Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Why don’t they do what they say? Say what they mean?

These were the burning questions asked by the British “new wave” band the Fixx on its 1983 hit “One Thing Leads to Another.” The song was allegedly written as an indictment of dishonest politicians. But I’ve grown convinced that they were talking about responders to the University of Michigan Consumer Sentiment survey.

This monthly telephone survey asks roughly 600 adult Americans dozens of questions related to how they feel about the economy. The answers are aggregated into a simple index – the widely-watched University of Michigan Consumer Sentiment Index (MCSI).

If your day includes a steady diet of market and economic news, you’re likely familiar with the MCSI. And if you have market-savvy clients, they’re likely reading (and wondering) about it too. MCSI results are regularly reported and analyzed on social media by popular market commentators like Mohamed El-Erian, Creative Planning’s Charlie Bilello, and Charles Schwab’s Liz Ann Sonders, to name just a few.

The MCSI is considered an important leading economic indicator. After all, roughly two-thirds of the U.S. economy consists of consumer spending. You would think that insight into how consumers are feeling about the economy and their personal finances would be useful information. But that depends…

Do they do what they say?

If so, we should see a strong correlation between the MCSI and personal consumption expenditures (PCE), which measures consumer spending. If folks are feeling financially optimistic, you’d think they’d be more inclined to spend. If they’re pessimistic, they should be less likely to spend.

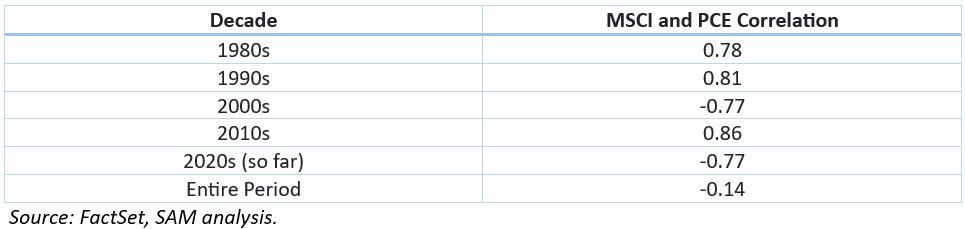

The following chart shows the correlation between the MCSI and PCE over the past several decades. For some context on the strength of a correlation, 0-0.19 is very weak, 0.20-0.39 is weak, 0.40-0.59 is moderate, 0.60-0.79 is strong and 0.80-1 is very strong. It works the same in reverse: A correlation of -0.70 is strongly negative – like the relationship between umbrella sales and sunny days.

There are some very strongly correlated periods, some that are the exact opposite of that, and over the entire period the correlation between investor sentiment and consumer spending is insignificant.

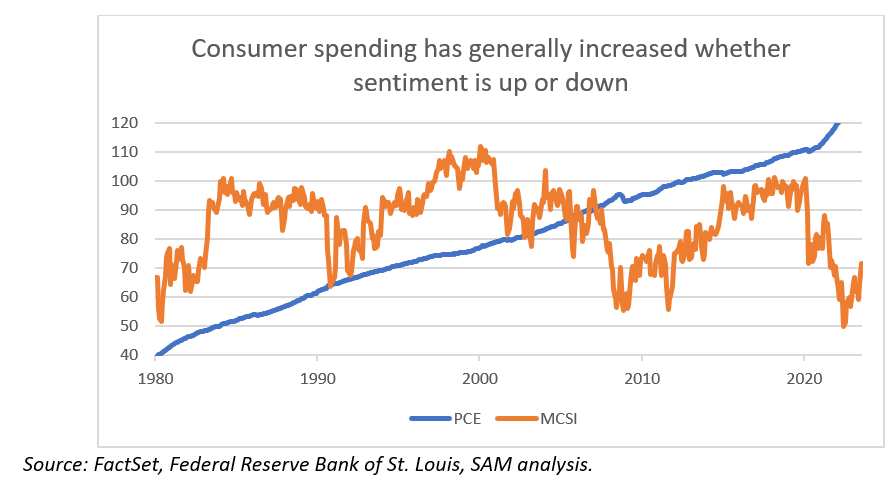

When the folks surveyed by the University of Michigan say they are optimistic, they tend to spend. When they are feeling pessimistic… they still tend to spend.

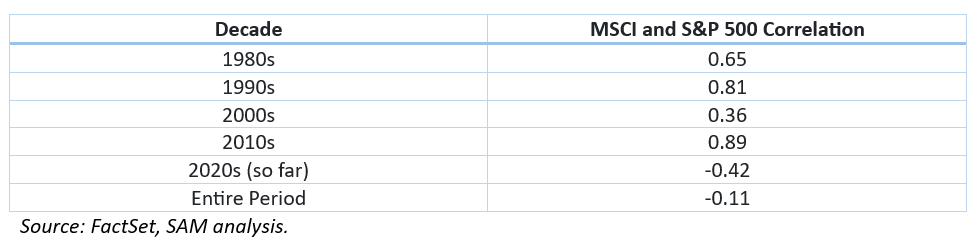

MCSI doesn’t provide an investment edge either. Its correlation to the S&P 500 index is equally spotty.

Clearly, if respondents represent the general public, they do not do what they say.

Why don’t they say what they mean?

Maybe someday the University of Michigan’s calls will be backed by A.I. software that can identify if the voice on the other end of the phone is lying. In the meantime, I’m willing to take them at their word – they probably do say what they mean. At that exact moment.

But sentiment is fickle. These surveys are done by phone. Ever not want to pick up the phone and answer dozens of questions? I’m guessing so. Maybe you got caught in bad traffic on the way home. Or your starting fantasy football quarterback just got carted off the field with an injury. Those annoyances aren’t long-term headwinds for the economy. But they will put you in a dour mood, nonetheless.

Perhaps such annoyances are rare. But it’s certainly reasonable to expect that answers to these surveys reflect what people are reading and hearing. After all, these are not 600 economic prognosticators. It makes sense that they would extrapolate how they feel today into the future.

And that’s what the University of Michigan Consumer Sentiment Index is best used for – knowing how the American public is feeling today.

The market, of course, looks forward. So, when you see articles and posts about the MCSI, ignore them. And if your clients approach you with MCSI questions, ask them about how they are feeling. Then, gently and politely, break it to them: The market doesn’t care.

Michael Joseph, CFA is a portfolio manager and deputy chief investment officer at Stansberry Asset Management. He is a member of the CFA Institute’s Practice Analysis Working Body and sits on the board of Copper State Credit Union and the advisory board of the Arizona Council on Economic Education. He can be contacted at [email protected].

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

Read more articles by Michael Joseph

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.