Corporate America, one of the few reliable purchasers of equities in this bear market, is retreating from its buying binge, fresh evidence that the Federal Reserve-induced slowdown is taking a toll on business sentiment.

US firms have announced plans to spend $580 billion on their own stock this year through Monday, down 8% from the same period a year ago, according to data compiled by Birinyi Associates. That’s a shift from January when buybacks were off to a record start.

Two-quarters of declining profits are straining the cash-generating machine at the same time banking stress and the specter of a recession loom. Some firms view it all as a reason to conserve cash. Goldman Sachs Group Inc. strategists have noticed and cut their forecast for market-wide repurchases, predicting a 15% decline for the full year.

“Buybacks give companies the flexibility to take their foot off of the pedal when they see a turn coming,” said Jeff Rubin, director of research at Birinyi. “I would surmise the decrease in actual corporate activity is a combination of companies taking a look at the macro picture of the economy as well as their lower year-over-year earnings and deciding to pare back their purchases as a precautionary measure.”

Companies are beating a retreat after last year’s record $923 billion buying spree defied naysayers. At the time, corporate spending helped prevent the bear market in stocks from worsening when investors of all stripes were bailing.

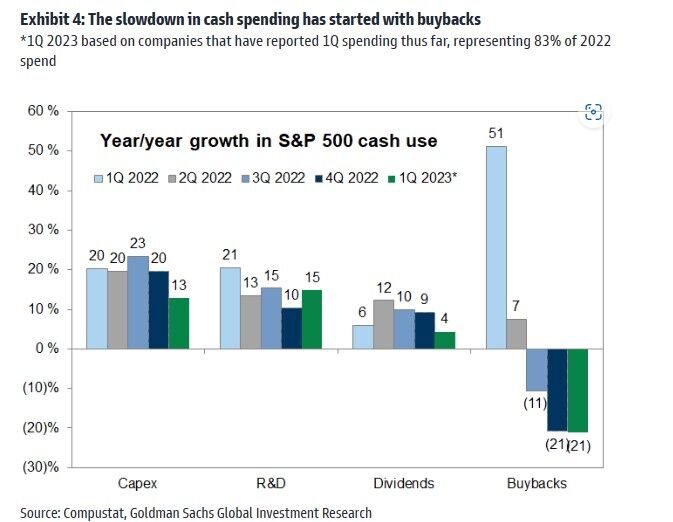

Now, that commitment may be waning as the S&P 500 has rallied 15% from its October low and profits are expected to contract for another two quarters. In the first three months of 2023, actual buybacks among the index’s constituents tumbled 21% from a year ago, according to data compiled by Goldman.

The firm’s strategists, including Ryan Hammond and David Kostin, expect companies to spend less money this year after their cash piles by one measure fell to the lowest since 2010. Excluding financial firms, cash balances plunged 13% in the last 12 months — the sharpest decline on record.

The shrinking pool of cash means buybacks will face a big reduction as chief executives stick to plans for dividends and capital spending. Total repurchases will amount to $808 billion this year, according to the Goldman team, down from a November estimate of $869 billion.

“The slowdown in earnings growth, the increase in policy uncertainty following the recent banking stress, and high starting valuations at which to repurchase stock all pose headwinds to buybacks,” the strategists wrote in a note this week. “The cost of debt has risen sharply, removing the incentive for debt-funded buybacks.”

While the team expects buybacks to stage a comeback in 2024, the anticipated drop this year removes one of the biggest allies stock bulls have had. In a tally of equity supply and demand kept by Goldman, corporate buying has topped all other investor categories from pensions to mutual funds and households in most of the past decade.

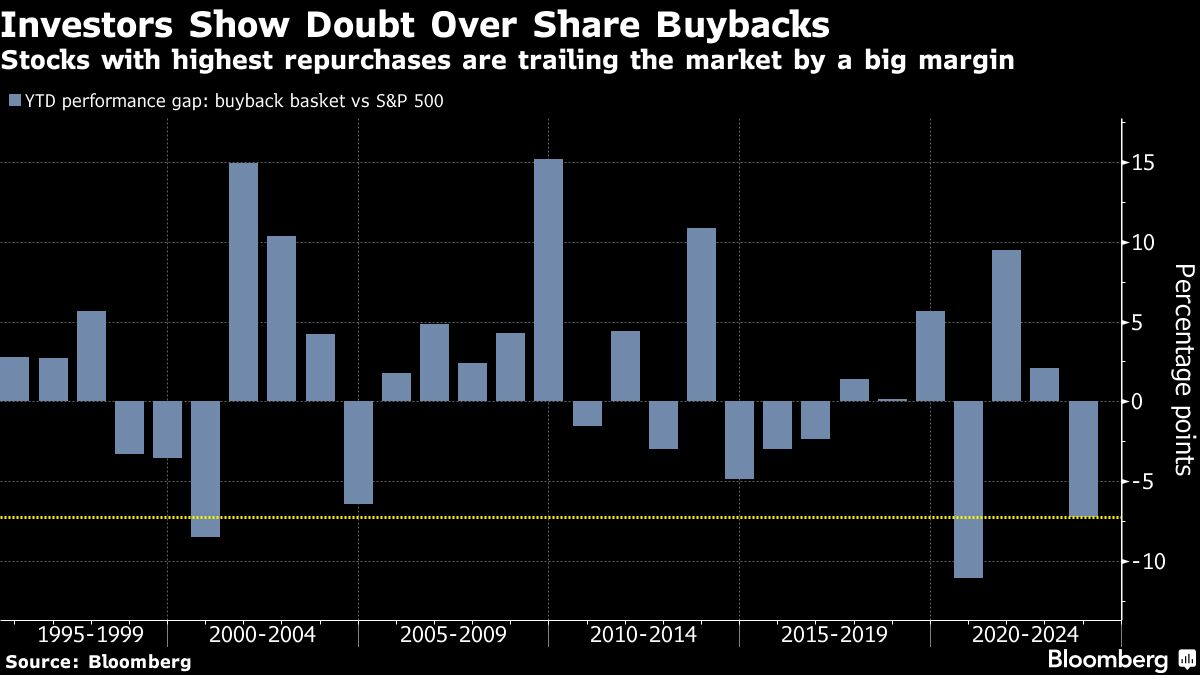

There are signs that investors are growing leery about the sustainability of this purchasing power. An index tracking S&P 500 stocks with the highest buybacks has lagged behind the broad benchmark by 7 percentage points since January, the worst performance this far into a year behind only the 2020 pandemic crisis and the 2000 bursting of the internet bubble.

Indeed, funding stress is creeping up among firms, according to Charles Cara, head of quantitative strategy at Absolute Strategy Research. He tracks a company’s ability to finance buybacks via a funding ratio that compares them to free cash flows after dividends and share issuance. In the 12 months through March, cash flows covered less than 50% of $178 billion in repurchases.

“These buybacks have to be at risk,” Cara said. “We would worry about repurchase programs coming to an end and not being renewed.”

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Lu Wang