Advisors who set up recurring withdrawals at TD (e.g., in Veo One) to occur at the beginning of each month, quarter or year need to beware. With the transition to Schwab, those scheduled January withdrawals will take effect in December instead. In IRAs, this may mean the withdrawal will apply to the wrong tax year (2023 instead of 2024) and will not count toward 2024 RMDs as expected.

Advisors who set up recurring withdrawals at TD (e.g., in Veo One) to occur at the beginning of each month, quarter or year need to beware. With the transition to Schwab, those scheduled January withdrawals will take effect in December instead. In IRAs, this may mean the withdrawal will apply to the wrong tax year (2023 instead of 2024) and will not count toward 2024 RMDs as expected.

Background

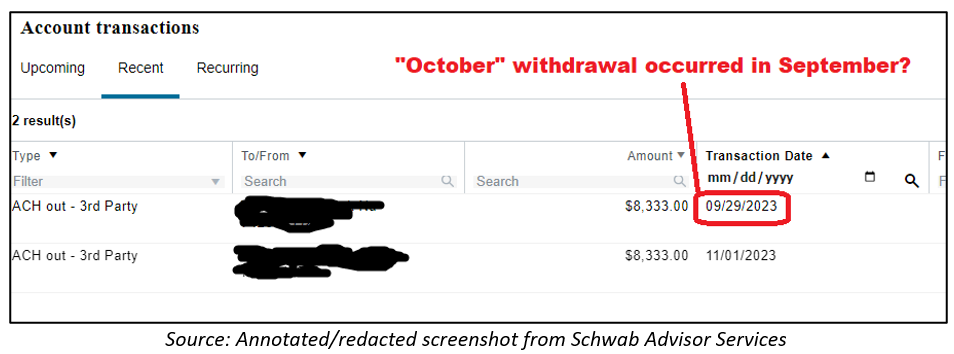

Recently, I was working on a “Move Money” operation on the Schwab Advisor Center website, when I noticed something odd about a recurring monthly withdrawal for one of my clients. We had set up a monthly draw from one of her portfolios, and in Veo we had specified that the withdrawal effective date be the first business day of each month. Yet it seemed her “October” withdrawal had an effective transaction date of September 29.

Further sleuth work revealed that multiple other clients’ October withdrawals had effectively occurred in September as well. As it turns out, this oddity was caused by a combination of (1) October 1 falling on a weekend, and (2) a difference between how Schwab Advisor Center (SAC) and TD’s Veo system handle business days in Move Money calculations.

Specifically:

- In TD/Veo, you would specify the “effective date” of a recurring withdrawal (e.g., the first of each month). In the event of weekends or holidays, the system would move the withdrawal to the first subsequent business day (e.g., 10/2/2023), in which case the “completion date” – when the money settles in a client’s bank account – would be the next business day thereafter (e.g., 10/3/2023).

- In SAC, it is the completion date that is anchored in the system, and in the event of a holiday, the effective date moves forward to the first available business day (e.g., 9/29/2023).

Either system is fine in theory. Specifically, TD’s system favored beginning-of-month withdrawals, while Schwab’s system works best for end-of-month withdrawals. The problem arises from transitioning recurring transactions from the former system to the latter.

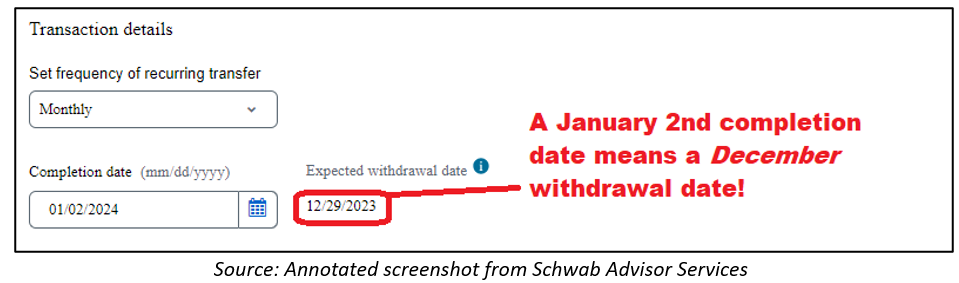

It seems that when the Labor Day cutover was finalized, recurring transactions were migrated to SAC with a “completion date” one day later than the “effective date” that was set in Veo. This sounds like a reasonable migration rule, but it had unintended consequences. Most notably, recurring transactions set in Veo to the first day of a month/quarter/year now have a completion date of the second day. But since January 1 is always a holiday, this means such transactions will always go effective in the prior year. The worst-case scenario would be a year in which January 1 is a Saturday, in which case even a completion date of January 4 would result in a 12/31 effective date.

This is most troubling with respect to withdrawals from IRA accounts. If monthly, quarterly, or (heaven forbid) annual withdrawals expected to occur in January are in fact credited in December, then:

- The withdrawals will be taxable in the 2023 tax year, instead of 2024 as intended.

- The withdrawals will not count toward 2024 RMDs, potentially requiring additional withdrawals in 2024 beyond what was intended.

What can be done?

Thankfully, this issue is avoidable. The first step I would suggest is to…

Contact Schwab

A very helpful member of the Schwab advisor services team spent nearly an hour on the phone with me, working through the details of this issue, both to ensure I wasn’t just missing something and to talk through workarounds. He also said he would raise this problem with his superiors, and I trust he did.1

I also sent a message through Schwab’s “service request” portal, alerting them to this problem.2 To this I received the following tremendous response:

Might this highly informative reply indicate that Schwab is aware of the issue and has plans to fix it? Um…that’s one possibility, I suppose…

Barring that, though…since this issue risks catching numerous advisors unaware, the best solution is for Schwab to fix it. My hope is that if more – and, let’s face it, larger – RIAs raise this issue, perhaps it will merit genuine attention before it’s too late.

But now that you know about it, you can also…

Spread the word

This is a problem we can fix on the advisor end (see below). But Schwab advisors need to be made aware of it. We can do our professional colleagues a favor and offer them a heads-up lest this issue that threatens to snag their clients. Forward this article to anyone you would like to help.

And finally, we can…

Work around the problem

Given the apparent degree of “urgency” conveyed by the Schwab team’s response to my inquiry, it is incumbent upon us as advisors to sidestep this issue ourselves. The first requirement for fixing the problem is to identify all the client accounts which it affects.

Your circumstances may differ, but here’s what my firm, Round Table Investment Strategies, was able to do to fix the problem on our end in SAC.

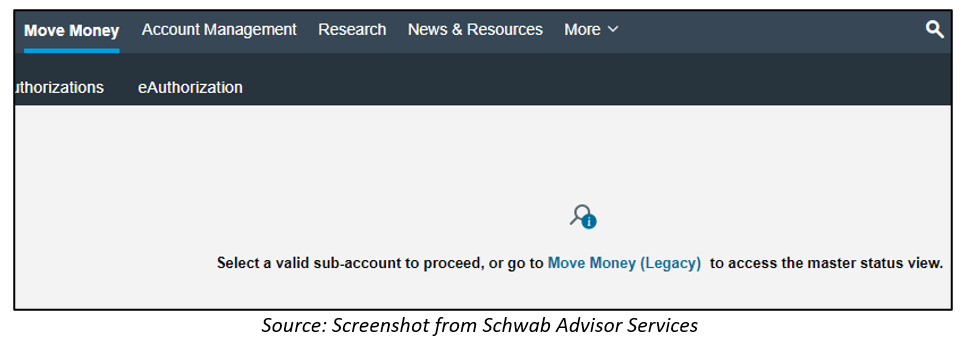

With our master account selected, we clicked on the “Move Money” menu item, which provided us with a link to “Move Money (Legacy)”:

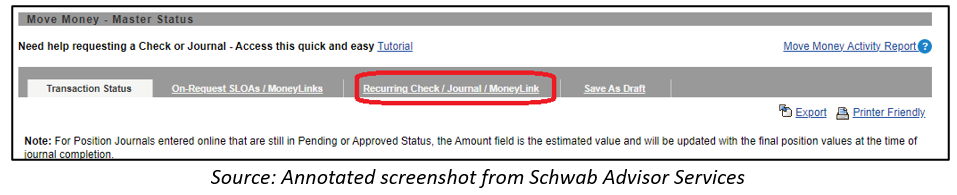

In the legacy Move Money screen, we clicked the “Recurring Check / Journal / MoneyLink” link:

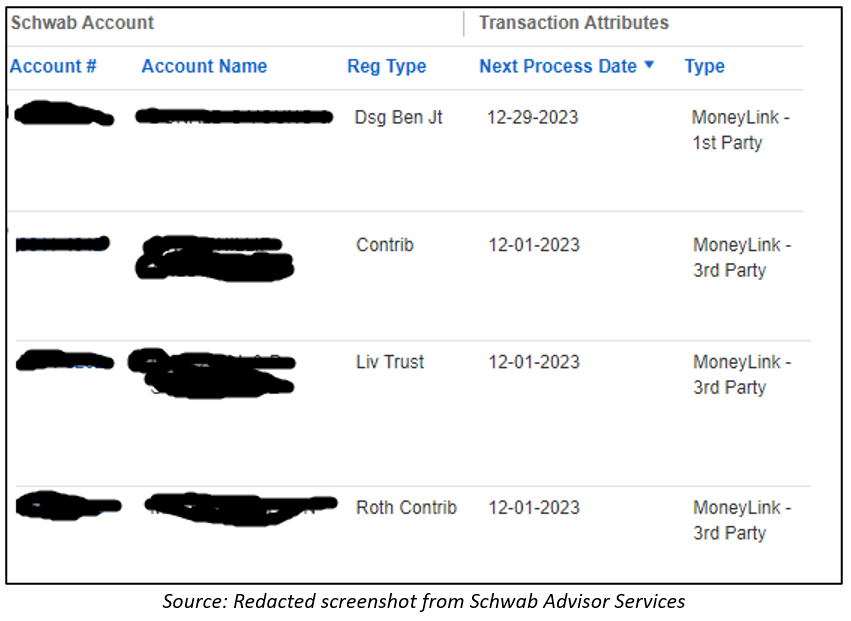

The resulting table helped us locate accounts that may be affected.

For example, the second, third, and fourth rows in the above image are monthly withdrawals that will likely creep into December when the January instance rolls around. The first row is a quarterly draw, where we can already see that the “Q1” withdrawal will be errantly processed on 12/29/2023. Then again, only the second row is a “Contrib” account (encoded Schwab-ese for an IRA), so opinions may vary as to whether the other three need to be addressed at all.

For accounts that do need to be addressed, there are a few options:

- We could move the recurring transaction from a completion date of January 2 to a completion date of February 2,3 and create a one-time draw on January 3. This process would need to be repeated annually unless/until Schwab modifies its system.

- We could move the recurring transaction completion date to the third day of the month. This will work this upcoming January, but we’d need to stay alert in subsequent years, when the weekend/holiday schedule may require it to move back further. Problematically, this would mean our clients would receive their cash flows somewhat later than they are used to from now on.

- What we settled on is to schedule a one-time withdrawal with a completion date of 1/3/2024 and then switch the recurring withdrawal on affected accounts to an end-of-month cycle, starting at the end of January. This effectively replaces an “early February” draw with a “late January” draw, etc. – a permanent solution that will minimize disruption for our clients by moving their scheduled cash flows forward slightly. We will also recalculate RMD schedules, etc. to account for the intentional decision to have 13 distributions in 2024 to solve the problem in all subsequent years.

Whatever solution you choose, be sure to double-check that the resulting scheduled withdrawal dates are as you expect. (Hopefully, it goes without saying that I and my firm can take no responsibility for any outcomes.)

Good luck and best wishes for a happy, gotcha-free New Year!

In his role as chief investment officer for Round Table Investment Strategies, Nathan Dutzmann is responsible for applying financial science and investment research to the process of constructing portfolios tailored to our clients’ individual needs and goals. Nathan was previously an investment strategist with Dimensional Fund Advisors and a partner and chief investment officer with Aspen Partners. He holds an MBA from Harvard Business School and a master’s degree in international political economy and a bachelor’s degree in mathematical and computer sciences from the Colorado School of Mines.

1 Unlike subsequent paragraphs, this is entirely serious and sarcasm-free. The guy was great to work with.

2 So none of this “You should have talked to us first before whining in public” stuff!

3 For monthly withdrawals; April 2 for quarterly.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

Read more articles by Nathan Dutzmann

Advisors who set up recurring withdrawals at TD (e.g., in Veo One) to occur at the beginning of each month, quarter or year need to beware. With the transition to Schwab, those scheduled January withdrawals will take effect in December instead. In IRAs, this may mean the withdrawal will apply to the wrong tax year (2023 instead of 2024) and will not count toward 2024 RMDs as expected.

Advisors who set up recurring withdrawals at TD (e.g., in Veo One) to occur at the beginning of each month, quarter or year need to beware. With the transition to Schwab, those scheduled January withdrawals will take effect in December instead. In IRAs, this may mean the withdrawal will apply to the wrong tax year (2023 instead of 2024) and will not count toward 2024 RMDs as expected.