 5% of annuity quotes on CANNEX include any type of COLA, and this percentage has been persistent over time. For example, when reviewing the CANNEX Annual Survey Experience Reports in 2012, 2017, and 2022, I found they were included only in 4.4%, 7.3%, and 3.6% of quotes, respectively. The last year a COLA explicitly linked to inflation (i.e., the CPI-U) was available (i.e., quoted) was in 2019; therefore, only fixed (nominal) COLAs are available today.

Adding the COLA increases the duration of the annuity. For example, the mortality-adjusted duration of SPIA with no COLA would be approximately 10.8 years versus approximately 12.0 years with a 2% COLA. Assuming a 5% discount rate, it takes approximately 25 years before the 2% COLA SPIA has a higher net present value than the SPIA with no COLA.

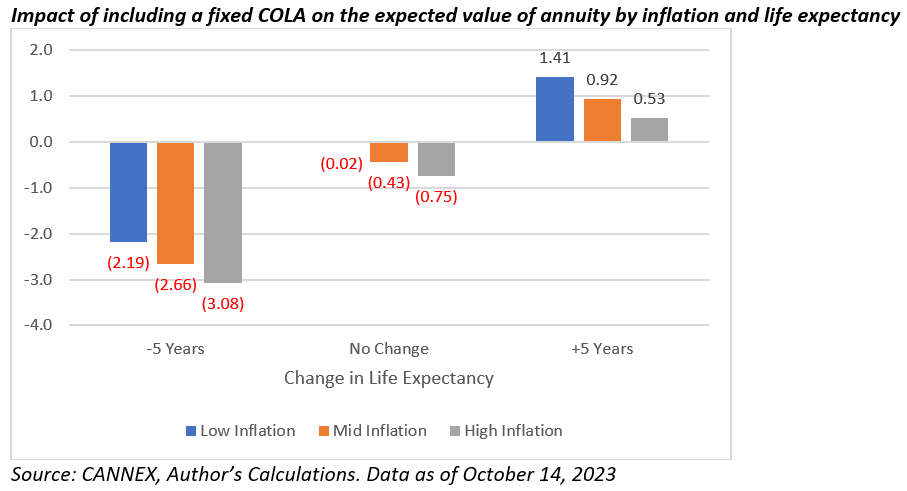

Including a COLA requires larger withdrawals from a portfolio earlier in retirement, subjecting the retiree to greater sequence-of-returns risk. I demonstrate this using an analysis were I assume a future average inflation rate of 2.5% with a standard deviation of 3.0%, using the above annuity payout rates, assuming half of the retiree assets are allocated to the annuity and the other half to a portfolio, which has an average return of 7.0% and a standard deviation of 10.0%, which is roughly consistent with a 50% equity portfolio based on PGIM Quantitative Solutions Q3 2023 capital market assumptions (CMAs). The correlation between the portfolio and inflation is assumed to be .25.

I conducted a 1,000 run Monte Carlo simulation and compared the mortality-weighted net present value of an annuity that included a 2% COLA to one that did not. I grouped the runs by inflation environment (low, mid, and high). Mortality is based on the Society of Actuaries 2012 immediate annuity mortality table with improvement to 2023. I applied various mortality loads to see how different life expectancies impact the values as well.

The expected benefit of including the COLA is negative. This is primarily because the retiree has to deplete the portfolio faster earlier in retirement for the annuity with the COLA due to the lower initial payment. The portfolio has a relatively higher return, which benefits the retiree as well. The COLA does the best only when inflation is relatively low and life expectancies are notably longer.

Conclusions

While nominal annuity COLAs seem like a smart move, my analysis demonstrates otherwise. Most retirees already have guaranteed lifetime income benefits with a COLA explicitly linked to inflation (Social Security’s retirement-income benefits) and given decreases in observed real spending among retirees, the costs associated with adding the COLA need to be considered before including them.

David Blanchett, PhD, CFA, CFP®, is managing director, portfolio manager and head of retirement research at PGIM. PGIM is the global investment management business of Prudential Financial, Inc. He is also an adjunct professor of wealth management at The American College of Financial Services and a research fellow for the Retirement Income Institute.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

More 529/College Planning Topics >

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.