Are Clients Saving Too Much for Retirement?

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Conventional wisdom is that retirees spend a fixed amount per year in real terms, meaning that the nominal amount they need rises each year with inflation. But evidence on actual spending behavior suggests that real spending falls with age. If that’s true, people need to save less for retirement than we think.

The standard model of retirement planning may have a key flaw

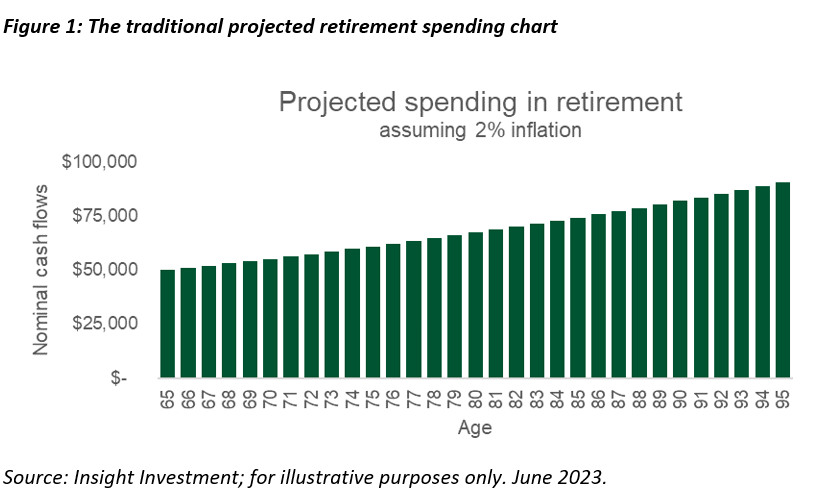

Financial advisors and their clients are familiar with the traditional upward-sloping chart of nominal spending in retirement:

This chart (figure 1) assumes that retirees’ spending stays constant in real terms and, therefore, nominal spending rises each year in line with inflation. In this example, a prospective retiree expects to spend $50,000 annually in retirement, and her advisor applies a 2% inflation adjustment to estimate future nominal spending.

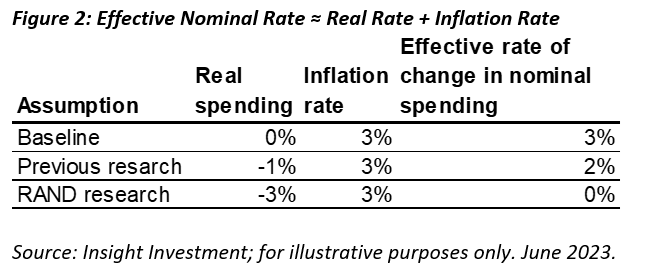

But this traditional model may be fundamentally flawed. Most previous research suggests that real spending is not flat over time but rather declines with age, at ~1% per year on average.

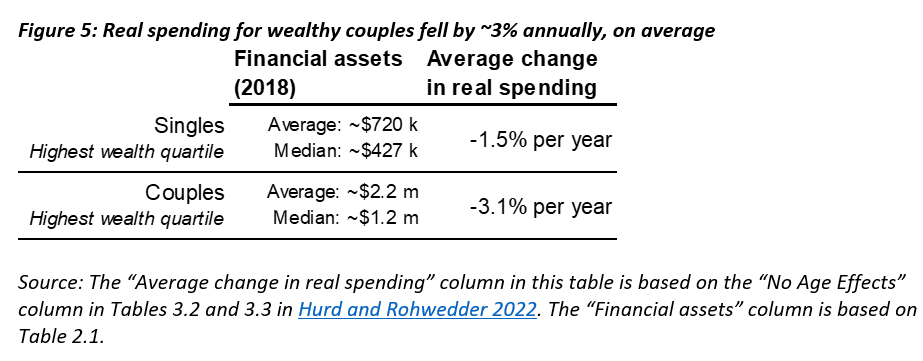

New research from the RAND Corporation (sponsored by Insight Investment) found that real spending for wealthy couples declined even faster, at ~3% per year on average. This finding has important implications for retirement planners.

Why are spending assumptions so important for retirement planning?

Real-spending assumptions determine the amount required to save, and even small changes in these assumptions result in big differences in that amount.

To demonstrate how significant the differences are, we compared three real spending assumptions:

1. A baseline assumption of 0%, based on current advisor practice;

2. An assumption of 1% annual decline, based on most previous research on this topic; and

3. A 3% annual decline, based on the new RAND research.

To keep the math simple, in all three cases we assumed inflation was 3%.

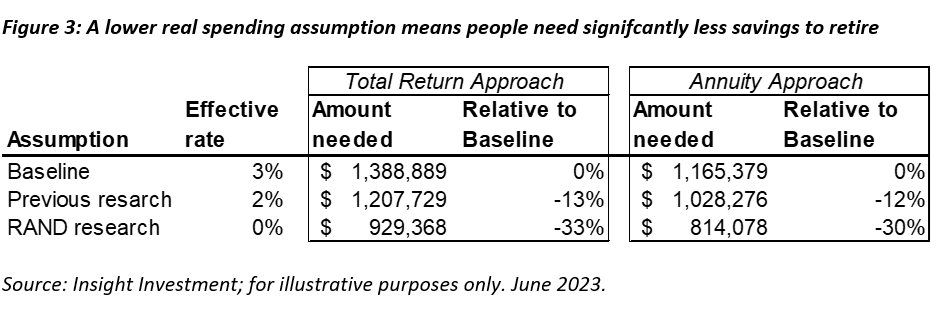

To evaluate the planning implications of these different effective rates, we considered two approaches to generating retirement income: a probability-based “safe withdrawal” approach and a safety-first solution using a single premium immediate annuity (SPIA). We assumed that a 65-year-old couple analyzed how much they would need to retire with an annual income of $50,000 from their assets.

Under both approaches (assumptions in the appendix), a small change in the effective spending rates made a big difference in the amount of savings required to retire. Compared to the baseline assumption, using estimates from the new RAND research means the couple would need 33% less to retire under the total-return approach and 30% less under the annuity approach.

How RAND arrived at a 3% annual real spending decline for wealthy couples

The recent RAND study looked at spending patterns using the Health and Retirement Survey (HRS), a longitudinal survey of older Americans from 2005-2019 conducted by the University of Michigan. The researchers sampled over 4,000 households aged 65 and older.

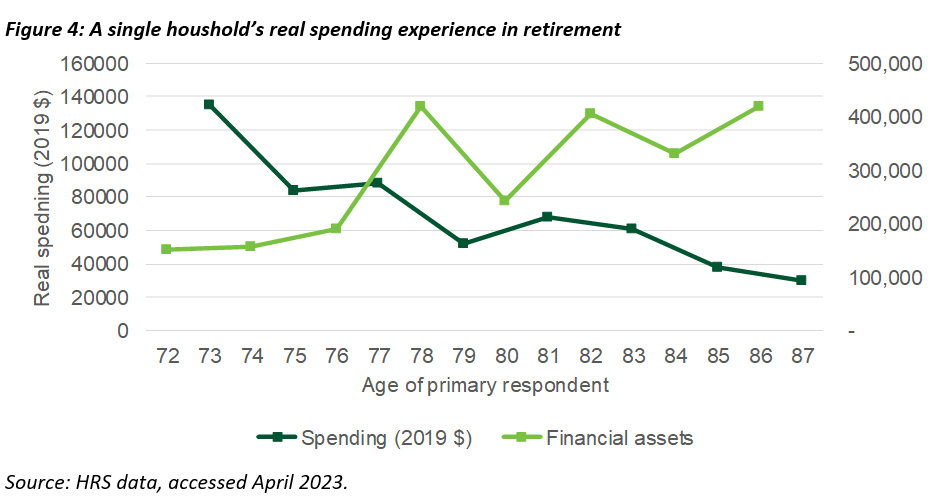

For example, one surveyed household was a married couple – in 2005, the husband was 73 and still working, and the wife was 70 and retired. By 2007, the husband was also retired, and both appeared 14 years later in the 2019 survey. Figure 4 shows their spending and assets over time.

Their real spending dropped sharply after retirement, as it does for some people, and then fell on average ~8% every two years, or ~4% annually in the subsequent 12 years. Meanwhile, the household’s asset levels generally went up over time.

The RAND study aggregated data across individual cases like this and used regression analysis to estimate how spending tends to change with age across thousands of households. It also broke the data into couples versus singles as well as by how wealthy the household was around age 65. The researchers only included couples that stayed intact from one survey to the next to screen out the effects on spending from widowing or divorce.

The study found that single households reduced spending by -1.5% per year on average, while couples reduced spending at -3.1% (Figure 5).

Some evidence indicates retirees chose to reduce spending over time

A key outstanding question is whether retirees want to spend less, or if it is something they do because they feel financially constrained.

At 93, perhaps retirees have seen enough of the world and been to enough fancy restaurants; or perhaps their more limited mobility makes it harder to enjoy those things. Alternatively, retirees may cut spending because they become increasingly concerned about running out of money, especially if they have spent too much earlier in retirement.

Depending on the answer, financial advisors should either plan for these spending declines we saw in the data, or help clients avoid them.

Unfortunately, there is no perfect answer at this stage. But there is some evidence that the decline in spending is, in fact, voluntary. The RAND study noted two key pieces of evidence:

1. Affluent people lowered their spending about as much as less-affluent people.

2. Budget shares for gifts and donations rise, especially for wealthier people, perhaps indicating they did not feel financially constrained.

A separate RAND study reported that “the majority of individuals at advanced ages reported less enjoyment from spending on travel; dining out; leisure activities; and new appliances, clothes, or a car… at the same time, indicators of financial or of being financially constrained were much less frequently reported at advanced ages.”

If a decline in spending is, in fact voluntary, this would validate Michael Stein’s idea from 1998 that there are three phases to retirement: the go-go years, the slow-go years, and the no-go years.

Healthcare cost risks should be dealt with separately

Another big question is about out-of-pocket (OOP) healthcare costs at the end of life. Did the “no-go” years come with increased spending on nursing homes and long-term care (not covered by Medicare)? Was the increase enough to offset declines in other kinds of spending, like leisure, travel, and housing?

The RAND study referenced another paper that found these expenses were concentrated among a small proportion of households. It showed the median OOP spending in the last year of life was $6,300; just 5% of households spent more than $62,000. As the authors noted, “at least at the median, accounting for OOP would not materially affect our findings about declining spending with age.”

As many advisors know, because end-of-life OOP costs can be very high but are not incurred by most people, it makes more sense to insure against this risk by using long-term care insurance rather than by incorporating it into a long-term spending plan.

To see why, for simplicity assume that 5% of wealthy people spend $200,000 on OOP expenses in the final years of their life, while the other 95% spend just $10,000. Of course, no one knows if they will be in the 5% or the 95%. In expected value terms, OOP costs will be ~$20,000 on average (5% x $200,000 + 95% x $10,000). If that $20,000 is incorporated into a plan, it will not do the retiree much good. If they are in the 5%, they will still have a huge shortfall if they need to pay $200,000 for OOP costs. If they are in the 95%, they will have twice as much as they need, which means they will have given up on higher spending earlier when they were healthier. When there is a small chance of a large expenditure, insurance is likely a more sensible solution than planning for the average.

Every client is different

The RAND research, like most other research on this topic, tells us about averages. But advisors know that clients are all different. Some will end up spending more over time in real terms. Other clients will have spending that bounces up and down over time, without a clear direction.

Understanding this variability in spending requires further research, as the authors of the RAND study noted. But averages are still useful for determining a starting point for planning. The question remains whether using a 0% real spending assumption still makes sense, given the evidence.

What do you think?

What has been your experience with retirees in your practice? Do you think real spending tends to decline during retirement, or does it stay flat or even increase? Or is it all over the map?

How has your experience shaped your planning methods? What do you use as the default real spending trajectory in your planning tool? Do you use a flat rate (0% + inflation), or do you tend to use a different rate?

We would love to hear more about your experience in the comments.

Appendix

Total return assumptions:

- CMAs are based on median CMAs from the Horizon Actuarial 2022 Survey of Capital Market Assumptions

- 60/40 portfolio of stocks (US Large Cap) and bonds (US Corporate Bonds Core)

- 80% probability of success to age 95

- Lognormal distribution of returns

- 1,000 simulations

Single-premium annuity (SPIA) assumptions:

- Data retrieved from Cannex on 2/17/2023.

- SPIA quotes from 12 providers

- Joint-life, non-reducing contract for 65-year-old male and 65-year-old female

- Only providers with A.M. Best rating of A- or better

- Only providers with COLAs at 0%, 2%, and 3% included

Massimo Young, CFA is head of investment solutions and technology for the individual retirement solutions group at Insight Investment.

Sounak Chatterjee, CFA is head of product and client solutions for the individual retirement solutions group at Insight Investment.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All