Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Caribou is hosting the 2023 Open Enrollment Summit. You can register for free here.

Medicare open enrollment comes every year and impacts over 55 million Americans. It’s an important time for Medicare beneficiaries to optimize their healthcare coverage and costs, and financial advisors are in the perfect position to guide clients through this crucial planning opportunity. Unfortunately, thanks to the complexity of healthcare, there are several mistakes I see advisors make year after year when it comes to Medicare open enrollment. In this article, I’ll break down the five most common mistakes I see and how to avoid them.

1. Starting too late

Every year I see advisors and their clients wait until the last two weeks of open enrollment to select coverage. This leaves little time to fully consider options and thoroughly assist clients. To avoid this mistake, meet with your clients before open enrollment even starts. September is a great time to schedule a meeting or call with clients to discuss their coverage preferences, and current and anticipated healthcare needs for next year.

Another way you can avoid the mistake of waiting too late is to remind clients about open enrollment. Something as simple as an email on October 15th announcing, “Medicare Open Enrollment is here! Need help determining your optimal coverage? Let’s set up a call,” will ensure that clients stay on top of their to-dos for open enrollment. This also gives them plenty of time to identify and enroll in the optimal Medicare coverage.

Include reminders in your CRM; one reminder the week before open enrollment starts and one three weeks before the end of open enrollment.

2. Assuming a client’s coverage from last year is the best choice this year

Amitabh Chandra, a healthcare economist, had an excellent article detailing the psychology of choosing and “availability heuristics,” and why people select the wrong health plan for their needs – a mistake that costs some clients 40% more than they would have otherwise paid in premiums.

For Medicare Advantage plans especially, costs, provider contracts, and drugs covered change every year. But for both original Medicare and Medicare Advantage, drug costs are a major expense. A prescription covered by your client’s plan last year might not be covered again this year because of a change in the plan’s drug formulary. And because there is currently no cap on how much Medicare beneficiaries can spend on drug costs, it’s imperative to review clients’ list of prescription medications each year during open enrollment to confirm as many of their medications as possible are covered at the best price.

To ensure your client doesn’t spend thousands in out-of-pocket drug costs, sit down with them and ask them to list their prescription medications. Check the insurance plan carrier’s website for covered medications. For example, Humana has a web page where visitors can check to see if a certain medication is covered. Doing a simple check with your clients will determine if their current plan is worth reconsidering for this year’s enrollment season.

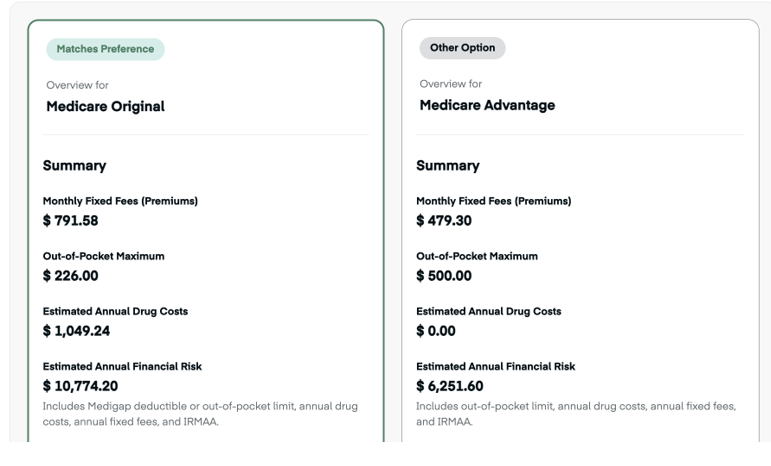

3. Only looking at monthly costs

Monthly costs are important, but they aren’t the only cost to consider. As a comprehensive financial advisor, it’s up to you to help clients review all the costs associated with Medicare. Take drug costs, for example. Let’s say your client wants to keep their healthcare costs low, so they choose a plan with a low monthly premium. But it turns out that the plan doesn’t provide comprehensive drug coverage for their prescription list, so they end up paying more on an annual basis. Look at network coverage. If your client picks a plan with a low monthly premium, but their primary care physician isn’t in-network, they’re going to end up spending more out-of-pocket every time they visit their doctor.

To avoid this mistake, look at all the costs associated with a particular coverage option. If your client is going with original Medicare, they’ll have:

- Part A premium (usually $0);

- Part B premium (income-based premium, potential IRMAA, and an annual deductible);

- Part D (income-based premium and a potential deductible); and

- Medigap (monthly premium, deductible, and an out-of-pocket maximum).

For Medicare Advantage plans, the costs vary greatly depending on the carrier, whether it’s a high- or low-deductible plan, and other factors. Your client will pay the monthly Part B premium and may also pay the plan’s premium (if there is one). Most plans include Medicare drug coverage (Part D). Help them compare plans by looking at the following costs:

- Part B premium (income-based premium, potential IRMAA, and an annual deductible);

- Medicare Advantage plan premium, if applicable;

- Medicare Advantage plan deductible;

- Medicare Advantage plan out-of-pocket maximum; and

- Part D (income-based premium and a potential deductible).

4. Using outdated healthcare cost estimates

Estimates are a great way to view expected healthcare costs, but they shouldn’t be the only number advisors and their clients use. Open Enrollment is the best time to refresh your healthcare line item in clients’ financial plans. Clients' costs will change year over year, especially as they age, and only adding inflation into estimates isn’t enough. For example, average estimates don’t take the following into account:

- Specific healthcare needs, such as medications or preferred doctors, which accrue with age;

- Location (healthcare costs vary based on where you live, and clients often move in retirement); and

- Personal preferences, like carriers and risk tolerance, which change as clients get into their decumulation phase.

To avoid this mistake, look at how frequently clients used the healthcare system last year and how much they spent on out-of-pocket costs and monthly premiums. Look at the plans available for the upcoming year that cover those needs. Then, update their financial plan. Include out-of-pocket costs, which include any co-pays they had when visiting a provider or facility, and how much they spent on medications, medical equipment, and procedures and treatments. Also, factor in clients’ most recent year of healthcare spending as it will give you a more accurate snapshot of what their expected healthcare costs will be next year. And to get even more accurate and customized healthcare cost calculations for clients, partner with a company that offers healthcare planning software to take the “heavy lifting” off your to-do list.

5. Not helping clients with open enrollment at all

The final – and biggest – mistake I see advisors make is not assisting their clients at all! Healthcare costs account for 15% of one’s assets during retirement – an average of $315,000. Put another way, healthcare costs are the third-highest area of spending in retirement. For advisors who want to provide truly comprehensive financial planning, it doesn’t make sense to ignore healthcare costs in their clients’ financial plans – especially for Medicare beneficiaries.

How can advisors avoid this mistake? Take all the tips in this article and apply them. If you’ve never helped clients through the open enrollment process, pick a handful of clients between the ages of 65-68. These are the clients who will either be going through open enrollment for the first time or have only done it a few times so far, and will likely need the most help navigating the process. For a full list of questions and considerations to walk clients through, click here.

Final thoughts

Healthcare costs will either help or hurt your client’s financial goals, and Medicare costs are no exception. Even beyond costs, helping clients pick the optimal health plan for their needs will save them a lot of unnecessary stress and build deeper client-advisor trust. Now that you know the mistakes to avoid and are equipped with strategies and actionable tips, you can confidently guide your clients through this open enrollment season.

Christine Simone is a co-founder of Caribou, a company that offers software to financial advisors to plan for and optimize healthcare costs. She often writes on the topics of healthcare and women in tech.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.