Gundlach: Deficits, Recessions, Unemployment and the Impending Crisis

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits The federal deficit is already high at 6% of GDP. But if a recession hits – as Jeffrey Gundlach fears will happen next year – unemployment will rise, and the deficit and the interest the government pays on it will cripple the economy.

The federal deficit is already high at 6% of GDP. But if a recession hits – as Jeffrey Gundlach fears will happen next year – unemployment will rise, and the deficit and the interest the government pays on it will cripple the economy.

Gundlach spoke to investors via a webcast, which he titled “Norms,” and the focus was on his flagship total-return fund (DBLTX). Slides from that webcast are available here. Gundlach is the founder and chairman of Los Angeles-based DoubleLine Capital.

Gundlach used to frequent a restaurant called Norms in Santa Monica, whose motto was, “We never close.” That was until it was sold in 2013. Societal norms and institutions are thought to be eternal, but he said that will not be the case with the Fed over the next decade, as it faces challenges financing the deficit. Other institutions – the police, Supreme Court, and presidency – will be confronted with similar challenges. Support for those institutions is already at all-time lows, Gundlach said.

“One of the norms we have been living on is debt,” he said, “and that can’t continue.”

The debt-based financing scheme on which the U.S. relies will end, and there will be a better place – a “new turning” – he said. But Gundlach did not say what that would be or how those institutions would evolve.

The deficit dilemma

The federal deficit is 6% of GDP, despite strong GDP growth in the third quarter.

But when there have been recessions, Gundlach said, there have been bigger deficits, especially since 2000.

When a recession has hit, deficits have grown by 5.1% on average. But looking at the last three recessions since 2000, deficits have grown at 9.4%. Growth of 5.1% would mean a $3.5 trillion deficit in four or five years, he said, but using the 9.4% rate means the deficit would be 20% of GDP.

When you look at the deficit alongside the unemployment rate, things become more troublesome. Both have gone up in parallel during recessions, at least until about 2015. Since then, the unemployment rate went down, but the deficit went up.

Gundlach said that if unemployment goes up to 5% (it is 3.9% now), there would be “substantial” deficit expansion.

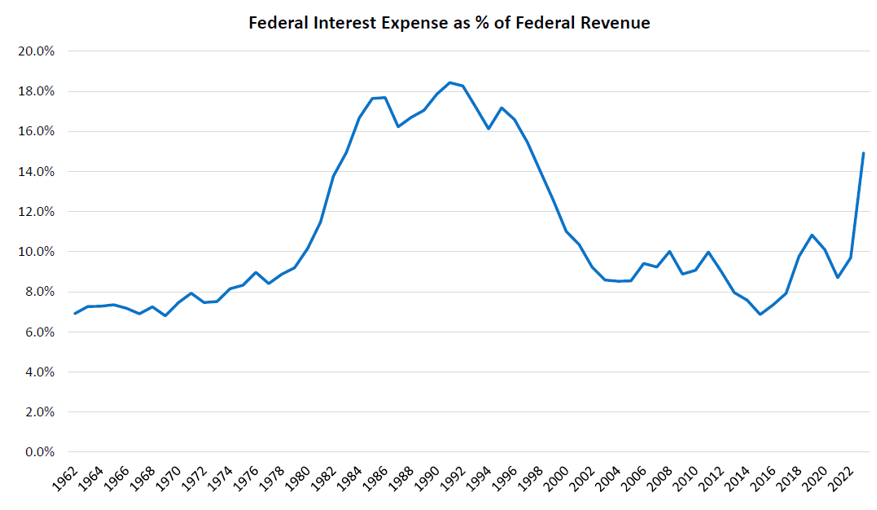

Federal interest as a percentage of revenue is going “vertical,” Gundlach said, because of deficit growth and rising rates. But it was higher in the 1980s, when rates were much higher, as can be seen in the graph below:

The CBO says that federal interest rates will go from 13% to more than 20% of tax receipts over the next decade, but Gundlach said that is based on optimistic assumptions – such as there being no recessions.

The average rate paid on interest on the federal deficit went from 1.42% in early 2022 to 3.10%, and the CBO does not assume further increases in that rate.

Treasury bonds have rallied since late October, Gundlach said. But if the Fed stays with its “higher for longer” policy and rates settle near where they are now, he said there will be more pressure on the deficit.

Is a recession coming?

Various indicators are much “more recessionary looking,” Gundlach said.

The 2-10 yield curve inverts two years prior to a recession and then de-inverts just before a recession starts. Gundlach said that metric reached an inversion of 108 basis points, then the yield curve flattened, but then it re-inverted to 48 basis points. It might de-invert in the next couple of quarters, he said. But for it to be a recessionary signal, it must stay inverted “for a while” and then de-invert.

Historically, the pattern of unemployment suggests we could be in a recession already, he said.

The Philadelphia Fed coincident index is recessionary, Gundlach said. The unemployment rate is a coincident indicator. When its 12-month moving average starts to rise by more than 0.5%, which it has, it signals a recession. The metric that never fails to call a recession is when the unemployment rate surpasses its 36-month moving average. That signal should come in the first or second quarter of 2024, he said.

“There is a probability of a recession coming,” Gundlach said, “and the deficit will be a non-stop problem.” The failure to find a solution to the deficit problem may be why 35 members of Congress are not seeking reelection, according to Gundlach.

The bond market and housing

There is a lot of money “on the sidelines” in money market funds. But he said it will not go to an ARKK- or “magnificent seven-” type of investment. That cash is bullish for Treasury bonds with longer maturities, he said.

Bond yields rose until late October because of a lack of demand, according to Gundlach, but that has changed. Demand from investors seeking higher rates at longer maturities is driving the bond market rally.

As rates rose in the mortgage market, housing supply was curtailed and home prices have gone to a high, exceeding their 2022 levels. If mortgage rates decline to 5.5%, housing supply will increase and prices will deteriorate, Gundlach said.

As mortgage rates rose, the prices of mortgage-backed securities (MBS) fell. Now there is no prepayment risk, he said. “The risk in the agency MBS market doesn’t exist,” he said. “You don’t have to worry about getting paid off early.”

The copper/gold ratio predicts a 2.75% 10-year yield. But as the economy weakened, there has been a rally in bond prices, Gundlach said. But that rally won’t last because of the deficit problems.

Core CPI inflation is 4% and headline is 3.2%, and Gundlach said inflation will remain in the 3% to 4% range into mid-2024. Then inflation will go to the mid-2% level by early summer of 2024.

If you take shelter out of the CPI, inflation is already at 2%. The Zillow rent index leads the owners' equivalent rent component of CPI by a year. The Zillow data suggests a 4% decrease in the shelter component, which means that the CPI will not be inflationary, Gundlach said, supporting the strength in bond prices. The same conclusion can be reached based on the Case Shiller data, he said.

Fed Chair Jerome Powell likes the “super-core” PCE (which excludes the shelter component), and it is already below 4%.

Other metrics, including the headline and core producer prices and export and import prices are non-inflationary.

Supply-chain bottlenecks are gone, he said, based on the NY Fed global supply chain data.

The Fed will not wait for the PCE to be below 2% to begin rate cuts. It is worried about the inverted yield curve and its effect on bank profits. High rates are choking off profitability for small companies as well. That stress will be a factor in the coming recession, Gundlach said, constraining the Fed’s ability to use monetary policy to help the economy.

The monthly mortgage payment for the median sales price of an existing home is $2,300, far higher than at any time in the last 25 years. Housing affordability is very low. Three years ago, it was cheaper to buy, but now it is cheaper to rent except in a few parts of the country.

The pending home sales index is at a 22-year low.

The number of homes under construction, both single- and multi-family, are shrinking. But those numbers are still high, which signals weaker housing prices.

Gundlach touched briefly on commercial real estate (CRE). Multiple sectors comprise the CRE market, and they behave differently. But office space delinquencies have risen to the average for CMBS in general, signaling considerable distress. Delinquencies in most other sectors (industrial, multi-family, lodging, retail) are okay.

Office property delinquencies continue to go up, as many companies are shrinking their employee footprint with buyers there take that space, he said.

Most of the office space CRE loans are owned by banks.

Robert Huebscher is the founder of Advisor Perspectives and a vice chairman of VettaFi.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All