Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

With the race to year-end now upon us, I share my thoughts on why, despite the recent reset and higher rates, I still see several reasons for market optimism for the remainder of the year.

My top five ideas are: distressed private credit, buyout private equity, opportunistic real estate, macro hedge funds, and structured investments.

1. Private credit: Distressed investing

After the steep rise in interest rates in 2022 and the first half of 2023, and with the Fed funds rate increasing to its highest level since July 2007,1 companies are facing the prospects of higher interest payments. As a result, over-levered companies are now encountering a difficult environment to service or refinance their debt. This creates the potential for an increase in the number of defaults for the remainder of 2023 and into 2024.

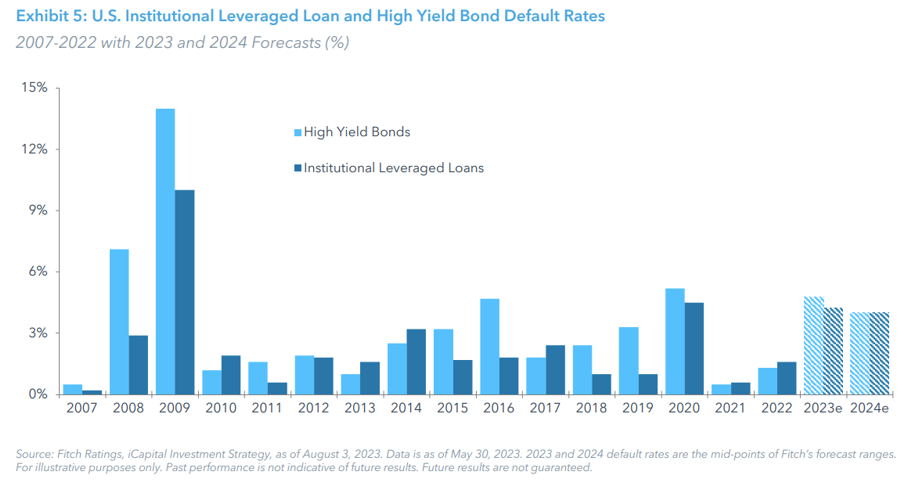

Signs of credit stress are already emerging, with the failures of several regional banks, highlighting the potential effect of increasing and elevated interest rates. Cracks in regional banks also have serious knock-on effects as lending standards tighten across the financial system, making refinancing maturing debt difficult for highly levered companies. In addition to the recent stress and uptick in defaults, Fitch Ratings’ 2023 U.S. Leveraged Finance (LevFin) default forecasts for high-yield loans rose from 3–3.5% in January 2023 to 4.5–5% in their May 2023 report (Exhibit 5).2 Given the significant growth in the credit markets since the global financial crisis, even a moderate increase in default rates can create an enormous opportunity for distressed investing. Investors may want to prioritize this segment of the market in 2023 to add diversification and enhance the return and income potential of their portfolios.

2. Private equity: Buyout

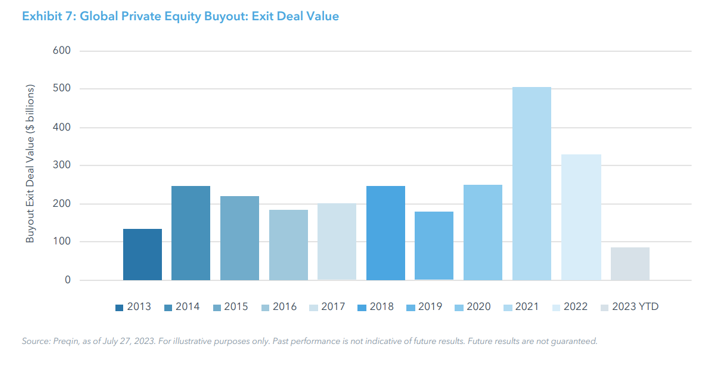

The first half of 2023 has generally seen a continuation of 2022 sentiments with macro uncertainty, limited exits, and subdued fundraising dominating private equity headlines. These prevailing circumstances are causing general partners (GPs) to pivot to quality, creativity, and discipline more heavily, with a tighter focus on selectivity and value creation. In the first quarter of 2023, completed buyout deals were valued at 10–15% lower than the same period in 2022.3 My conviction for the buyout investment theme was partly rooted in the lower valuation which has started to take effect.

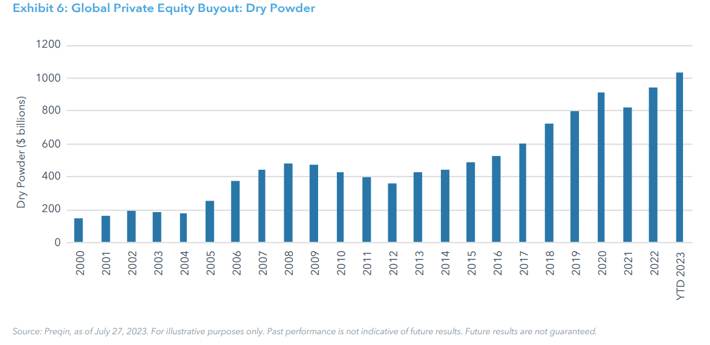

But I am keeping a keen eye on the amount of “dry powder” in the private equity buyout ecosystem, which stands globally at about $1.1 trillion.4 With the rebound of public markets in the first half of the year,5 signs of the relative easing of inflation, and some green shoots showing in the IPO market, there is a concern that deal valuations will rebound back to the levels they were in late 2021/early 2022. Fundraising for new funds has been slow, which is keeping dry powder in check. But as market conditions improve faster than expected, investors’ sentiment towards new deals and new fund commitments will play an important role in valuations for new deals.

3. Real assets: Opportunistic real estate

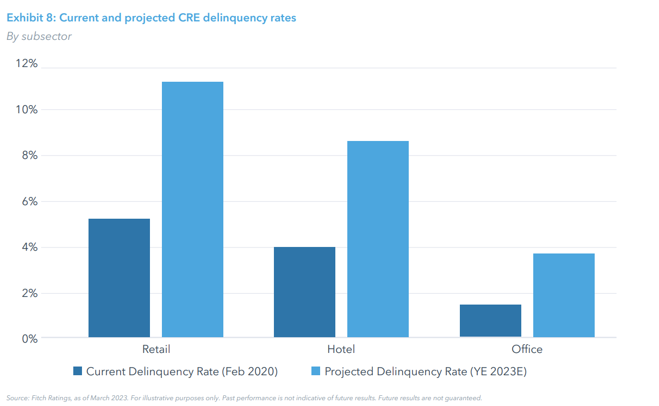

As borrowing costs have risen, cracks have started to appear in the commercial real estate (CRE) market, exacerbated by a $1.5 trillion wall of looming loan maturities by the end of 2025,6 and instability among regional banks. Moreover, an economic slowdown could further dampen demand for real estate, increasing the stress on pricing (Exhibit 8). This has led to a CRE sell-off in recent quarters, particularly in the more duration-risk sensitive core and core-plus segments of the market.

Against this backdrop, a combination of factors make investing in higher-returning opportunistic real estate very compelling: 1) near-term refinancings at higher rates and less clarity on net income is expected to lead to stress and even distress; 2) ongoing secular shifts and trends within multifamily, logistics, and offices resulting in potentially large property type dispersions; and 3) the chance to deploy fresh capital in a new vintage without the drag of existing assets weighing on returns. In my view, experienced opportunistic real estate managers are positioned to capitalize on opportunities that are experiencing financial and/or operational dislocation, and they have the potential to generate returns via improvements and repositioning, rather than raising rents (which is difficult to do in challenging economic environments). Adding an allocation (or increasing an existing allocation) to opportunistic real estate could diversify growth options within a client portfolio.

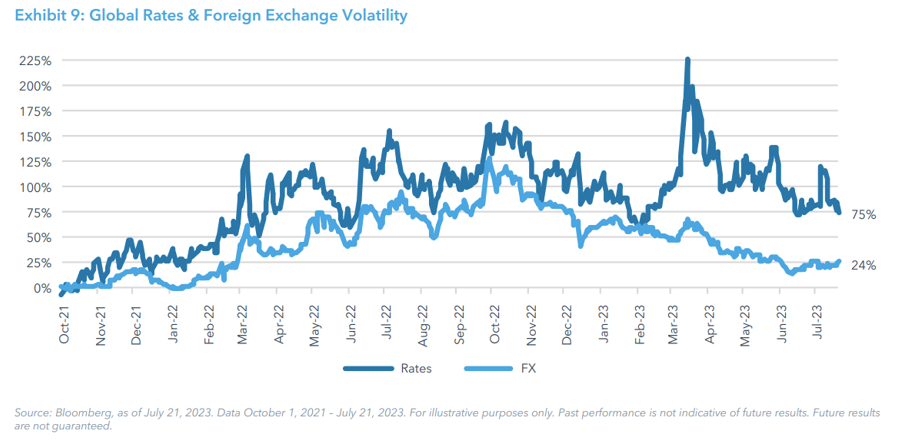

4. Hedge funds: Macro

Macro hedge funds invest globally across fixed income, foreign exchange, commodities, and equity markets based on a top-down assessment of factors, such as economic growth, central bank policies, and geopolitics. These funds have been consistent positive performers in recent years and were the top performing hedge fund category in 2022.7 While most macro managers trade across asset classes, global interest rates, and foreign exchange are often key markets for managers to express their views through both relative value and directional trading. As a result, macro hedge funds are often able to take advantage of periods of heightened volatility within the rates and FX markets, as I have witnessed recently (Exhibit 9). With inflation still stubbornly high in many countries, I expect periodic spikes in volatility moving forward, with divergent interest rate policies impacting the relative value of developed and emerging market currencies.

Looking back over 30 years, macro funds have generally produced returns with limited beta and correlation to traditional stocks and bonds, and have tended to perform well during crisis periods, underscoring their diversification benefits in portfolios of traditional assets.8 Although off to a modest start in 2023,9 I continue to have a favorable view for the strategy in an environment characterized by high interest rates, elevated inflation, and uncertainty around economic growth. Should these trends continue as I expect, it will offer an opportunity for macro practitioners to identify and structure trades with asymmetric risk/return profiles.

5. Structured investments: Notes with downside protection

As short-term rates remain elevated, I continue to see an opportunity for investors in structured investments. The higher rate for the bond component of a structured investment allows for more funding to be deployed in the underlying options package, offering investors the potential to lock in more attractive enhanced upside and/or downside protection terms. For example, I am seeing equity-linked income notes offering 40% barrier protection with double-digit contingent coupons, providing investors with enhanced income potential while also maintaining downside protection in the event of volatility in the equities market10.

Investors can also gain structured investment exposure through defined outcome funds, which can offer strategic exposure to equities for bullish investors with limited loss exposure. Higher rates have allowed investors to benefit from shorter holding periods and higher upside caps, with certain funds providing for 95% principal protection and a 20–23% upside cap after a two-year maturity11.

The potential to take advantage of attractive structured investment terms in the high-rate environment is especially timely as I anticipate nearing the end of the Fed rate hiking cycle. Thus, investors would be well positioned to lock in elevated rates now.

Anastasia Amoroso is a managing director and the chief investment strategist at iCapital.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our full schedule of upcoming CE-approved virtual events.

Read more articles by Anastasia Amoroso

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.