Managing Taxes in Retirement using the Effective Marginal Tax Rate

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits

Two corrections were made to this article on November 15, 2023: The first is that Exhibit 6 was not included, and it now appears in the article. The second is that the title for exhibit 9 should say RMD instead of IRA.

Research on tax-efficient retirement distribution strategies aims to sequence withdrawals from taxable, tax-deferred, and tax-exempt accounts to maximize after-tax spending. That can be either in terms of meeting an after-tax spending goal for as long as possible or preserving the most after-tax legacy after meeting spending needs over a specified timeframe.

We will simulate different strategies to determine which strategy provides the greatest tax efficiency in terms of supporting the most after-tax spending and legacy for retirees. We focus on how to source retirement spending needs as well as deciding whether to generate additional taxable income through Roth conversions.

The challenge is not just balancing taxable income over time in the face of our progressive federal income tax brackets, but managing the potential large tax impacts of important nonlinearities in the tax code that can cause effective marginal tax rates to wildly diverge from the federal income tax brackets. We will investigate how retirees can create efficiency in the face of these nonlinearities:

- The Social Security “tax torpedo” applies when an increase in taxable income uniquely causes a greater percentage of the Social Security benefit to become taxable.

- Preferential income sources (qualified dividends, long-term capital gains) stack on top of ordinary income and have their own tax schedule. An increase in ordinary taxable income can uniquely push preferential income into higher tax brackets.

- An increase in taxable income above certain thresholds triggers increases to Medicare Part B and Part D premiums two years later (called Income-Related Monthly Adjustment Amounts, or IRMAA).

- The net investment income tax (NIIT) applies when investment income exceeds relevant thresholds.

Numerous resources are available that explain the specifics of these tax non-linearities. For those seeking further background on this, we suggest reading Chapter 10 of Pfau’s Retirement Planning Guidebook.

We begin with an overview of a unique methodology for identifying tax-efficient distribution strategies. We refer to it here as the “effective marginal rate” (EMR) methodology. It uses “tax maps” within each year to track the effective marginal tax rate on each dollar of ordinary income, including the non-linearities above.

We then analyze two tax planning strategies. The first is the conventional wisdom. The conventional retirement strategy is to spend taxable assets first, then tax-deferred (IRA) assets, and then tax-exempt (Roth IRA) assets. This serves only as the baseline, as there is wide consensus that more tax-efficient distribution strategies are possible, including the strategic use of Roth conversions.

The answer for creating tax-efficiency beyond the conventional approach generally involves spending from a blend of taxable and tax-deferred assets to meet expenses and to potentially make Roth conversions to generate more taxable income beyond what is needed to cover current spending, while taxable assets remain. Once taxable assets deplete, the retiree then shifts to spending a blend of tax-deferred and tax-exempt assets to control the amount of taxable income and taxes, which might also include Roth conversions, in a manner that allows for the greatest after-tax spending and legacy potential for investment assets. The challenge, though, is how to develop specific guidelines for managing this process.

The EMR method for developing tax-efficient withdrawal strategies

At Covisum, Elsasser pioneered the use of tax maps combined with an effective marginal tax rate method for determining efficient retirement distributions.

The methodology begins with a recognition of any unavoidable ordinary income, including pensions, interest from taxable savings and bonds, earned income, and RMDs, in addition to any unavoidable preferential income, such as qualified dividends. Social Security benefits fall into a peculiar category, as the tax is driven not just by the amount of Social Security income, but also the amount of ordinary income, some tax-free income, and preferential income.

Once the unavoidable income amounts are established, the retiree’s decision is how much additional ordinary income in the form of IRA withdrawals or Roth conversions should be recognized in any tax year. To guide that decision, Covisum introduced the concept of a tax map that tracks the effective marginal tax rate on each dollar of ordinary income. The EMR was used instead of the more common “marginal rate” to reflect the fact that many non-linearities relevant to financial decision making are not technically taxes. The glaring example for retirees is IRMAA surcharges, but ACA premium subsidies and homestead exemptions from real-estate taxes are similarly relevant and could not be considered as an income tax liability (IRMAA is considered in this article and in Covisum’s current model, but ACA subsidies and homestead exemptions are not).

The EMR methodology considers each dollar of potential withdrawal from IRA accounts or Roth conversions as desirable or undesirable, based on whether the dollar can be taken below a target EMR. If the next dollar would experience an EMR above the target EMR, it is considered undesirable.

The tax map demonstrates that effective marginal tax rates can increase or decrease with additional dollars of ordinary income, such that just because a tax target is initially reached doesn’t necessarily mean that one should stop generating taxable income. There are situations in which an undesirable dollar must be taken to access a larger pool of desirable dollars.

We consider an example of a tax map used in conjunction with two different EMR targets to explain better how this methodology works. The tax map in Exhibit 1 is created for a couple over age 65 using married filing jointly status in 2023. They receive Social Security benefits worth $52,200 and unavoidable preferential income of $20,000 through taxable investment accounts. Their tax map shows multiple discrete increases and decreases related to federal income tax brackets, the taxation of Social Security income, the stacking of preferential income on ordinary income, the 3.8% NIIT, and multiple potential IRMAA surcharges.

Including only their unavoidable income, their taxes are still $0 as they still have excess capacity within their standard deduction, and their stacked preferential income is well below the 15% threshold. Once their deduction is used, the EMR is immediately 18.5% as they face the 10% bracket and are in the portion of the Social Security tax torpedo in which $1 of income generates tax on 85% of each dollar of Social Security benefits. They are still in the tax torpedo when they enter the 15% federal bracket, such that the EMR then increases to 22.2%. The EMR falls to 12% briefly after Social Security achieves full 85% taxation. But then the EMR increases to 27% as stacked preferential income is pushed from 0% to 15% as more income is achieved in the 12% federal bracket. The EMR briefly falls to 12% before the 22% federal income bracket kicks in. After this point, in terms of the ordinary income levels shown in the exhibit, they face multiple IRMAA surcharges, an increase in the federal income tax bracket to 24%, and then an EMR of 27.8% when the NIIT is applied to their preferential income.

So how much additional ordinary income should they generate through IRA distributions to either cover spending needs or as Roth conversions? There are three income levels in which the EMR shifts from less than (or equal to) the 15% target to more than 15%. When ordinary income (not including the taxable portion of Social Security) reaches $12,386, they face the tax torpedo. When ordinary income reaches $55,579, they must deal with preferential income stacking. When ordinary income reaches $75,779, they reach the 22% federal income tax bracket. Which of these income bands can they reach without exceeding a 15% EMR on that chunk of income? In this example, the first chunk of income can be reached at a 0% EMR and is desirable. But neither of the opportunities to increase ordinary income to a higher amount allow for an EMR that is less than the target. Increasing ordinary income from $12,386 to $55,579 faces an EMR of 18.2%; increasing from $12,386 to $75,779 results in an EMR of 21%. The best decision to make in conjunction with a 15% EMR target is to generate $12,386 of ordinary income through IRA distributions.

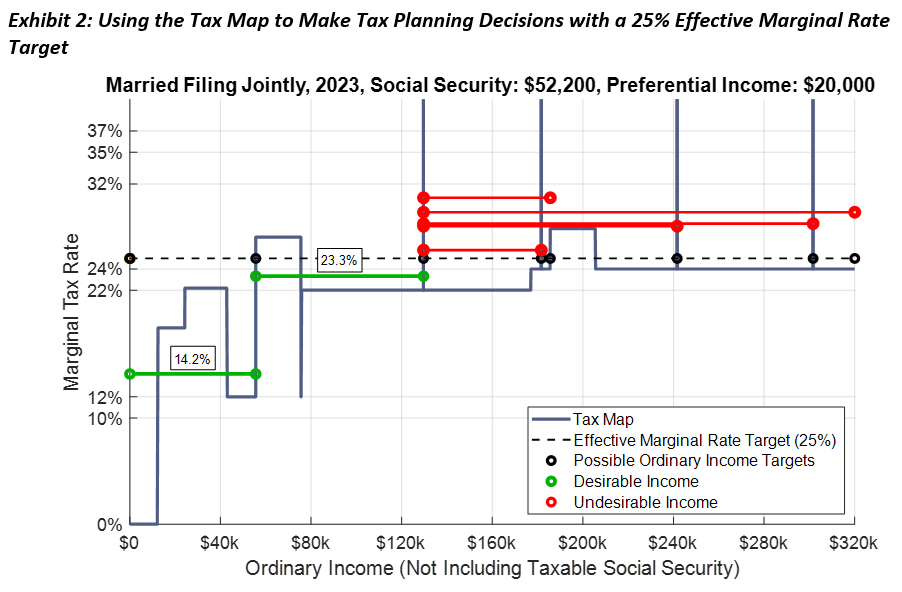

For further understanding, we will also describe how the decisions are made if the EMR target were instead equal to 25%. In Exhibit 2, we can see there are more points where the EMR shifts from less than (or equal to) 25% to more than 25%. It happens when preferential income stacking begins, with each of the four IRMAA surcharges shown in the exhibit, and when the NIIT begins to apply. We want to test which of these income segments are desirable in the sense of allowing for the income generated to be taxed at an EMR under 25%. Generating the first segment of ordinary income in its entirety through $55,579 is desirable, as its EMR for the segment is 14.2%.

Next, we check the income segment between $55,579 and $129,629, where the first IRMAA threshold is reached. This income segment is also desirable, as it is taxed at an EMR of 23.3%. Beyond this point, generating more taxable income is undesirable. Any increase from this point to where the EMR shifts from less than 25% to more than 25% results in an average tax rate on that segment of more than 25%, as illustrated by the additional red lines in the exhibit positioned at the amounts of the taxes. In this case, the recommended course of action to maintain a 25% EMR target is to generate ordinary income up to the threshold that would trigger the first IRMAA surcharge.

The IRMAA charge is illustrated as a spike to greater than 100%, because the charge is not phased in and is instead applied in its entirety when a threshold is reached. In the absence of other circumstances, no rational person would withdraw a dollar that costs more than a dollar in taxes. But in this case, there are other circumstances. Immediately after the IRMAA threshold is crossed, the EMR drops back under 25% again as the 22% federal bracket resumes. Nonetheless, IRMAA surcharges can be difficult to overcome, as is the case here. Since the effective marginal tax rate didn’t have the opportunity to fall to 25% again after the IRMAA surcharge, it means that the optimal distribution is to generate IRA distributions up to just under the point of the first IRMAA surcharge would apply, avoiding the surcharge. To be clear about the IRMAA surcharge, though it will impact Medicare premiums two years later, we create the tax maps with it included in the current year for the purposes of determining the average effective tax rates when generating additional income.

This methodology considers all the points where the effective marginal tax rate shifts from below to above the targeted threshold and accounts for any situation where it again drops below the target.

Comparing the EMR method to conventional wisdom

Now that we’ve established the methodology for determining a withdrawal amount from the IRA, we will shift to a comparison of the EMR methodology with different EMR target rates to the conventional wisdom strategy to quantify the positive impact these approaches have on the after-tax legacy value of assets at age 95.

Portfolio distributions will include Roth conversions and use a blended strategy that mixes taxable and tax-deferred distributions at first, and then tax-deferred and tax-free distributions later, to provide control over the effective marginal tax rate. The couple first takes any RMDs from the IRA, which begin at age 75. If Social Security benefits and RMDs from the IRA exceed the desired spending level and taxes due, then any surplus is added as new savings to the taxable account. More commonly, if RMDs and Social Security benefits are less than the desired spending and federal income taxes due, additional withdrawals are first taken from the taxable account until empty, then from the IRA account until the target tax rate is reached, then from the Roth IRA. If the spending need is met by withdrawals from the taxable account or a combination of the taxable account plus IRA withdrawal, but additional funds may be withdrawn under the EMR target, those funds are converted to Roth.

Taxes on these additional IRA distributions and conversions are paid through further distributions from the taxable account when possible, or otherwise from the tax-deferred account after the taxable account depletes. Distributions are taken at the start of each year. This algorithm leads spending strategies to be a blend of taxable and tax-deferred IRA assets while taxable assets remain, and then a blend of IRA and Roth IRA assets.

Financial market returns

This analysis is based on simple financial return assumptions. In this article, we assume an overall portfolio return of 5.06%. This consists of a 3% inflation assumption and a 2.06% real return. Asset allocation is not directly relevant other than to manage the breakdown between interest income and qualified dividends to determine income distributions from the taxable portfolio. We assume a portfolio of 60% stocks and 40% bonds, with a dividend yield of 3% (matching inflation) and a bond yield of 5.06%. The remainder of returns for stocks reflect long-term capital gains.

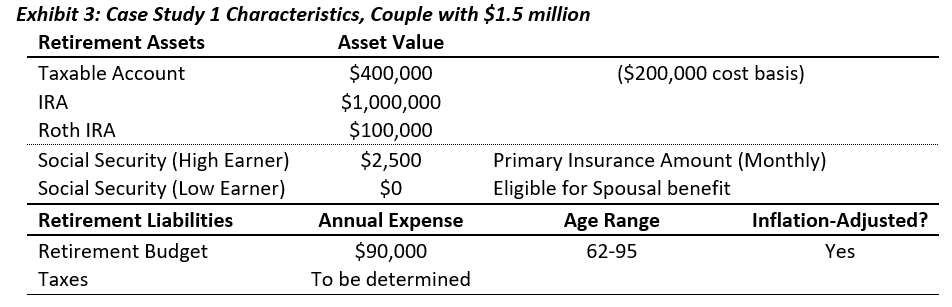

Case study 1 details

We consider a mass affluent couple with $1.5 million of investment assets. Both individuals are age 62 and are assumed to be born on January 1. For simplification, the start date for this analysis is the start of 2023, so that we do not have to pro-rate numbers in the first year. For their retirement finances, the priority is to build a financial plan that will cover their spending goals through age 95. When meeting spending goals, a secondary priority is to maximize the after-tax surplus of wealth for their beneficiaries at age 95.

Their financial details are provided in Exhibit 3. Retirement assets include $400,000 in a taxable brokerage account (with a $200,000 cost basis), $1,000,000 in a tax-deferred IRA, and $100,000 in a tax-free Roth IRA. For simplification, this household has one wage earner whose Social Security primary insurance amount is $2,500 monthly. Both spouses will delay claiming until age 70, which provides a 24% benefit increase through the delay credits for the worker, but not the spouse, allowing for a combined $52,200 per year in 2023 dollars. Annual cost-of living adjustments are assumed to match the 3% inflation rate.

The projected core annual retirement expenses for the couple equal an inflation-adjusted $90,000 throughout retirement. They live in a state with no income tax. This couple rents their home in retirement to avoid the additional complications associated with managing home equity in the retirement plan.

They must pay federal income taxes – an additional expense that will be estimated beyond these spending goals. We calculate taxes on the portfolio distributions, including qualified dividends, interest, and long-term capital gains from the taxable account, the ordinary income generated from IRA distributions, the precise amount of taxes due on Social Security benefits, any Medicare premium surcharges if modified AGI exceeds the relevant thresholds, as well as any potential net investment income surtaxes due. These taxes are calculated based on the tax law in 2023, including the shift to higher tax rates in 2026 that is part of the sunsetting provisions in current law, as well as the new RMD life tables introduced in 2022. Tax brackets increase with inflation, though the thresholds for determining taxes on Social Security and the net investment income tax are not inflation adjusted. This couple uses the standard deduction instead of itemizing.

The legacy value of assets reflects the real after-tax value of investments remaining at age 95 in 2023 dollars, using the inflation rate as the discount rate. Taxable assets receive a step-up in basis at death, providing their full value for heirs. Tax-deferred assets maintain their embedded income tax liability after death. We assume that adult children will be beneficiaries, and the SECURE Act requires them to spend down the account within a 10-year window when they may still be in their peak earnings years and face higher tax rates. To reflect this, we assume that remaining tax-deferred assets will be taxed at a 25% rate to reduce their legacy value to heirs. Tax-free Roth assets also face the same distribution requirements, but they will not be taxable to heirs, so their full value passes as legacy.

If the entire spending goal cannot be met over the retirement planning horizon, we calculate the spending shortfall relative to the goals as a negative legacy. Only Social Security remains to cover a portion of spending if investments deplete. But this case study was designed so that all strategies considered were able to meet the full lifetime spending goal.

Results for case study 1

The results proceed in two stages. First, we seek to determine the EMR target for the effective marginal tax rate strategy that provides the best outcome and confirm that this outcome provides an enhancement over the conventional wisdom. Then we provide a detailed comparison between the tax-efficient strategy and the conventional wisdom to better explain how tax planning can improve retirement outcomes.

Exhibit 4 shows the after-tax legacy value of assets for different strategies in inflation-adjusted levels (all monetary values are defined as real 2023 dollars). We investigate different fixed EMR targets, including cases where the tax target approaches but does not include the tax rate, keeping spending out of that tax bracket when feasible, as well as when the target does include that tax rate to allow for movement through the tax bracket when feasible. The conventional strategy results in the worst outcome. It supports a legacy of $37,474 after meeting spending goals. The EMR target supporting the best outcome is to manage 15% as the upper limit for desirable income generation. This supports $159,599 of real legacy. When we calculate the internal rate of return on after-tax spending and legacy supported by these strategies, we find that the conventional wisdom supported a net 4.17% after-tax return. Taxes reduced returns by 0.89%. For the best performing strategy, the net after-tax return was 4.58%, which is an improvement of 0.41% over the conventional wisdom. This can be interpreted as the additional tax alpha generating by a more efficient strategy compared to the conventional wisdom.

The next set of exhibits compares characteristics of the conventional wisdom strategy and the tax-efficient strategy. First, Exhibit 5 shows the dollar amount (in real 2023 dollars) of the Roth conversions made at each age. For the tax-efficient strategy, the last of the taxable account is spent at age 66, and Roth conversions are made consistently at their largest value until this time. Once the taxable account is depleted, there is more pressure on the tax-deferred account to support spending needs first, but there is some capacity for Roth conversions at age 67 to 69. Once Social Security benefits begin at age 70, there are no further opportunities for Roth conversions.

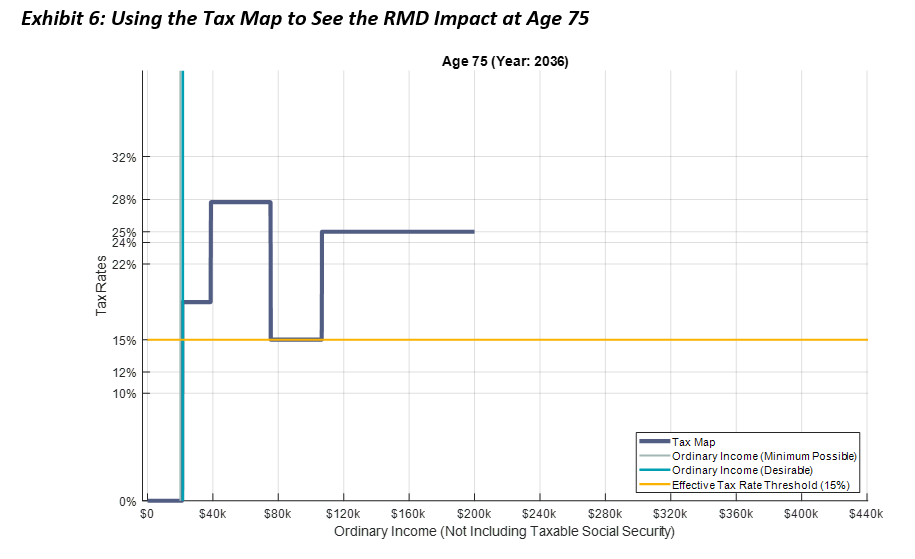

In terms of the tax maps, the behaviors throughout retirement that align with the use of a 15% EMR target are as follows. First, for ages 62-66 when the taxable account remains, ordinary income is generated until the point that preferential income stacking (from 0% to 15%) begins, which raises the effective marginal tax rate to 27%. Then, for ages 67-69, ordinary is generated through the end of the 15% federal income bracket (which is assumed to return in 2026). For ages 70-74, ordinary income is generated to fill the standard deduction. Any further income generation leads to an effective marginal tax rate of 18.5%, reflecting the impacts of the tax torpedo in the 10% federal bracket. Exhibit 6 below demonstrates that once RMDs begin at 75, it is no longer desirable to generate any further ordinary income for the remainder of retirement, as the couple is already immersed in the highly taxed Social Security tax torpedo. Fortunately, with this tax planning the couple has created a large enough Roth IRA so that it can support the remaining spending needs.

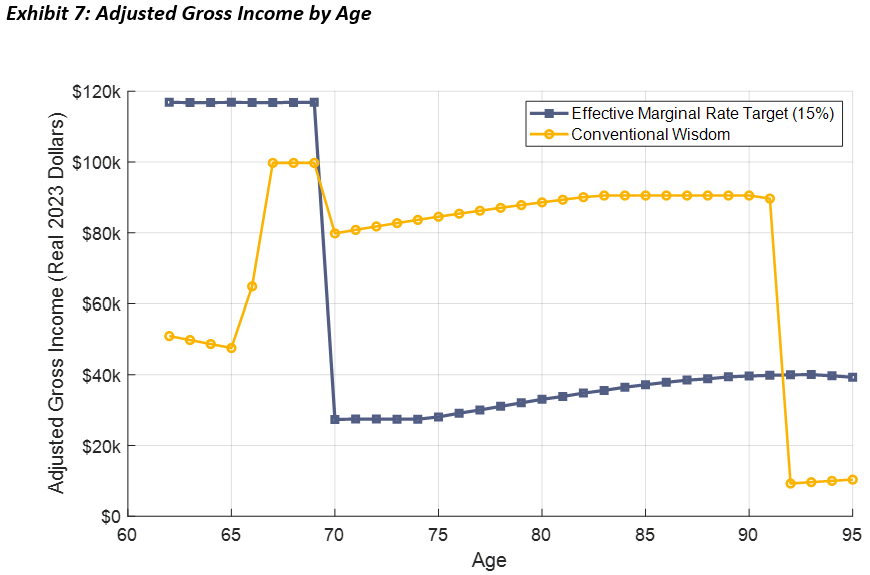

Next, we continue to look at features of the tax-efficient strategy compared to the conventional wisdom. Exhibit 7 shows the adjusted gross income (ordinary plus preferential income) at each age with these two approaches. In this case study, with no above-the-line deductions, total income is equivalent to adjusted gross income (AGI). Compared to the conventional wisdom strategy, the tax-efficient strategy front-loads taxable income to the years before Social Security begins. This lays the foundation for subsequent AGI to be less, at least until age 92 when the convention wisdom strategy depletes the IRA. Roth distributions then supplement Social Security, leaving a portion of Social Security as the only source of taxable income.

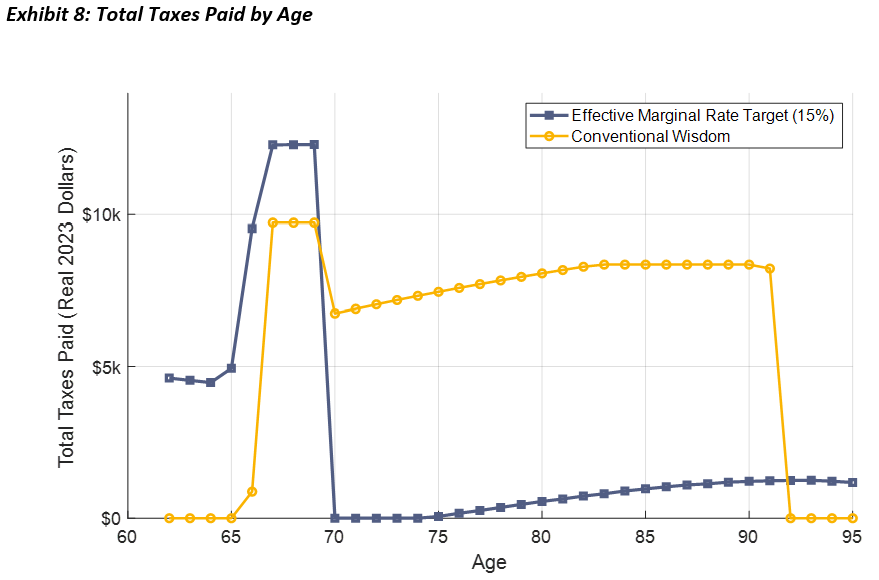

Exhibit 8 next shows the total taxes paid for each retirement year. With the conventional wisdom, taxes are $0 while the taxable account remains because interest income is less than the standard deduction and preferential income remains within the 0% bracket. But taxes increase dramatically when spending is covered through the IRA. There is a reprieve at age 70 when Social Security reduces the IRA distribution, and because not all Social Security is taxed. The reason taxes tilt upward after this relates to how the Social Security taxation thresholds do not adjust for inflation, so an increasing percentage of Social Security is taxed over time until it reaches 85%. Then taxes drop once the IRA depletes. This is compared to the tax-efficient strategy, which frontloads taxes in the years before Social Security begins and is then able to dramatically reduce subsequent tax bills in a manner that we showed can dramatically increase after-tax legacy values.

Exhibit 9 illustrates the RMDs by age. The tax-efficient strategy can keep them more level, while the conventional wisdom picks up on the pattern that the IRA balance is still much higher when RMDs begin but is reduced more dramatically as the IRA covers all spending not supported through Social Security.

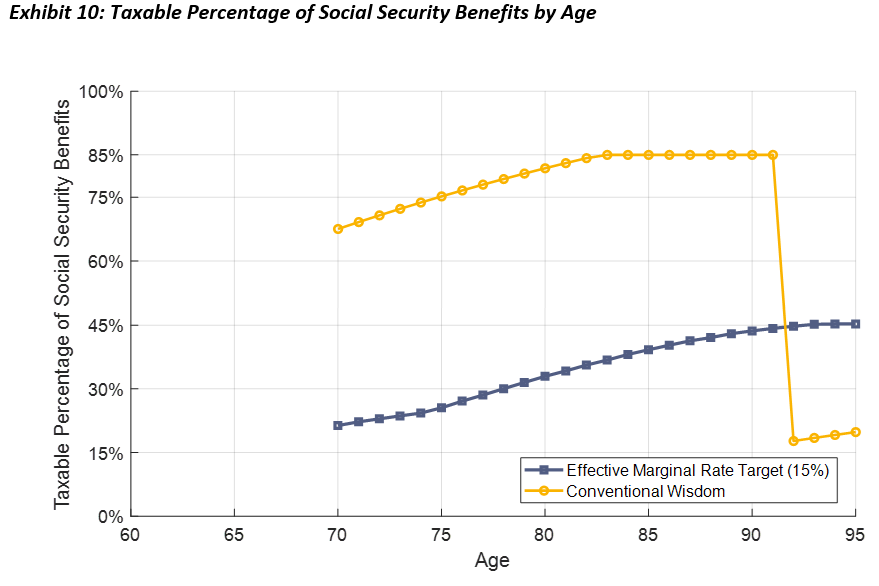

Next, Exhibit 10 partly demonstrates how the tax-efficient strategy provides greater financial benefit through its frontloading of taxes. In this case study, the upfront taxes paid help to reduce the taxable amount of Social Security benefits received by the household quite dramatically in retirement. This has a significant impact on reducing taxable income and tax bills for the household.

Exhibit 11 provides more insight into the strategy’s actions. For the conventional wisdom, it’s simply a matter that the tax bracket is 0% in years that spending is supported through the taxable account or the Roth IRA, and the couple ends up in the 15% bracket in years that spending is supported through the IRA. As for the tax-efficient strategy, for ages 62 to 66, ordinary income is managed up to the point that the preferential income sources would begin to be taxed at 15%. This happens to be at a point when ordinary income falls into the 12% and then the 15% tax bracket. Then for ages 67 to 69, taxable assets are depleted, and the couple is no longer burdened by the impact of stacking preferential income. They now generate ordinary income through the end of the 15% bracket. Once Social Security begins at 70, this couple will be burdened by the Social Security tax torpedo for the remainder of retirement, leading to limits on income generation through the tax-deferred account. For ages 70 to 74, the couple remains in the 0% tax bracket as any additional income above the standard deduction would be taxed at an 18.5% marginal rate with Social Security’s impact included, pushing them above the 15% target. After age 75, RMDs force the couple into the 10% tax bracket, but they avoid generating additional income because they are still positioned firmly in the Social Security tax torpedo with high effective marginal tax rates applied to any additional income. With the tax-efficient strategy, this couple acts to avoid taxation on their preferential income in the early years and then to avoid the full impact of the Social Security tax torpedo after age 70. They were not constrained by IRMAA or the NIIT in this case study.

Finally, Exhibit 12 makes clear that the differences in legacy for the tax strategies are not only at age 95. The tax-efficient strategy supports more after-tax legacy than the conventional-wisdom strategy throughout the entire retirement horizon. This can be understood with a reminder about how after-tax legacy is calculated. Taxable and Roth IRA assets pass tax free, but we assume any remaining IRA assets are taxed at 25%. Since the tax-efficient strategy begins Roth conversions at age 62 and keeps the effective marginal tax rate on these conversions under 15%, it begins to immediately support a higher after-tax legacy.

The bottom line

This case study shows the potential value for tax planning in retirement to improve results for clients and create tax alpha through strategic effective-tax-rate management.

Wade D. Pfau, PhD, CFA, RICP® is a co-founder of the Retirement Income Style Awareness tool, the founder of Retirement Researcher, and a co-host of the Retire with Style podcast. He also serves as a principal and the director of retirement research for McLean Asset Management. He also serves as a research fellow with the Alliance for Lifetime Income and Retirement Income Institute. He is a professor of practice at the American College of Financial Services and past director of the Retirement Income Certified Professional® (RICP®) designation program. Wade’s latest book is Retirement Planning Guidebook: Navigating the Important Decisions for Retirement Success.

Joe Elsasser, CFP® is the founder and president of Covisum, a financial planning software company focused on retirement income related decisions and is a founding partner of Adaptive Advice, a Registered Investment Advisor. He co-authored Social Security Essentials: Smart Ways to Help Boost Your Retirement Income and has been a frequent contributor to a variety of industry publications.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All