There’s a new crediting strategy available for registered indexed-linked annuities (RILAs) called “dual directional.” While common in the structured products space for at least a decade, dual-directional approaches allow for the investor to potentially receive a positive credited return even if the return of the underlier (e.g., the price return of the S&P 500) is negative, typically within certain ranges.

There’s a new crediting strategy available for registered indexed-linked annuities (RILAs) called “dual directional.” While common in the structured products space for at least a decade, dual-directional approaches allow for the investor to potentially receive a positive credited return even if the return of the underlier (e.g., the price return of the S&P 500) is negative, typically within certain ranges.

In this piece, I explore the efficacy of traditional RILAs and those that offer dual-directional crediting. I use a total-portfolio context with a portfolio-optimization approach based on utility theory.

I found that both types of RILAs (traditional and dual directional) have the potential to improve portfolio efficiency, although allocations to dual-directional RILAs were greater and they resulted in greater risk-adjusted returns than traditional counterparts, likely due to the diversification benefits of the approach.

Dual-directional crediting strategies are worth considering for client portfolios, especially for those individuals already considering allocating to RILAs.

RILAs with dual-directional crediting

RILAs are also referred to as structured annuities, investment-variable annuities and buffered annuities. While these sound like very different things, the underlying strategy is very similar. An insurance company uses financial options to gain a unique exposure to an index, typically to create a “buffer” or a “floor” approach.

With a buffer, the first amount of loss is absorbed by the product, based on the buffer level, and the investor would suffer any loss beyond that point. For example, if the buffer is 10% and the return of the underlier (such as the S&P 500) was -40%, the investor would lose 30%. With floor products, the downside is limited to a stated percentage, such as 10%. For example, if the floor is 10%, you can’t lose more than 10% regardless of the return of the underlier (e.g., the S&P 500). A RILA with a 0% floor would have the same risk profile as a fixed-indexed annuity (FIA).

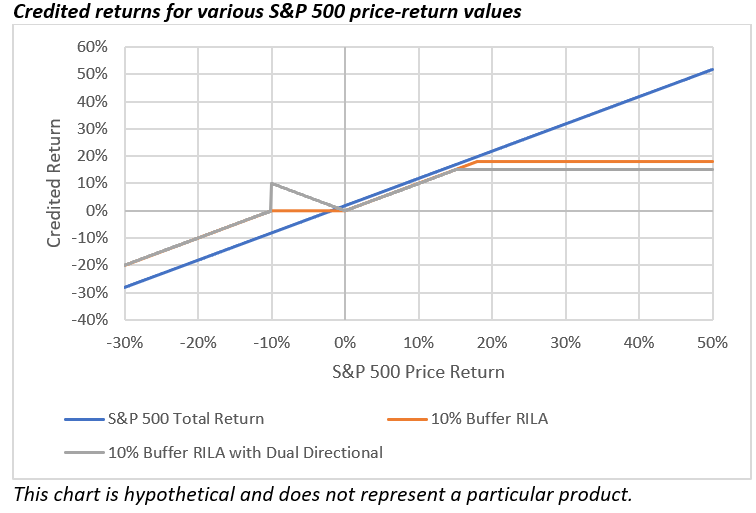

With dual directional approaches, the credited return can be positive if there is a positive or negative return for the underlier. Dual-directional crediting strategies in RILAs tend to result in positive credited return if the underlier falls between zero and the respective buffer, where the credited return is the absolute value of the negative return. For example, if the buffer is 10% and the return of the underlier was -5%, the credited return would be 5%.

Dual-directional strategies reduce the cap (i.e., upside) for a given RILA. For example, focusing on RILAs from two different issuers (but effectively the same product), a RILA with a 10% buffer and a one-year segment duration on the S&P 500 would have cap of 18%. Including the dual-directional approach would reduce the cap to 15%. Alternatively, a RILA with a 20% buffer and a six-year term on the S&P 500 would have an unlimited cap, while the dual-directional cap would be 140%. The exhibit below includes the credit returns for different index (price returns) for the S&P 500 assuming the previously noted one-year structure.

Dual-directional strategies effectively represent a “trade” (the fundamental nature of RILAs) where there is less upside when returns are positive but a positive return when the return of the underlier is negative, but within a given range.

Analysis

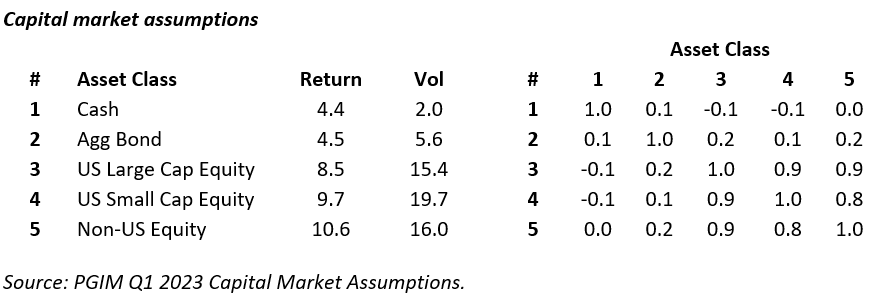

I determined optimal portfolios for this analysis using a constant relative-risk-aversion (CRRA) utility function where the goal is to maximize the certainty-equivalent wealth given the respective risk-aversion levels, assuming a one-year investment period. This utility model captures the unique return distribution associated with RILAs (i.e., it does not have to assume returns are normally distributed). For the analysis, I generated 1,000 years of returns using the capital market assumptions (CMAs) below (which are based on PGIM’s Q1 2023 estimates) assuming returns are multivariate normal.

The dividend yield on U.S. large-cap equity is assumed to be 1.7%, which reduces the credited return of the RILA, since it is based on price return. I imposed a maximum 50% allocation constraint to non-U.S. equity to ensure reasonably diversified (i.e., implementable) portfolios.

While there are no assumed explicit expenses with the RILA, since most RILAs do not have explicit fees, there are generally explicit fees when financial advisors manage a portfolio for a client. Therefore, a 1.1% fee is assessed against the portfolio, which reflects a 100 basis point advisor fee and a 10 basis point investment management fee.

While this analysis focuses on RILAs, it would be possible for advisors to build the specific strategies modeled directly using financial options. This analysis also ignores taxes (i.e., assumes monies are in a tax-deferred account, such as an IRA).

I considered two RILAs, and both have 10% buffers where the underlier is the S&P 500. The cap for the traditional 10% buffer RILA is assumed to be 18%, and the cap for the 10% buffer RILA with dual-directional crediting is 15%. These caps are consistent both with an actual RILA product that exists on the market as well as a model used to estimate caps based on the Black–Scholes options pricing model.

The equity allocations range from 100% for a risk-aversion level of approximately 1 and an equity allocation of approximately 10% for a risk-aversion level of approximately 30. When solving for the optimal portfolios that include RILAs, the assumed risk-aversion levels are determined based on a power trendline that fits the optimal equity levels. This creates a more accessible risk target for displaying results. The analysis includes results based on the risk aversion coefficients for equity allocation targets of 10% to 100% in 5% increments.

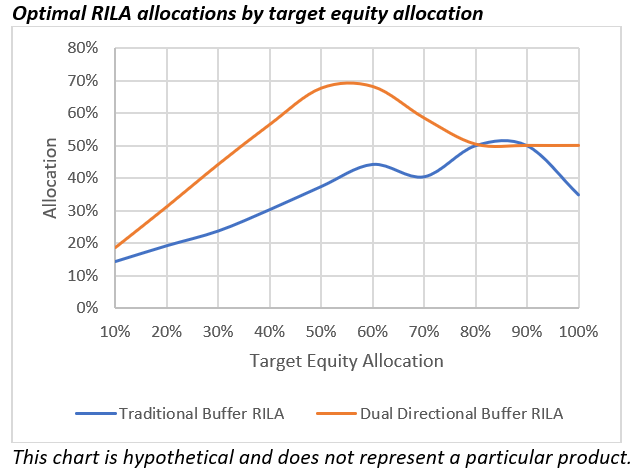

The exhibit below includes the optimal allocations to the two types of RILAs for the equity allocation range considered.

The allocations to either RILA are both positive (i.e., they improve portfolio efficiency), although they are clearly highest for investors with a balanced risk aversion.

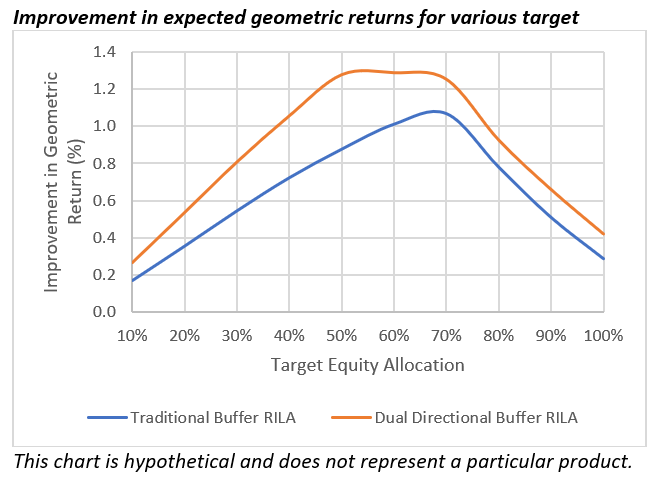

The allocations to the dual-directional RILA are notably higher than the traditional RILA as well, suggesting they result in greater gains in portfolio efficiency. The next exhibit provides some context on this effect and includes the difference in the geometric expected return of the respective portfolios that include the weights to the RILAs versus those that exclude RILAs (i.e., include only the base asset classes).

The expected geometric returns are positive for sets of RILAs, suggesting they can result in more efficient portfolios. The expected geometric returns are notably higher for the dual-directional RILA strategy, though, suggesting they can improve portfolio outcomes more than traditional RILAs alone.

RILAs are an annuity structure that is capturing increasing assets and attention among financial advisors for these reasons.

Conclusions

Within the RILA space, there is a new crediting strategy emerging referred to as “dual directional” where credited returns can be positive even if the return of the underlier (e.g., the S&P 500) is negative. This analysis suggests that allocating to dual-directional strategies can improve portfolio efficiency beyond the benefits from allocating to traditional RILAs.

David Blanchett, PhD, CFA, CFP®, is managing director and head of retirement research at PGIM. PGIM is the global investment management business of Prudential Financial, Inc. He is also an adjunct professor of wealth management at The American College of Financial Services and a research fellow for the Retirement Income Institute.

Disclosures

Hypothetical Past performance is not indicative of future results.

Clients should consider the contract and the underlying portfolios’ investment objectives, policies, management, risks, charges and expenses carefully before investing. This and other important information is contained in the prospectus, which clients should obtain from their financial professional and read carefully.

It is possible to lose money by investing in securities.

This material is being provided for informational or educational purposes only and is not a recommendation about managing or investing a client’s retirement savings.

Provided courtesy of Pruco Life Insurance Company, Newark NJ, and Prudential Annuities Distributors, Inc., Shelton, CT, subsidiaries of Prudential Financial, Inc.

Exclusively for Financial Professionals. Not for use with Consumers.

1072731-00001-00

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

Read more articles by David Blanchett

There’s a new crediting strategy available for registered indexed-linked annuities (RILAs) called “dual directional.” While common in the structured products space for at least a decade, dual-directional approaches allow for the investor to potentially receive a positive credited return even if the return of the underlier (e.g., the price return of the S&P 500) is negative, typically within certain ranges.

There’s a new crediting strategy available for registered indexed-linked annuities (RILAs) called “dual directional.” While common in the structured products space for at least a decade, dual-directional approaches allow for the investor to potentially receive a positive credited return even if the return of the underlier (e.g., the price return of the S&P 500) is negative, typically within certain ranges.