How Stress Testing Retirement Plans Builds Client Confidence

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Stress tests are everywhere – banks, portfolios, and even retirement plans can get a stress test. But retirement stress tests tell just one story: whether a good retirement will look bleak if portfolio balances take a big hit.

This story can be misleading and drive client anxiety, uncertainty, and inaction.

A better retirement stress test would focus on the standard of living in retirement and how spending would need to change in times of market turmoil or heightened inflation. I led the development of a retirement stress-testing tool that does exactly that. Focusing on income and adjustments, instead of on success and failure, builds confidence and encourages action. When back tested through the rigors of the global financial crisis, 1970s stagflation, or the Great Depression, a good retirement income plan can typically be saved by relatively minor, temporary adjustments.

Most retirement-income planning focuses on the “probability of success” score. So, it’s natural to ask how this score would change if, say, the client’s portfolio experienced a 2008-2009-sized loss. This stress test is indeed available in many software programs, and it’s common to see a plan have gone from an 80% to 50% probability of success during the global financial crisis. But this change in score isn’t very useful. A score doesn’t tell someone what to do. It doesn’t give guidance or directions. If an advisor can’t tell clients what adjustments – if any – would have to be made when experiencing stress, clients will have irrational instincts. Might they run out of money or need to cut spending in half? Or maybe they would have to downsize their house or move in with adult children?

Not only is this success/failure framing scary – it’s wrong.

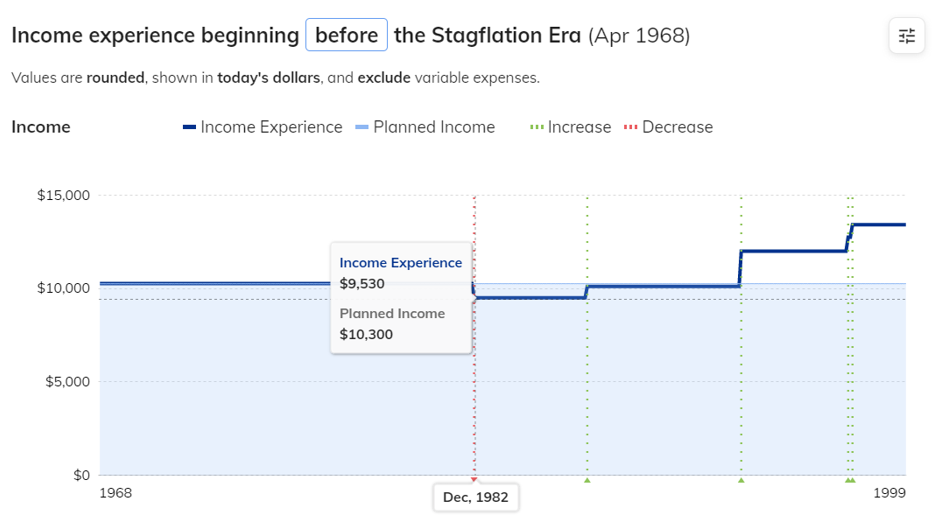

Retirees don’t tend to “fail” in retirement – they adjust. Consider a plan for a 65-year-old couple that provides $10,300/month in inflation-adjusted income through a combination of withdrawals from a $2 million portfolio, two Social Security checks delayed until normal retirement age ($5000/month), and a $1000/month pension. This plan would today have an 80% probability of success, when measured using historical patterns of returns and inflation.

This plan also includes risk-based guardrails that, when tested under the conditions of the global financial crisis, triggered a $200/month reduction in withdrawals and spending from March 2009 to December 2016. After this period of minor belt tightening, the plan allowed for spending above the original plan.

The adjustments in these stress tests are all triggered by risk-based guardrails that take into account the clients’ unique situation and all information available up to each point in the plan and each point in history (ages, mortality expectations, inflation, portfolio performance, timing of non-portfolio cash flows, etc.).

The stagflation of the 1970s and 1980s is a harder test for retirement than the global financial crisis. The anemic real returns and high inflation of those decades that gave us the (in)famous “4% rule.” When stress tested starting in 1968, the above plan required a more sizeable 7.5% reduction in spending and withdrawals from December 1982 to March 1987, with higher-than-originally-planned total spending thereafter.

These stress tests don’t stop at the point of crisis. They run through the length of the plan or up to the present. In contrast, score-based retirement stress testing ignores the fact that we know what happened after the global financial crisis (or any other historical period before it). If we are sitting in 2023, it is irresponsible to stop the stress test in 2009. By withholding half of the story and focusing on an abstract score, rather than dollars-and-cents spending, we run the risk of misleading and confusing clients.

We know from clinical psychology that uncertainty can cause more anxiety than does bad news. By showing clients concrete, dollar-based information on how spending would have needed to change through relatable time periods like these, advisors can remove or at least reduce anxiety and give clients permission to go live their lives.

I have received numerous first-hand stories from advisors about this effect on client psychology. One advisor said:

My clients, who are set to retire […] had second thoughts about retiring this year due to the market and, ‘What if this is like another Depression?’ I said, ‘Let’s see for ourselves,’ and reviewed the retirement stress test using the Great Depression scenario. The clients were amazed to see not only didn’t they run out of money, but their income provided for all their needs and goals throughout the entire time period! They left the meeting confident in their decision to move forward with retirement this year.

Another advisor told me:

We’ve used [the retirement stress test] directly in client meetings during some of the market turmoil of 2022 and early 2023 and immediately you can see relief and confidence from the client when they see that their retirement would have held strong through events much worse that what we are seeing now.

A third advisor noted that this approach to stress testing helps clients understand the value of their firm’s adjustment-based planning and ongoing guidance:

I can show someone that market shocks are a very real possibility in retirement, but here is how we would have helped them navigate [them] – that level of awareness and reassurance can provide such peace of mind.

Could the future be worse than the past? Of course! But recorded history does include some dark periods, and these are useful and instructive examples of how a good adjustment-based retirement income plan, monitored and updated regularly, can produce reasonable adjustments in spending.

In each of these stress tests, decisions about when and how to adjust spending in tough times are made only with information that would have been available at that point in history – no cheating by looking into the future. And that’s exactly the situation planners find themselves in today: with the need to use all information at their disposal to make good recommendations about spending and adjustments. Stress tests that illustrate spending and adjustments are invaluable for improving advice, client experiences, and client confidence.

Justin Fitzpatrick, PhD, CFA, CFP® is CIO of Income Lab.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All