Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

End-of-year planning is all about reviewing the past year’s performance and planning for next year. As you prepare for that planning and gather information to review 2023 and plan for 2024, don’t forget to include healthcare costs, the third-highest expense in retirement, and one of the top five highest expenses for the average American adult. Healthcare costs also impact taxes, and with tax season quickly approaching, now is the time to prepare.

In this article, I'll share the impact healthcare costs have on financial plans, the critical healthcare information to include (such as medical tax deductions and IRMAA), how to budget for costs in a world of variables (there’s no such thing as a planned healthcare crisis), and tangible strategies to implement during open enrollment and beyond to ensure clients are on the optimal coverage.

Why should you care about healthcare costs?

As a financial advisor, it is imperative to include the high expense of health care in financial plans. But aside from cost savings, helping clients plan for healthcare costs differentiates you as an advisor in a competitive and crowded industry, and ensures clients come to you first as a trusted expert in all areas of their lives. Consider that 65% of clients surveyed expected health insurance guidance from their advisor, but only 4% received it. Offering healthcare planning makes you stand out as part of that 4%.

Helping clients plan for healthcare costs creates a more accurate financial plan, helps you attract new clients, and improves satisfaction among current clients.

How can you include healthcare planning in your end-of-year planning strategies?

Next year’s expenses

You can’t plan for unexpected illnesses and procedures, but there are expected healthcare costs you can help clients prepare for by incorporating them into the financial plan. For example, you can include clients’ monthly health insurance premiums in their financial plan. Depending on your clients’ healthcare needs, they may have additional healthcare costs they can plan for proactively. Although you can’t plan for medical emergencies, you can consider what your client’s deductible and out-of-pocket maximum are to determine their potential financial risk should a catastrophic event happen. In addition to monthly premiums, you and your client can also plan for prescription costs, copays, and any planned surgeries or procedures. Including those healthcare costs will give you a more accurate picture of what your client’s expenses are for next year.

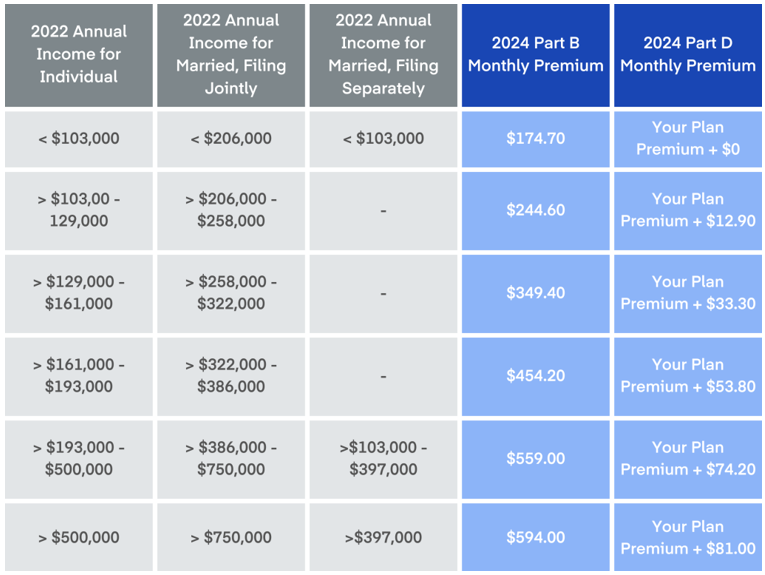

IRMAA

For clients already on Medicare or who are reaching eligibility soon, IRMAA is a factor you and your clients will want to consider. The income-related monthly adjustment amount (IRMAA) is based on a client’s tax filing status, the current year’s adjustment amount, and their modified adjusted gross income (AGI) from two years prior. In 2024, the standard base monthly premium for Part B is $174.90 whereas the monthly premium for Part D varies by plan. For example, to calculate 2024 IRMAA, which is added to these base premiums, the Social Security Administration (SSA) will look at your client’s tax return from 2022. Their Medicare premiums and IRMAA determination are sent to them every year in the fall. Below is a table of expected total costs, which include both the base amount and IRMAA charge:

If your client has a few years until they enroll in Medicare, they might want to take steps now to control their modified adjusted gross income (MAGI) and potentially reduce IRMAA. For clients who aren’t on Medicare yet and can enroll in a high-deductible health plan, one tool to utilize is a health savings account (HSA). I often advocate for HSAs because of the triple-tax advantages they have. HSA withdrawals for qualified medical expenses are tax-free, so using these funds to pay for Medicare premiums, deductibles, and copays can help clients potentially avoid using their taxable income for these expenses. This in turn lowers their taxable income and their MAGI. Using an HSA and saving the contributions for use in retirement is a great strategy to ensure clients have sufficient funds in retirement to cover their growing healthcare needs. The annual pre-tax contributions in 2024 are $4,150 for individuals and $8,300 for families.

Premium tax credits

An area that is often overlooked by advisors is premium tax credits (PTCs), which have been extended into 2025. These tax credits lower monthly premiums for those enrolled in a marketplace plan. Individuals with annual income up to 400% above the Federal Poverty Level (FPL) are eligible for a PTC. States such as California, Massachusetts, New Jersey, and Vermont have enacted state-level subsidies that help out specific populations, too. To be eligible, your client must be enrolled through a marketplace plan and can’t qualify for other programs such as Medicaid and Medicare, or have an employer plan offered to them that covers minimum essential coverage.

There are two ways to claim this credit:

- Claim a monthly advanced premium tax credit (APTC) by estimating income for the coming year. If you over- or underestimate, your client’s premium credit is reconciled when they file taxes for the year.

- PTCs may also be reconciled as a lump sum when they file taxes.

This is often overlooked because advisors don’t realize that the tax credit is a sliding scale that depends on the cost of insurance where the client resides and the size of their household. I’ve seen many clients, even with six-figure incomes, qualify because they live in a state where insurance is more expensive, or they have two or three kids still on their tax return.

Visit this link to learn more about who the marketplace includes as part of your household.

Medical tax deductions

In an ideal world, all clients would annually evaluate if it’s worthwhile to itemize their medical expenses. You can help them determine if they meet the threshold percentage of their AGI to claim these deductions. To itemize medical expenses, your client will need to keep their receipts and document the following:

- Date of transaction;

- Description of items and the amount they paid;

- The entity they paid; and

- Reason for care.

During tax season, you and your client can calculate their AGI on Schedule 1 on their 1040 tax return. Your client will need to know their filing status, total medical expenses, the year their expenses were in, what portion of the expenses were reimbursed (i.e., insurance-covered part of it), and their AGI. They can then add up their medical expenses and calculate their medical tax deduction in Schedule A in their 1040 tax return. An estimate of what they’re able to deduct can be found using the IRS calculator.

Preparing for next year’s open enrollment

At the time of writing this, there were only three weeks left for Medicare open enrollment. Marketplace open enrollment, on the other hand, is much longer; it runs until January 15 for most states. Open enrollment is a great topic of discussion for end-of-year review. Reviewing your clients’ healthcare needs, preferences, and costs from this past year, as well as including those factors for the coming year, will ensure your client is enrolled in the most optimal plan. You wouldn’t set and forget about your financial plan, would you? The same is true of clients’ health insurance plans.

Final thoughts

Healthcare costs take up a major chunk of clients’ expenses. Planning for those costs as best as you can reduces the stress and anxiety many clients feel about healthcare coverage and costs. Being the one to alleviate client concerns around this area leads to better client satisfaction and retention. Plus, there’s an increasing focus on life planning (also known as comprehensive financial planning or holistic financial planning), and health and wellness are major components.

The goal of including healthcare in your end-of-year planning is to make your clients’ lives easier now and throughout the next year, and to create a clearer picture of their finances. The information and strategies in this article will help you achieve those goals.

Christine Simone is a co-founder of Caribou, a company that offers software to financial advisors to plan for and optimize healthcare costs. She often writes on the topics of healthcare and women in tech.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our full schedule of upcoming CE-approved virtual events.

Read more articles by Christine Simone