Investor indifference to the threat of a prolonged debt-ceiling impasse has left a handful of tail-risk strategies almost too cheap to pass up.

That’s according to Bank of America Corp. analysts, whose math shows that purchasing hedges now with options on the S&P 500 and gold would stand to yield profits more than 30 times the upfront premium should negotiations break down and markets react like they did in 2011.

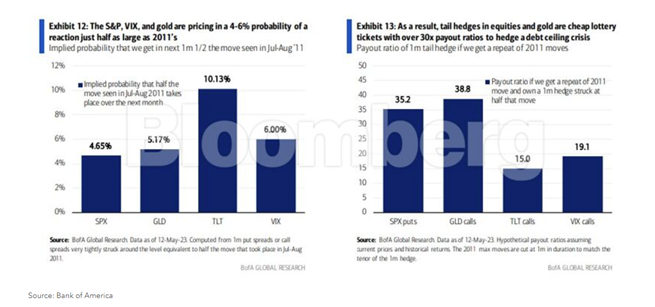

Derivatives tied to those assets point to a very low probability of a crisis happening — even one that’s half as bad as 12 years ago. Based on BofA’s calculation, market-derived odds now sit between 4% and 6%.

Money managers are similarly unfazed. In a BofA survey, released this week, 71% of the pros say they expect a resolution before the government exhausts its options to fund itself. That’s at odds with a surge in the cost of insuring Treasuries against default that by some measures has eclipsed levels during previous debt-ceiling standoffs since at least 2007.

“Various asset classes remain seemingly calm about the current (arguably riskier) situation,” BofA strategists including Gonzalo Asis wrote in a note Tuesday. “We, therefore, find it sensible to buy S&P and gold hedges.”

Treasury Secretary Janet Yellen has repeated warnings that the Treasury risks running out of room to stay under the debt ceiling as soon as June 1, commonly referred to as the X-date. After a meeting Tuesday at the White House, President Joe Biden and congressional leaders said they were optimistic a bipartisan deal to raise the debt ceiling could be possible within days even as House Speaker Kevin McCarthy warned the two sides remained far apart.

During 2011’s drama around the debt cap, the S&P 500 tumbled 17% over one month through early August, while the Cboe Volatility Index, or VIX, jumped along with gold and Treasuries.

Even if the equity benchmark index incurs a loss just half the size it suffered 12 years ago, a trader buying one-month put contracts stuck 8.5% out of the money would pocket a profit amounting to 35 times the initial premium, according to BofA’s analysis.

Similarly, owning call options on gold and the VIX would see a payout ratio of 39 and 19, respectively, the study showed.

With long-dated Treasuries implying a relatively higher probability of a 2011-styled shock, at 10%, calls on the iShares 20+ Year Treasury Bond ETF (ticker TLT) could fetch a lower payout ratio of 15, based on the team’s calculation.

To be sure, the potential for giant payouts reflects a lack of demand for protection around the event. After all, many investors have been cautiously positioned, parking money in cash while pivoting toward haven assets such as gold and consumer-staple stocks

Moreover, history shows whatever impact that debt-ceiling chaos brought to the market, it got erased eventually. After the 2011 debacle, the S&P 500 fully recovered six months later.

“We’re not going to try to get too cute about what may or may not happen here,” said Rich Weiss, chief investment officer for multi-asset strategies at American Century Investment Management “We’re already defensively positioned. That’s about as good as you could do.”

With X-date fast approaching, investors should take the opportunity to purchase some insurance against an unfavorable outcome, according to BofA analysts.

“Tail hedges in equities and gold are cheap lottery tickets,” they wrote.

A message from Advisor Perspectives and Vetta Fi: To learn more on this and other topics, check out our full schedule of upcoming CE-approved virtual events.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.