Ten Crucial Insights from the Year's Index Returns

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits How have U.S. stocks performed this year? The answer is simple, but you’d never know that from looking at the three most often quoted indexes.

How have U.S. stocks performed this year? The answer is simple, but you’d never know that from looking at the three most often quoted indexes.

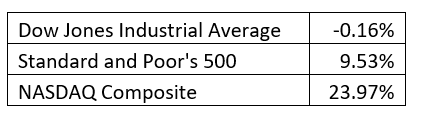

As of May 29, 2023, three major index returns were as follows:

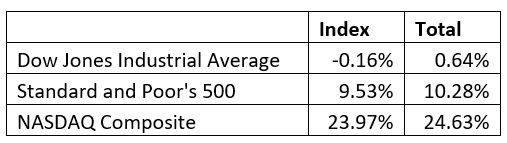

To make matters more confusing, these index returns don’t include dividends, which one must include when looking at total returns. Here are the dividend-adjusted returns:

The differences between the raw and total index returns are small in short periods of time, but they compound over longer horizons. S&P Global reported that since 1926, 32% of the S&P 500 returns have come from dividends.

Your client reading and listening to the mainstream media may understandably be coming to you quite confused about how markets are performing this year.

Which of these three indexes is right? The answer, of course, is none of them. They are all subsets of the total U.S. stock market. The total return (including dividends) of the U.S. stock market was 9.44%.

The total market is the most meaningful because it reflected the total return of the average dollar invested in the U.S. stock market before fees.

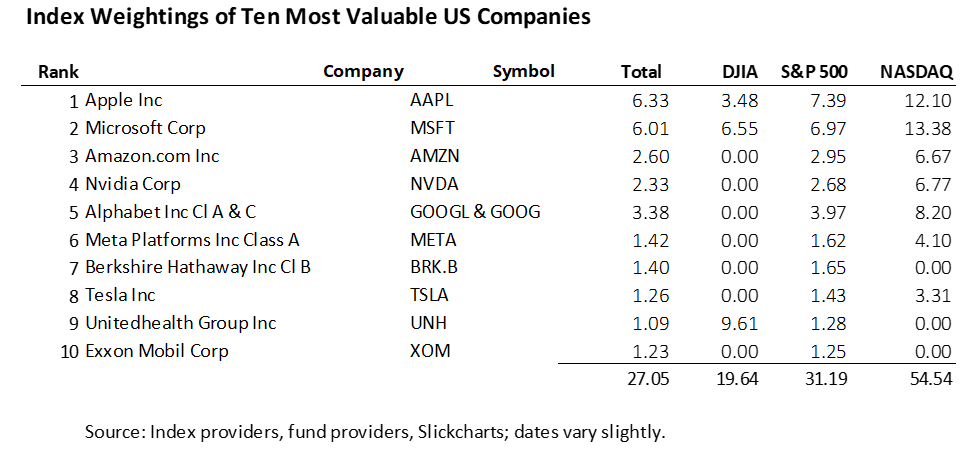

The differences in returns are because the constituents and their weightings vary significantly. In the following chart, you can see that 10 companies (combining Alphabet A and C share classes) comprise a startling 27.05% of the total U.S. stock market. Those 10 companies are also in the S&P 500, but not all are in the DJIA or NASDAQ. So, these 10 most-valuable companies comprise only 19.64% of the DJIA but a whopping 54.54% of the NASDAQ 500.

Apple (AAPL) is in all four indexes, but its weightings vary from 3.48% in the DJIA to 12.10% in the NASDAQ. And while United Healthcare (UNH) was one of the 10 most valuable companies, it accounted for 9.61% of the DJIA average but only 1.09% of the total-stock market. United was down 8.87% for the year.

Though the DJIA is the most-quoted index, it’s a silly little index of only 30 companies and, for obscure historical reasons, is weighted by price rather than market capitalization. Apple is roughly six times as valuable as United Healthcare, but United has a price per share nearly three times that of Apple so it’s weighted nearly three times greater that of Apple. To further illustrate the silliness of the DJIA, if United Healthcare had a 1-10 reverse stock split, it would account for 51.5% of the index without increasing the value of the company. Back when it was created, adding 30 prices per share wasn’t that easy of a task; the fact that it’s still the most quoted index proves the power of inertia.

Explanations

Mega-cap tech companies have driven market returns this year, with 20 companies accounting for almost the entire return of the market. That explains the tech heavy NASDAQ’s stellar return and even why the S&P 500 bested the total-stock market.

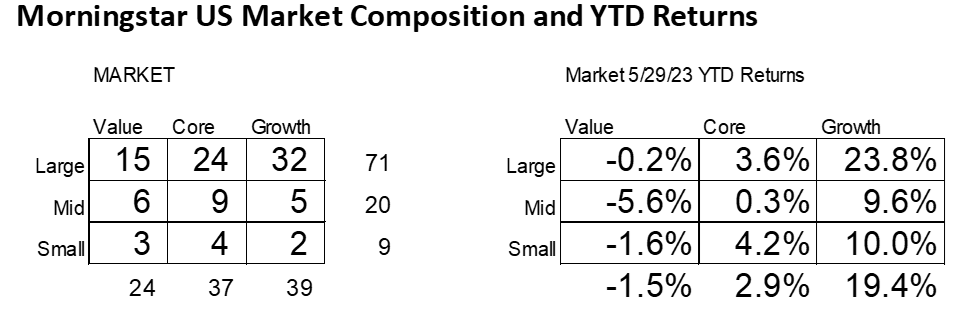

Morningstar assigns the weightings of the styles of the U.S. market as follows:

Morningstar’s definitions reflect its assignment of stocks into one of the nine style boxes. It now defines nearly a third of the total stock market as large-cap growth, which had far greater returns than any other style box. This has been a trend for the last decade, though 2022 was an exception. In fact, roughly 77% of large-cap funds underperformed the S&P 500 index during the first five months, with the average fund underperforming by 2.60 percentage points.

Active managers respond by saying the handful of mega-cap growth funds are distorting market returns. That is an excuse, just like those who confidently said the mega-cap growth stocks were obviously overvalued and small and mid-cap stocks were the hidden gems.

Many claim that this year is an extreme exception when just a few stocks drove market returns. But it turns out that the best performing 4% of listed companies explained virtually the entire net gain for the U.S. stock market since 1926. The other 96% earned an average of zero over nearly a century (according to research by Hendrik Bessembinder, professor, and Francis J. and Mary B. Labriola at Arizona State University).

The high-performing companies are constantly changing along with the hot industries. The six most valuable U.S. stocks today didn’t even exist 50 years ago.

Ten insights and implications

Here are 10 takeaways for you and your clients:

1. The three most-often quoted indexes range from very misleading (DJIA) to a minimally acceptable measure (S&P 500) of the U.S. stock market.

2. The best indicators of U.S. stock performance are lesser known and quoted indexes like the Dow Jones US Total Stock Market Index or the FT Wilshire 5000.

3. Because finding the total return of the above two indexes is difficult, one can look at total returns of broad U.S. stock-index funds such as the iShares Core S&P Total US Stock Market ETF (ITOT) or the Vanguard Total Stock Market ETF (VTI).

4. Irrespective of the index used, one must benchmark a portfolio to the total-return (including dividends) of an index.

5. It is likely that a handful of companies will continue to drive the return of stocks as they have done so for nearly a century.

6. Academic research is backward looking and includes periods of time when today’s most valuable companies didn’t exist, and railroads dominated the stock market. In addition, the cost of buying smaller stocks was prohibitive during most of the past century.

7. Those companies that appear “obviously overvalued” may, in fact, be a bargain. A warning sign that your estimate of the fair value of the market is incorrect is that you feel confident that a part of the market will either outperform or lag.

8. The cap-weighted total-stock market represents the collective wisdom of all investors. It is the only index that is not vulnerable to price distortions from asset flows; assets can flow into or out of this index without fear that the index will be over- or under-valued.

9. Allocate assets in proportion to the total market. For example, a portfolio comprised of 30% small-cap value is over-weighting that part of the market by a factor of 10. That is the opposite of diversification.

10. The only sure way of owning your fair share of next year’s handful of the market’s top performers is to own a total-stock-market index fund.

When I hear the pundits saying the stock market is flat this year, I smile knowing what they mean is that they picked the wrong stocks. Giving clients market returns is far better than giving them excuses. And the next time I drive home and the radio host quotes the DJIA return for the day, I’ll still be wondering how U.S. stocks actually performed.

Allan Roth is the founder of Wealth Logic, LLC, a Colorado-based fee-only registered investment advisory firm. He has been working in the investment world of corporate finance for over 25 years. Allan has served as corporate finance officer of two multi-billion-dollar companies and has consulted with many others while at McKinsey & Company.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All