Investors are bailing on preferred shares at a historic clip because of the growing concern about the health of US regional banks.

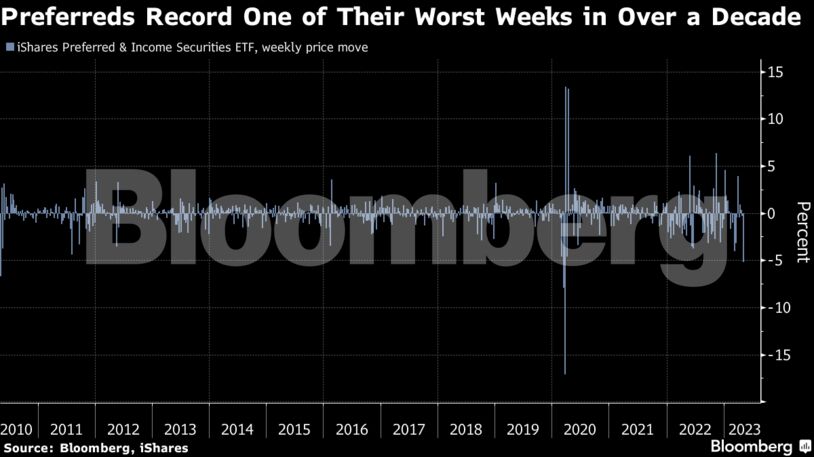

A $12.2 billion iShares exchange-traded fund tracking the wider preferred market sank 5.1% last week, marking one of the biggest selloffs since the global financial crisis.

Preferreds, a kind of hybrid security, are popular with banks because they help meet capital requirements without diluting shareholders. But now, the market is being upended in a selloff fueled by regional bank failures.

Issuance by banks is running at its slowest pace since 2018, and money managers say trading in the secondary market is a challenge.

“Without issuance and with money on sidelines, it’s just ‘what do you do?’,” said Allen Hassan, head of preferred stock trading at Ziegler Capital Markets, who has been trading the securities for more than 20 years. “It doesn’t feel like there’s a lot of confidence out there.”

Traders describe an illiquid market that’s become difficult to navigate, with big gaps appearing in prices from day to day. Part of the issue is that few are willing to buy riskier preferreds given the recent string of regional bank failures, they say.

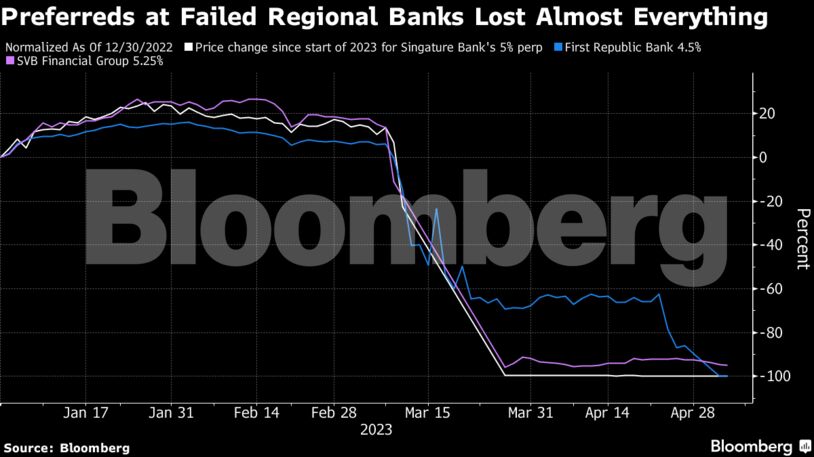

First Republic Bank’s preferreds were effectively wiped out after the failed lender was bought by JPMorgan Chase & Co. First Horizon Corp’s preferreds tumbled 26% in the week after scrapping its merger with Toronto-Dominion Bank. The shares are now indicated at $17.4, or just under 70% of face value.

To long-time watchers, like Collin Martin, a director and fixed income strategist at Charles Schwab & Co., the price declines are some of the sharpest since the global financial crisis.

Big investors have also been getting out. Cohen & Steers Inc. cut exposure to regional bank preferreds, while Spectrum Asset Management, founded by outspoken market veteran Mark Lieb, sold First Republic Bank preferreds in the weeks before it collapsed.

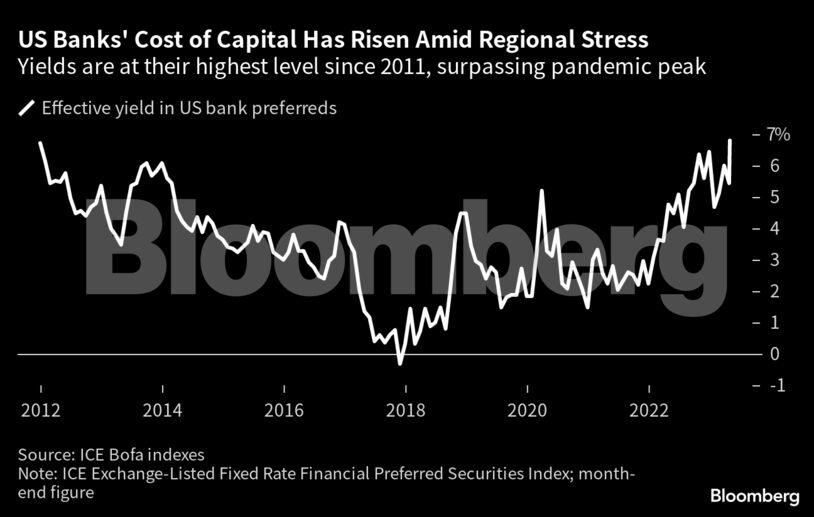

Preferreds rank above common equity, but below all types of debt and pay high dividends. The securities are typically perpetual, but banks often redeem them early if they can replace them at cheaper rates. But with effective yields now at the highest in 12 years, according to an ICE BofA index, analysts say banks are more likely to skip their call options.

Refinancing is too expensive in the current market, though most big US banks don’t need to raise new capital at the moment, said Martin at Charles Schwab.

For smaller lenders, it could spell trouble. They rely on preferred shares to fulfill regulatory requirements and with investors demanding sky-high dividends, they’ve effectively been shut out of the market.

Preferred shares are the US equivalent of European banks’ additional tier 1 bonds, which drew attention recently after a historic $17 billion wipeout of Credit Suisse Group AG notes. Unlike preferreds, AT1s have more complex mechanisms to force losses on bondholders at times of stress, including conversion into common equity or loss of principal.

Exchange-traded preferreds with first calls this year and next are indicated more than $3 below their face value of $25 on average, a sign that more banks may skip their calls, based on data compiled by Bloomberg.

Even so, some investors are spying on opportunities in the wreckage. The iShares preferred ETF rebounded 1.5% on Friday, the first gain in five days.

“You have to buy them when there’s blood in the water,” said Ziegler’s Hassan. “This product will be the cheapest paper to buy out there. There will be a lot of money to make.”

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.