Calling your business a burning platform is, in most cases, a stupid thing to do. The idea is to scare staff into performing better and prepare an underperforming organization for painful layoffs. But it can just make things worse. The collateral damage may include frightening away customers who fear the firm could go bust. The boss of Rolls-Royce Holdings Plc has just shown that the gamble can — sometimes — pay off.

Tufan Erginbilgic used the phrase in a town hall with staff shortly after taking the helm of the UK aerospace and defense icon in January. The message was blunt: Rolls is bloated, it fails to make a satisfactory return on capital and its crisis is existential. In an industry relying on long-term contracts, this was an especially risky approach. Inevitably, it leaked. The immediate share price reaction was negative. Erginbilgic previously ran a division of oil major BP Plc and appeared to be showing his inexperience as the chief executive officer of a listed company.

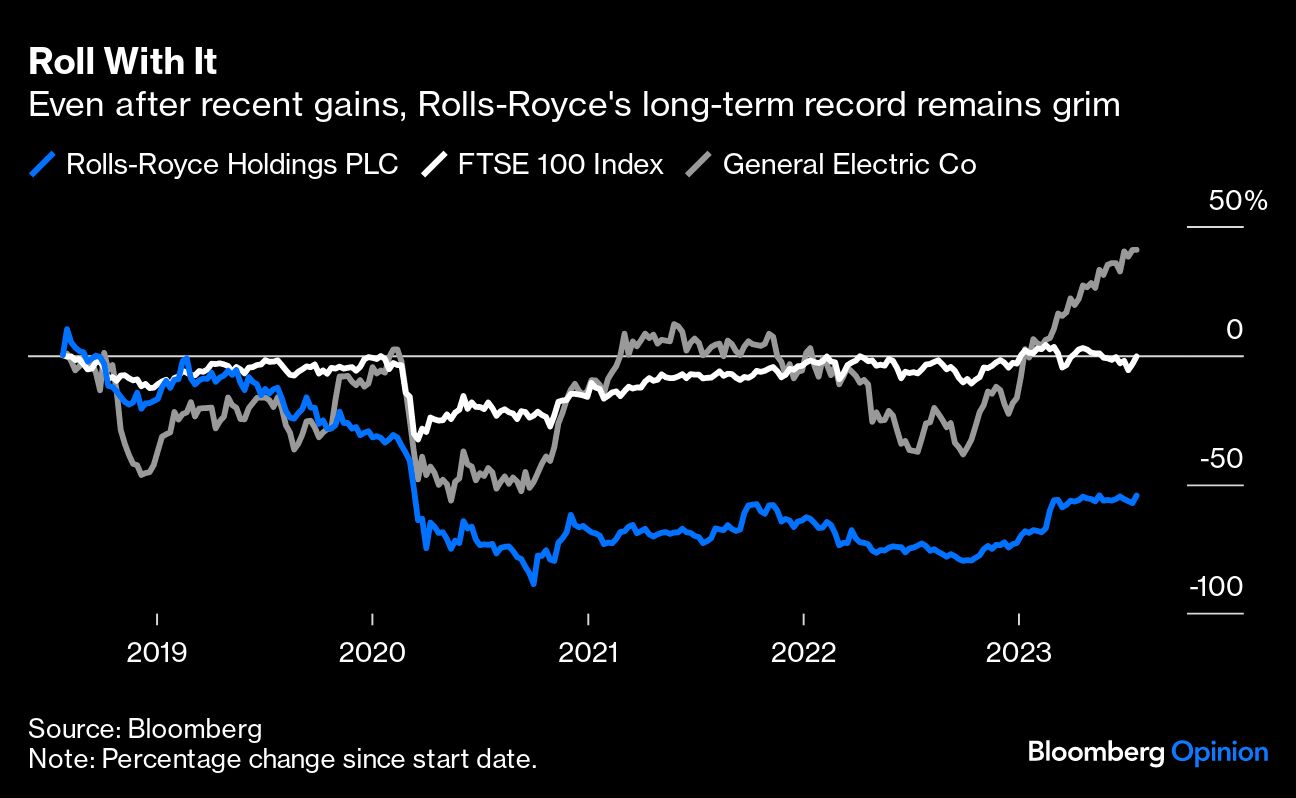

Yet on Wednesday, Rolls’ shares jumped as much as 25% after the company said operating profit excluding one-off items would be around £670 million ($865 million) at the half-year stage, more than double the consensus forecast, with the full-year number likely to be at least £1.2 billion, around one-third higher than analysts expected. This year, the stock has almost doubled, valuing the company at more than £15 billion.

Rolls cites a combination of “commercial optimization,” pricing actions, and contract improvements as partly responsible for its change of fortune. The implication is that Erginbilgic has made customers agree to terms more favorable to Rolls, renegotiating existing agreements and reducing the drag of uneconomic legacy contracts written in a rush to win market share.

Of course, it helps that the airline industry has bounced back faster than expected following the pandemic. Defense spending is up, and Rolls has also found ways to service engines at lower costs. All the same, there’s at least some evidence here that CEOs can sometimes scare customers into helping keep a supplier alive.

There are still big questions for Roll's investors. In the short term, one is how much extra there is to pursue in becoming more efficient and aggressive — was this just low-hanging fruit? Further out is the issue of Rolls’ strategy in engines for narrow-body planes. Having exited a joint venture with Pratt & Whitney a decade ago, Rolls needs to find another partner or generate sufficient cash to make the hefty organic investment required to serve the next-generation fleet. It had bet on wide-body planes — a lower volume but higher margin business.